An international equity sleeve inside a taxable account has a quieter tax drag than a business development company (BDC) or mortgage real estate investment trust (REIT), but it is not trivial. Vanguard Total International Stock Index Fund ETF (NASDAQ:VXUS) paid $2.1884 per share in trailing-12-month distributions on a closing price of $84.90 on July 9, 2026. A meaningful slice of that income is non-qualified because it comes from foreign issuers, which means more of it is taxed at ordinary rates in a taxable account than a comparable U.S. index fund would generate. That is the case for holding VXUS in a Roth IRA.

Why VXUS Belongs in a Roth

Three factors matter. First, VXUS distributes on a quarterly cadence, typically ex-dividend in mid-March, mid-June, mid-September, and mid-December, with December historically the largest payment. Second, the fund carries a razor-thin expense ratio of 0.05% since March 18, 2026, so tax drag is the dominant cost of taxable ownership, well ahead of fees. Third, a portion of VXUS’s dividends flow through as non-qualified foreign income, which is taxed at your marginal ordinary rate rather than at long-term capital gains rates.

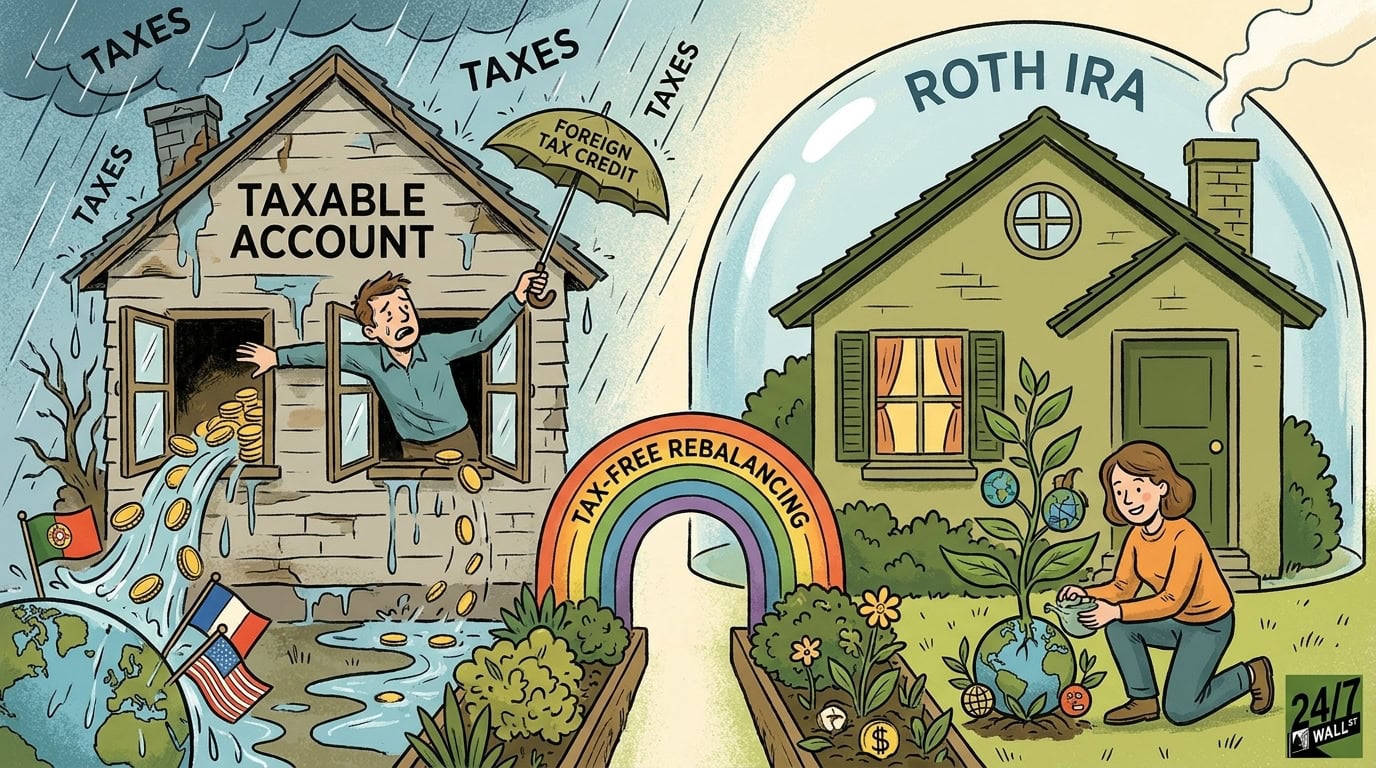

However, in a taxable account, foreign taxes withheld on those dividends can be recovered through the foreign tax credit. Inside a Roth, that credit is forfeited. That tradeoff is real, and it is the reason this decision is closer than it looks compared with holding a U.S. growth ETF in a Roth.

The Tax Delta: Roth Versus Taxable

Use a $500,000 VXUS position as the working example. On the annualized forward distribution estimate of $1.5444 per share, the position generates roughly $9,100 in annual distributions. Assume, conservatively, that the effective ordinary-rate exposure (after the qualified portion and after any recoverable foreign tax credit in a taxable account) lands near the full amount at the 24% bracket.

| Scenario ($500K in VXUS, 24% bracket) | Gross Income | Federal Tax | Net Income |

|---|---|---|---|

| Taxable brokerage | $9,100 | $2,184 | $6,916 |

| Roth IRA | $9,100 | $0 | $9,100 |

| Annual delta | n/a | n/a | $2,184 |

| 10-year delta (no growth) | n/a | n/a | $21,840 |

