Jim Cramer, the CNBC host and longtime market commentator, offered a measured take on X this morning that cuts through the noise around 2026’s most crowded AI trade: “Meta isn’t as rewarding as a Micron but it is still real money nonetheless.” As a former hedge fund trader, Cramer’s framing is worth unpacking because it captures a discipline that gets lost when one stock runs the way Micron has.

The comparison lands at a natural moment. Meta Platforms (NASDAQ:META | META Price Prediction) rallied 5.71% intraday on July 10, while Micron Technology (NASDAQ:MU) has become the poster child for the memory-in-the-AI-era thesis. Cramer’s argument is that owning the compounder can still be rational, even after the cyclical winner has already tripled.

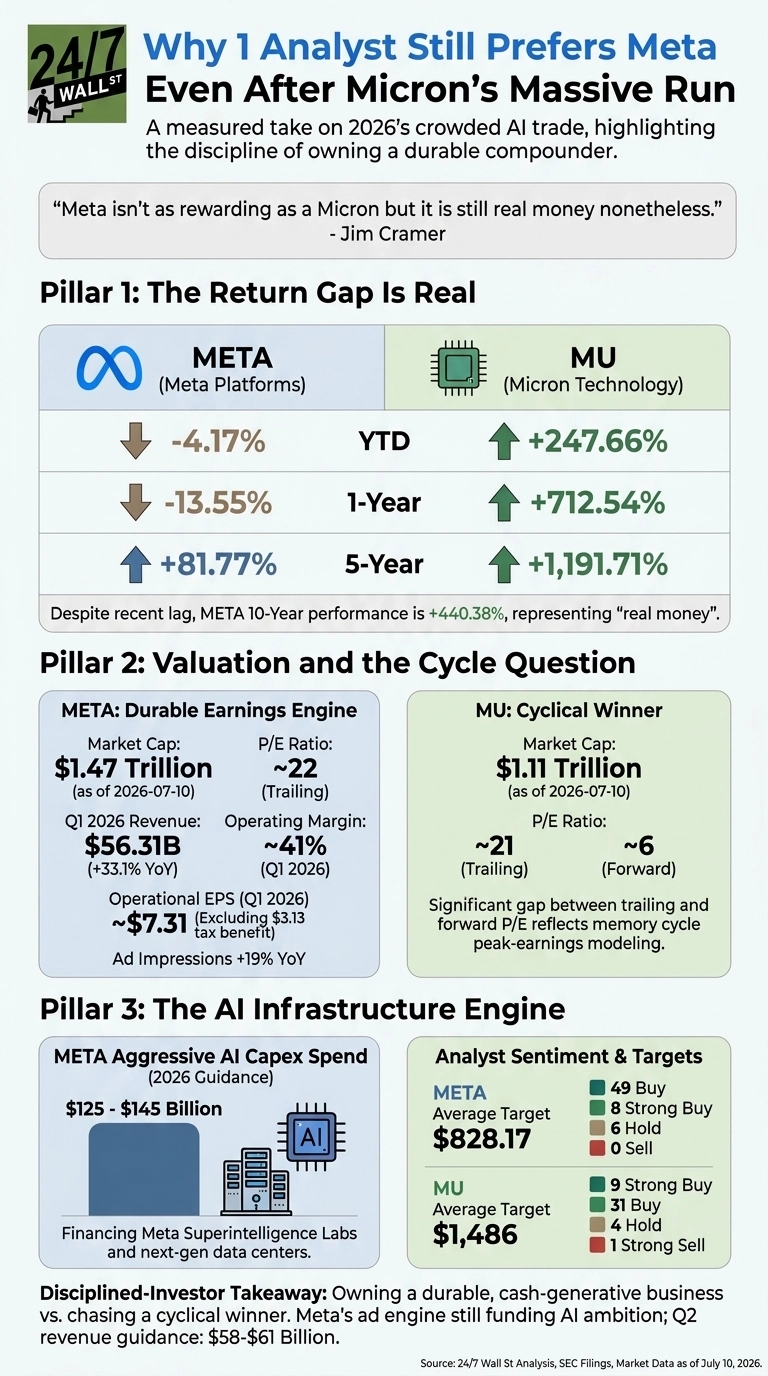

Pillar 1: The Return Gap Is Real

Cramer is acknowledging Micron’s run. The numbers are one-sided.

| Metric | META | MU |

|---|---|---|

| YTD | -4.17% | +247.66% |

| 1-Year | -13.55% | +712.54% |

| 5-Year | +81.77% | +1,191.71% |

| Trailing P/E | 22 | 21 |

Meta has actually trailed the market over the trailing 12 months, but the tone has shifted. Shares are up 8.12% over the past month and 8.33% over the past week, with the stock trading around $667.54. Micron sits near $980.81. On a 10-year view, Meta is still up 440.38%. That is the “real money” Cramer is referencing.

Pillar 2: Valuation and the Cycle Question

Meta trades at a P/E of roughly 22, with a market cap of about $1.47 trillion. Micron, at a market cap near $1.11 trillion, screens at a similar trailing multiple of 21 and a forward multiple of 6. That gap between trailing and forward is the memory cycle in a nutshell: analysts model peak-earnings power today, and the historical playbook says supply eventually catches demand.

Meta’s earnings are a different animal. Q1 2026 revenue climbed 33.1% to $56.31 billion, with operating margin around 41% and ad impressions up 19% year over year (per Meta’s SEC filing). The reported $10.44 EPS included a $3.13 per share tax benefit, leaving underlying operational EPS near $7.31. Still strong, but investors should back out the noise.

Pillar 3: The AI Infrastructure Engine

The reason Meta remains “real money” in Cramer’s frame is what the company is doing with its cash. Management lifted 2026 capex guidance to a range of $125 to $145 billion, financing the buildout of Meta Superintelligence Labs and next-generation data centers out of an ad business that still produced $55.02 billion in Q1 alone. That capex, incidentally, is a big reason Micron’s order book is what it is (for investors thinking about the picks-and-shovels side of this trade, our 7 Stocks Powering the AI Boom report walks through the infrastructure supply chain).

Sell-side sentiment reflects the split. Meta carries an average price target of $828.17, with 49 buy and 8 strong buy ratings against 6 holds and no sells. Micron’s target sits near $1,486, but with a wider distribution that includes one strong sell.

The Disciplined-Investor Takeaway

Chasing the biggest winner after the fact is a different exercise than owning a durable, cash-generative business. Meta’s 13.55% one-year drawdown and its capex burden are legitimate risks. So is the memory cycle risk baked into Micron’s forward multiple. Cramer’s point is that both can be real money, and an investor who owns Meta through this stretch is not making an obvious mistake because a different stock ran harder. Keep an eye on Meta’s Q2 report, where management’s guided $58 to $61 billion revenue range will show whether the ad engine is still funding the AI ambition without breaking stride.

Contact [email protected] for any questions or corrections.