Six gigawatts. That is the total AMD Instinct GPU capacity AMD (NASDAQ:AMD | AMD Price Prediction) will deploy for Meta under a partnership disclosed alongside its most recent earnings, with the first 1-gigawatt tranche powered by a custom MI450-based GPU. For scale reference, one gigawatt is roughly the output of a large nuclear reactor. Meta is committing to power-plant-scale AMD silicon, and it is doing so on top of a separate 6-gigawatt OpenAI agreement already on the books.

The total investment in compute for AMD has been rumored to be around $300 billion, though we’ll see what ultimately gets invested over time. Indeed, that’s the big question mark right now in financial markets.

What It Means

Hyperscalers do not sign gigawatt-scale accelerator agreements as hedges. They sign them when they intend to build. That reframes AMD from a challenger chasing NVIDIA (NASDAQ:NVDA) into a co-supplier for the largest AI infrastructure buildouts in the world.

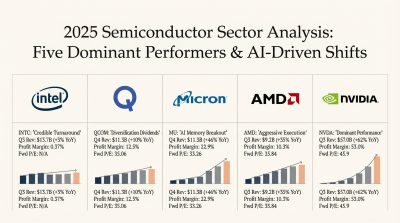

The financial fingerprints are already on the tape. Q1 FY2026 Data Center revenue reached $5.775 billion, up 57% year over year, making it the largest and fastest-growing of AMD’s four segments. Total Q1 revenue landed at $10.253 billion, up 37.9% year over year, beating the $9.91 billion consensus by 3.41%. Non-GAAP EPS came in at $1.37 versus $1.29 expected, driven by non-GAAP gross margins which expanded to 55% (up 170 basis points year over year).

Cash generation is scaling with the mix shift. Q1 free cash flow hit $2.566 billion, up 252.96% year over year, on operating cash flow of $2.955 billion. Net income more than doubled to $1.383 billion, up 95.06%.

Market Reaction

AMD shares closed at $517.82 on July 2, 2026, down 4.26% on the day. That single-session dip is noise inside a much larger move. AMD is up 141.79% year to date from $214.16 at the end of 2025, and up 273.82% over the past year. For context, over the same twelve months, NVIDIA is up 24.06%.

Bull Case

The AMD bull case rests on a simple observation – the company’s customer roster now looks like NVIDIA’s. AWS, Google Cloud, Microsoft Azure, and Tencent are expanding 5th Gen EPYC-powered instances. Meta is the lead customer for 6th Gen EPYC (Venice and Verano). Oracle Cloud Infrastructure is standing up a 50,000-GPU AI supercluster using AMD Helios rack design in Q3 2026. Samsung is supplying HBM4 memory for the MI455X.

Guidance points to further acceleration. AMD guided Q2 FY2026 revenue to roughly $11.20 billion, implying about 46% year-over-year growth, with non-GAAP gross margin expanding to about 56%. On the Q1 call, CEO Lisa Su said, “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations and a growing pipeline of large-scale deployments providing us with increasing visibility into our growth trajectory.”

The pressure on rivals is visible in relative performance. Intel (NASDAQ:INTC) still carries a negative EPS of -$0.60 on a trailing basis, with quarterly earnings growth down 71.7% year over year. NVIDIA remains the incumbent, but AMD is winning nameplate capacity commitments rather than trial orders. Analyst posture reflects it: 41 buy or strong buy ratings against 10 holds and zero sells, with a consensus target of $508.31.

Bottom Line

Six gigawatts from Meta and another six from OpenAI turn AMD’s AI narrative from optionality into contracted backlog. For long-term holders, the anchor to watch is Data Center revenue, which drove the Q1 beat and underpins Q2 guidance of about $11.20 billion in total revenue.

AMD’s valuation is stretched, with a forward P/E of 77 on a stock up 141.79% year to date leaves little room for execution slips. But, the shipments behind those gigawatts are what the next earnings report will need to prove. That is the number that decides whether the pressure on rivals turns into permanent market share.

Contact [email protected] for any questions or corrections.