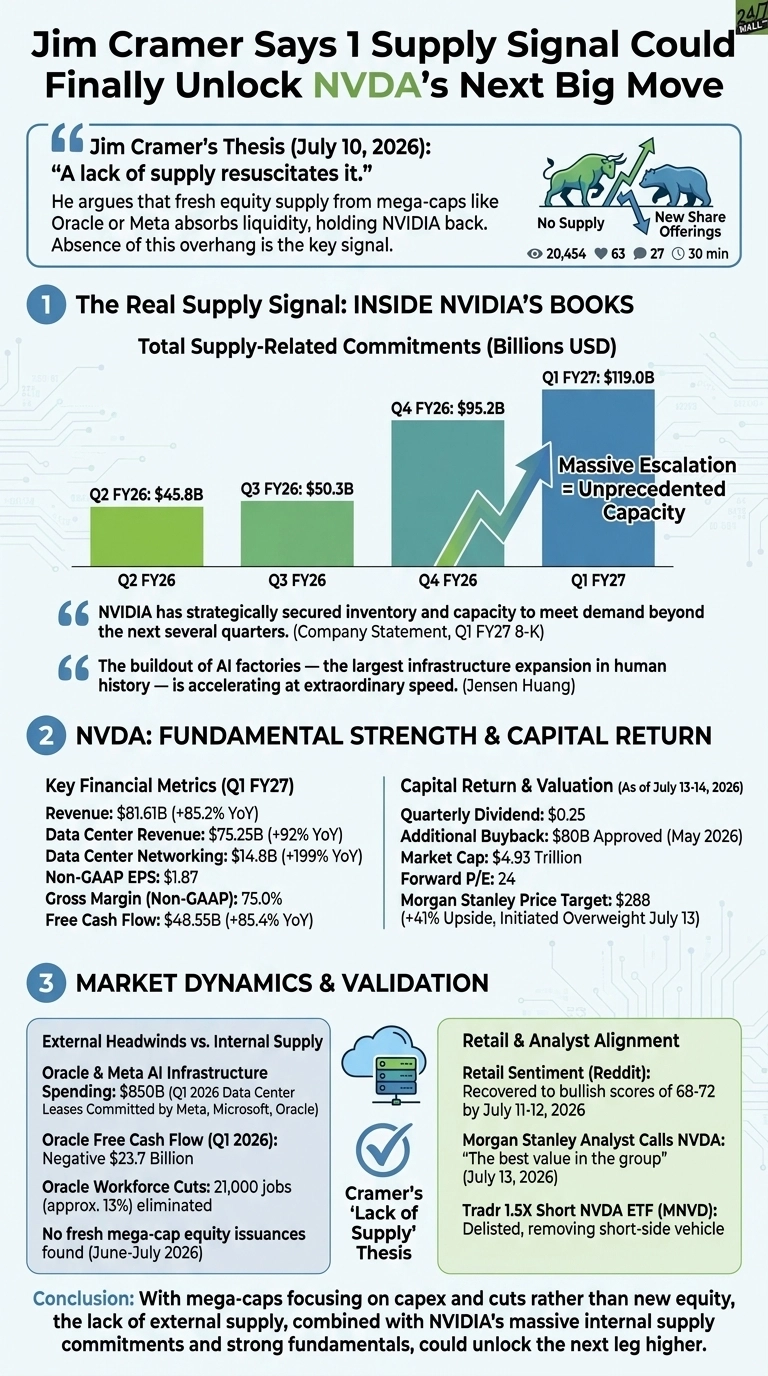

Jim Cramer posted a market thesis on July 10, 2026 arguing that fresh equity supply from mega-caps like Oracle or Meta is the one variable holding NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) back from its next leg higher. In his framing, large new share offerings absorb liquidity that would otherwise chase AI leadership, while “a lack of supply resuscitates it”.

The post drew 20,454 impressions, 63 likes, and 27 replies within 30 minutes, a sign retail traders are already positioning around the same question.

The Supply Mechanic Cramer Is Describing

Equity supply is a real market mechanic. When a mega-cap floats billions in new stock, index funds and generalist portfolios have to make room, often by trimming winners. NVIDIA, the largest weight in most tech baskets, tends to be the release valve.

Cramer’s read is that with $850 billion in Q1 2026 data center leases committed by Meta, Microsoft, and Oracle and Oracle already bleeding negative $23.7 billion in free cash flow, capital markets desks have been bracing for issuance risk.

So far, the news feed shows heavy capex and workforce cuts (Oracle eliminated 21,000 jobs, roughly 13% of its workforce) rather than fresh secondaries. If that holds, the overhang Cramer identifies simply is not there.

NVDA: The Numbers Behind the Setup

NVIDIA closed at $203.53 on July 13, down 3.52% on the day and off 4.2% over the past month, though still up 23.57% over the past year. Market cap sits near $4.93 trillion on a forward P/E of 24, which Cramer has repeatedly called mispriced given NVIDIA’s software moat.

The fundamental case is intact. Q1 FY2027 revenue landed at $81.61 billion, up 85.2% year over year, with data center revenue of $75.25 billion (+92% YoY) and data center networking of $14.8 billion (+199% YoY). Non-GAAP EPS came in at $1.87. Guidance for Q2 calls for $91 billion in revenue at a 75% gross margin.

The Real Supply Signal Is Inside NVIDIA’s Filing

The most concrete supply signal sits inside NVIDIA’s own books, on the balance sheet rather than the issuance calendar. Total supply-related commitments jumped to $119 billion, up from $95.2 billion at the end of Q4 FY26 and $45.8 billion at Q2 FY26. Multi-year cloud commitments climbed to $30 billion.

Management stated in its Q1 FY27 8-K that “NVIDIA has strategically secured inventory and capacity to meet demand beyond the next several quarters”. Jensen Huang framed the backdrop as “the largest infrastructure expansion in human history”. Capital return is scaling in parallel: a dividend hike to $0.25 quarterly and an additional $80 billion buyback authorization approved in May.

Wall Street is aligning with Cramer’s view. Morgan Stanley’s Joseph Moore initiated coverage on July 13 at Overweight with a $288 price target, implying 41% upside, calling NVDA “the best value in the group”.

What To Watch Next

Cramer’s thesis puts the burden on the calendar. If Oracle, Meta, or another hyperscaler taps public equity markets in size before NVIDIA’s next earnings report, the overhang argument stays alive.

If issuance stays quiet while NVIDIA delivers on its $91 billion Q2 guide, the supply constraint flips from headwind to tailwind. Retail sentiment on Reddit already recovered to bullish scores of 68 to 72 by July 11 to 12, suggesting the audience is primed for exactly the setup Cramer described.

Contact [email protected] for any questions or corrections.