I keep buying NVIDIA (NASDAQ:NVDA | NVDA Price Prediction), and the receipts make it hard to stop. Every paycheck, every dip, every quarter that prints another set of numbers most companies will never see, I add. This is the position I size up when I should be diversifying away from it, and I want to explain why with the data.

The core of my thesis is simple. Nvidia sells the picks and shovels for what Jensen Huang calls “the largest infrastructure expansion in human history”, and the buyers are the richest companies on earth.

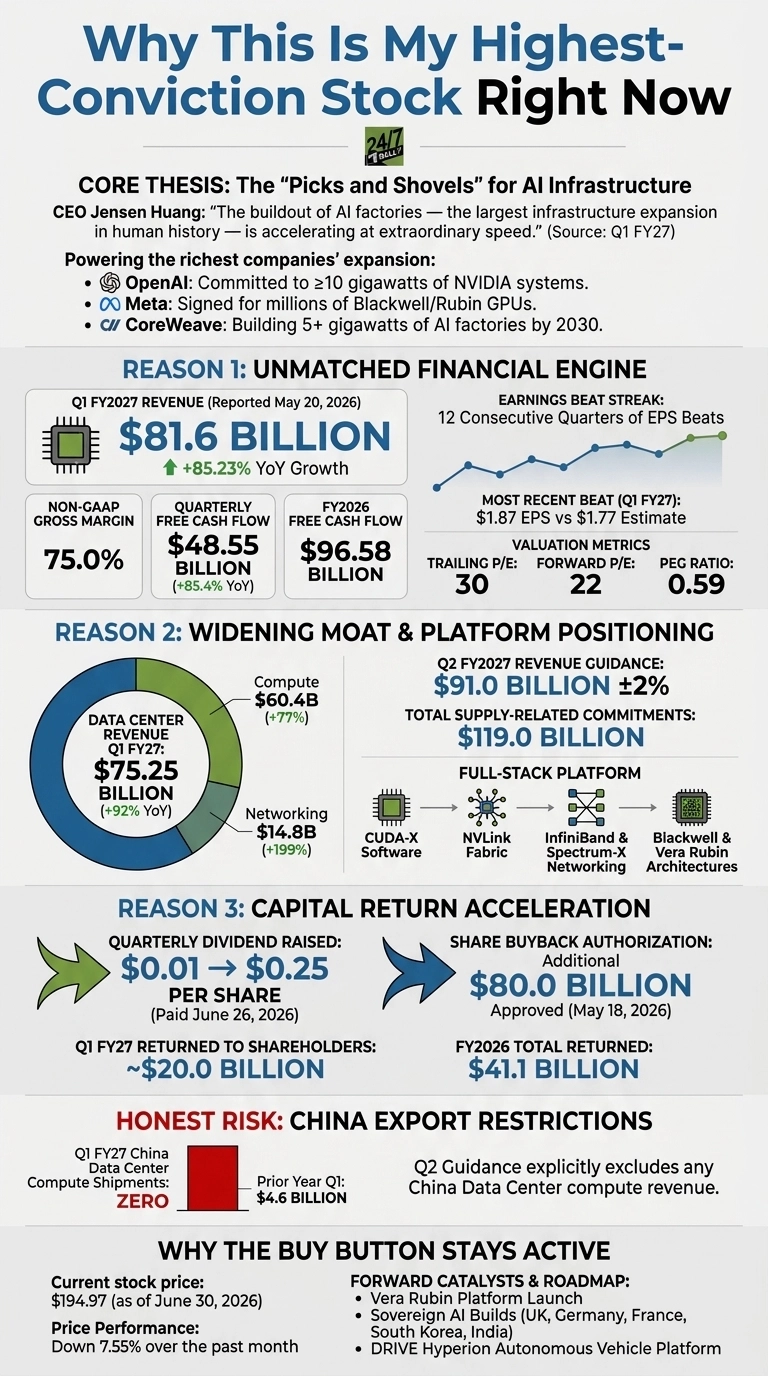

OpenAI committed to at least 10 gigawatts of NVIDIA systems. Meta signed up for millions of Blackwell and Rubin GPUs. CoreWeave is building 5+ gigawatts of AI factories by 2030. When that customer list keeps growing, I keep adding.

Reason 1: A financial engine at a scale I have not seen before

In the quarter reported May 20, 2026, NVIDIA put up revenue of $81.6 billion, growing 85.23% year over year. Non-GAAP gross margin landed at 75%. Free cash flow for the quarter hit $48.55 billion, on top of FY2026 free cash flow of $96.58 billion.

The company has now beaten EPS estimates for 12 consecutive quarters, with the most recent report of $1.87 topping the $1.77 consensus. A trailing P/E of 30 with a PEG of 0.59 and a forward P/E of 22 tells me the market is still pricing this like a normal chip company.

Reason 2: A widening moat

Data Center revenue was $75.25 billion, up 92% year over year, with networking alone growing 199%. The company guided Q2 to $91 billion. Behind that guide sits $119 billion in total supply-related commitments. CUDA, NVLink, InfiniBand, Spectrum-X, and the upcoming Vera Rubin platform mean customers are buying a full stack they cannot easily swap out.

Reason 3: Capital returns have shifted gear

On May 18, 2026, the board raised the quarterly dividend from $0.01 to $0.25 per share and authorized an additional $80 billion in buybacks on top of $38.5 billion remaining. NVIDIA returned $20 billion to shareholders in a single quarter and $41.1 billion across FY2026. For a long-term holder, that is compounding I can feel.

The risk I take seriously

China is the real one. NVIDIA shipped zero H20 Data Center compute units to China in Q1, against $4.6 billion in the year-ago quarter, and Q2 guidance assumes none. Hyperscalers also account for roughly 50% of Data Center revenue, which is real concentration.

My thesis holds because the $91 billion Q2 guide and 85.23% growth were produced with China explicitly stripped out. Demand outside that one geography is already setting records.

Why the buy button stays active

The stock trades at $194.97, down 7.55% over the past month, while the underlying business produced net income of $58.32 billion in one quarter.

Sovereign AI builds across the UK, Germany, France, South Korea, and India, the Vera Rubin ramp, and DRIVE Hyperion in autos give me a multi-year roadmap with cash to fund every step. I keep buying because the cash flow keeps showing up, and the moat keeps getting deeper.

Contact [email protected] for any questions or corrections.