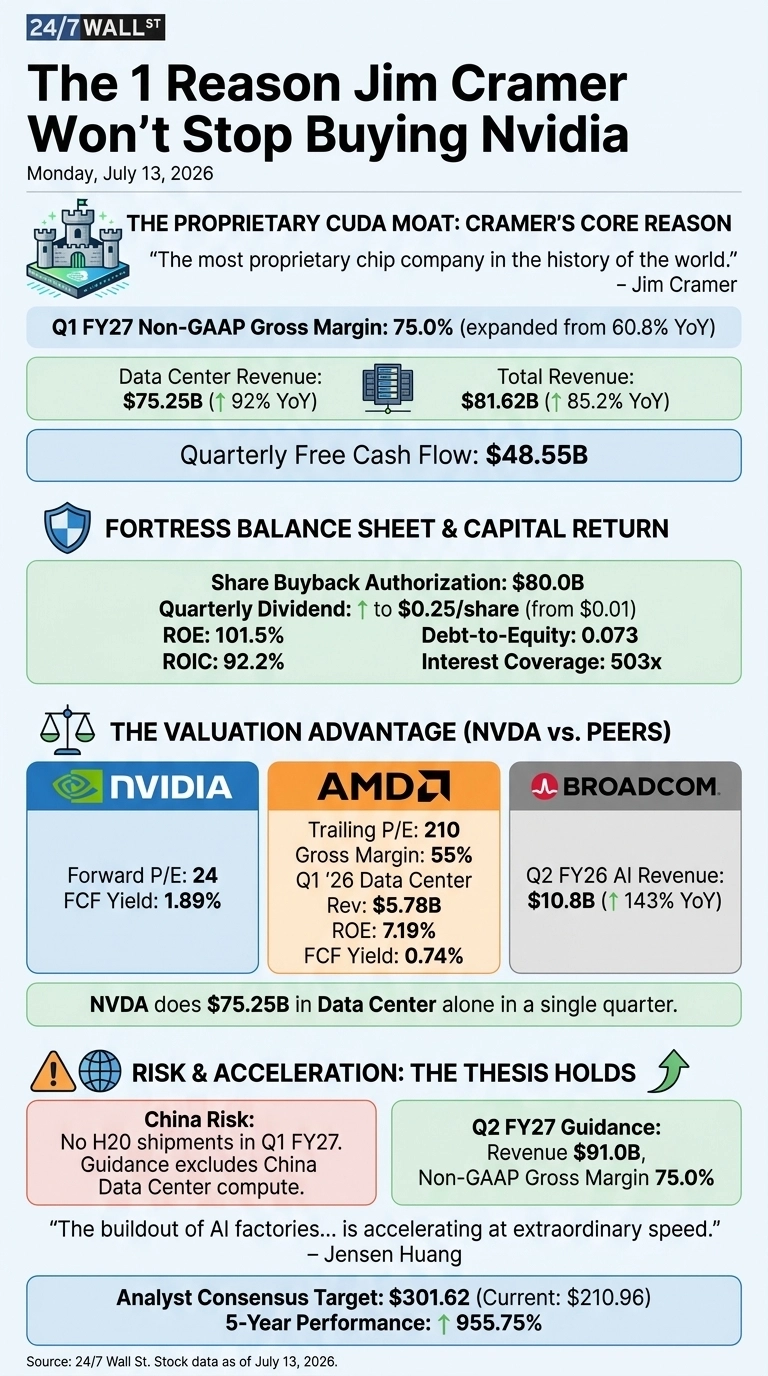

Jim Cramer’s line about NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) being the most proprietary chip company in the history of the world captures why the stock keeps drawing long-term capital. The case for owning it on a decade-long horizon strengthens with every quarterly report.

The Core Reason: CUDA Is the Moat

Every AI developer builds on CUDA. Each hyperscaler trains on it. Every frontier model, from OpenAI to Anthropic to Meta’s multi-year Blackwell and Rubin deployment, runs on it. That software moat is why NVIDIA’s Q1 FY27 non-GAAP gross margin printed at 75%, expanded from 60.8% a year earlier. Numbers like that come from proprietary ecosystems, not commodity chip businesses.

The Receipts

Data Center revenue hit $75.246 billion, up 92% YoY. Data Center networking alone did $14.8 billion, up 199%. Total revenue was $81.615 billion, growing 85.2%. Free cash flow in a single quarter came in at $48.554 billion.

The board authorized an additional $80 billion share buyback and lifted the quarterly dividend from $0.01 to $0.25 per share. Return on equity is 101.49%. Return on invested capital is 92.21%. Debt-to-equity sits at 0.073, with interest coverage of 503.42. A fortress balance sheet stapled to a growth engine.

The Valuation Nobody Wants to Hear

Here is the part worth focusing on. NVIDIA trades at a forward P/E of 24. Advanced Micro Devices (NASDAQ:AMD) trades at a trailing P/E of 210 with a gross margin of 55% and Q1 2026 data center revenue of $5.775 billion. AMD’s ROE is 7.19%, and its free cash flow yield is 0.74%, against NVIDIA’s 1.89%.

Broadcom (NASDAQ:AVGO) is a real business. Q2 FY26 AI semiconductor revenue was $10.8 billion, up 143% YoY, and CEO Hock Tan is targeting $100 billion in AI sales by 2027. NVIDIA already does $75.25 billion in data center alone in a single quarter. The platform is the differentiator.

The Real Risk

China is the real one. There were no H20 compute products shipped to China in Q1 FY27, and the Q2 FY27 guidance excludes any Data Center compute revenue from China. Custom silicon from Amazon Trainium and Broadcom is another live threat.

But NVIDIA guided $91 billion for Q2 FY27 anyway, with a 75% non-GAAP gross margin. The moat absorbed the China hit and kept accelerating. That is the tell.

Why the Thesis Holds

Jensen Huang put it plainly: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.” Analyst consensus target sits at $301.62 against a current price of $210.96, with 48 buy ratings, 10 strong buys, 2 holds and 1 sell. Over five years the stock is up 955.75%.

The bull case rests on a company generating $48.55 billion of quarterly free cash flow, a 101.5% ROE, and a proprietary software layer nobody has replicated — a combination that belongs on long-term watchlists for as long as the AI cycle runs. It is running.

Contact [email protected] for any questions or corrections.