Then subtract the lost foreign tax credit in the Roth case, which typically runs several hundred dollars on a position this size. The Roth still wins at 24%, but the margin is narrower than the headline suggests.

The Bracket Multiplier

With the same $500,000 position and the same roughly $9,100 in annual distributions:

| Bracket | Tax in Taxable | Net in Taxable | Annual Roth Advantage (before FTC) |

|---|---|---|---|

| 22% | $2,002 | $7,098 | $2,002 |

| 24% | $2,184 | $6,916 | $2,184 |

| 32% | $2,912 | $6,188 | $2,912 |

| 37% | $3,367 | $5,733 | $3,367 |

The higher the bracket, the more the non-qualified slice of VXUS’s distributions costs in a taxable account, and the harder the foreign tax credit has to work to close that gap. For 32% and 37% filers, the Roth case is materially stronger. (For readers weighing whether to sequence international exposure inside conversions, the Roth Window framework maps the multi-year path.)

The Angle Most Readers Miss: Tax-Free Rebalancing

International equities historically drift versus U.S. equities. VXUS returned 22.4% over the trailing year and 29.4% over five years, while Vanguard Total Stock Market ETF (NYSEARCA:VTI) returned 20.8% and 64.5% over the same windows. In a taxable account, every rebalance between the two sleeves triggers a capital gain. In a Roth, that same rebalance is free. Over 10 or 20 years of disciplined rebalancing, the compounded value of avoiding those taxable gains often exceeds the annual dividend tax delta.

What to Do

- Calculate the non-qualified portion of your VXUS distributions from your prior-year 1099-DIV. If most of the box-1a income is non-qualified, the tax shelter provided by the Roth is more valuable than the foreign tax credit you would forfeit.

- Before your next contribution, prioritize VXUS placement inside a Roth over a U.S. growth ETF, since VXUS’s trailing $2.1884 per share distribution is a larger income stream to shelter than a low-yield growth fund.

- If you already hold VXUS in a taxable account, run the Roth conversion math on that specific lot against the 4.56% 10-year Treasury yield as your opportunity cost, and net out the foreign tax credit you would give up before deciding.

Contact [email protected] for any questions or corrections.