Intel (NASDAQ:INTC | INTC Price Prediction) is the stock of the moment, riding a 250.79% year-to-date melt-up and dominating every chip headline. But here is what you should actually be watching.

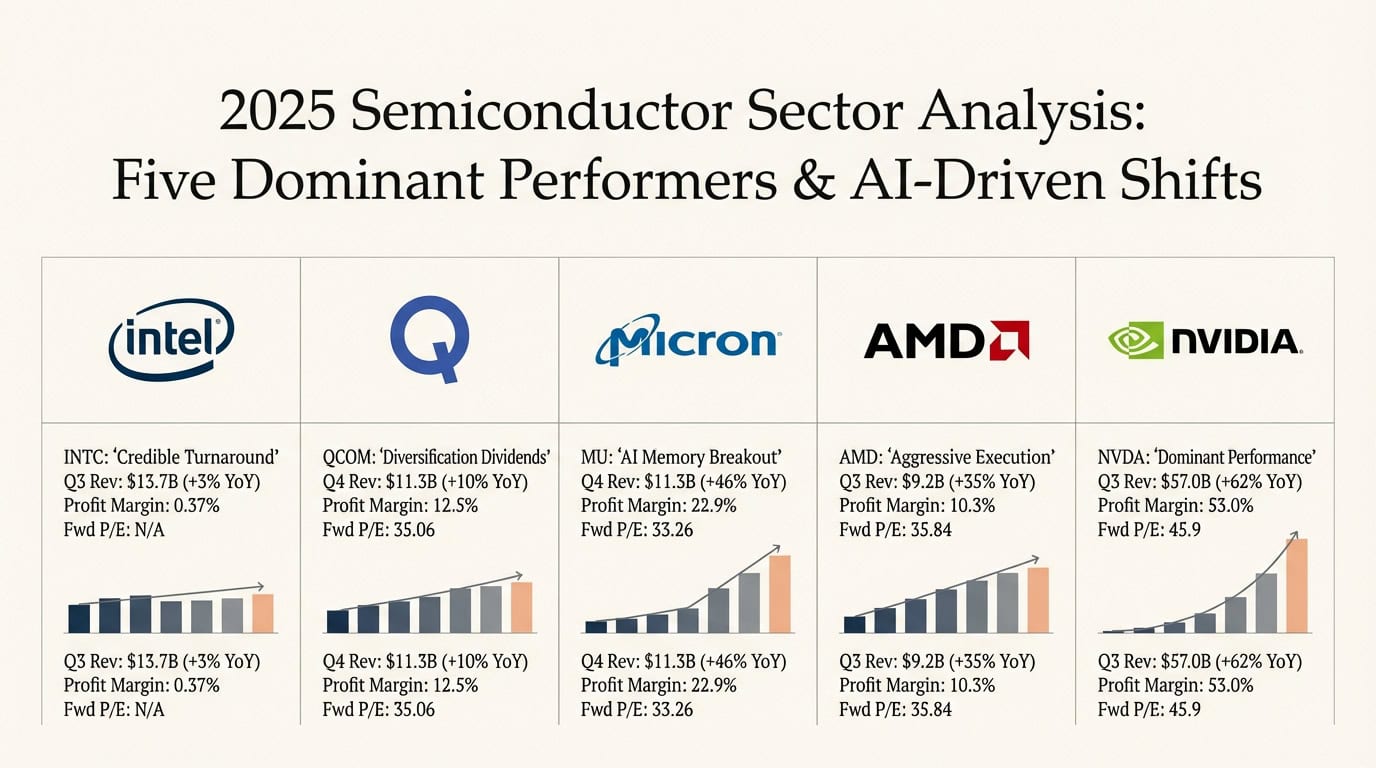

The Intel story sounds tidy at the headline: revenue beat by 9.22%, non-GAAP EPS of $0.29, and a CEO talking up agentic AI. Look one layer down and the turnaround is paid for with shareholder cash. Intel posted a GAAP net loss of $3.728 billion tied to a $4.07 billion Mobileye impairment, free cash flow of negative $3.867 billion, and an Intel Foundry segment that bled $2.51 billion in operating losses in Q4 FY25 alone. Q2 FY26 guidance calls for non-GAAP EPS of just $0.20, a sequential step down from the headline number everyone is celebrating. Intel even flagged the risk of a pause or discontinuation of Intel 14A if customer demand falls short, alongside ongoing U.S. government acquisition of significant equity interests that dilute existing holders. On Reddit, a post titled “Intel trading at a ~119x forward P/E and nobody is talking about this” drew 672 upvotes for a reason.

The reflex move is to rotate into NVIDIA (NASDAQ:NVDA). At a $215.94 billion revenue base and 75.2% non-GAAP gross margins, NVIDIA is the most crowded long in the market. The room is full. The better seat is next door.

The Redirect: AMD Is the Under-Owned No. 2 in AI

Advanced Micro Devices (NASDAQ:AMD) reported Q1 FY26 revenue of $10.253 billion, up 37.85% year over year, with non-GAAP EPS of $1.37 beating consensus by 5.88%. Three reasons it deserves the attention investors are wasting on Intel:

- A named hyperscaler win at gigawatt scale. AMD has a commitment from Meta to deploy up to 6 gigawatts of AMD Instinct GPUs, with the first 1-GW powered by a custom MI450-based GPU. That is a concrete, signed-up anchor customer.

- Hyperscaler pipeline exceeding plan. CEO Lisa Su told investors that “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.” AWS, Google Cloud, Microsoft Azure, and Tencent are expanding 5th Gen EPYC instances. AMD is being designed in.

- Operating leverage is kicking in. Data Center revenue grew 57% to $5.775 billion, non-GAAP gross margin expanded 170 basis points to 55%, and free cash flow surged 252.96% to $2.566 billion. Q2 guidance calls for revenue of roughly $11.2 billion, around 46% growth, with gross margin widening further to ~56%. Growth is accelerating while margins expand. That is the rare combination.

Intel’s chart is up because the U.S. government, NVIDIA, and SoftBank wrote checks while the foundry has yet to turn. NVIDIA’s chart is up because every fund in the country owns it. AMD’s chart is up because the underlying business is compounding cash at triple-digit rates with a customer list that now includes Meta at 6 gigawatts. One of these stories does not require a leap of faith.

The action statement: stop reading Intel headlines and start doing the work on AMD.

Contact [email protected] for any questions or corrections.