At $134, Palantir (NASDAQ:PLTR | PLTR Price Prediction) screens as fully valued, while at $220, NVIDIA (NASDAQ:NVDA) screens more attractively on the numbers. Both anchor the AI trade, but their setups differ sharply.

Palantir builds data and AI software (Gotham, Foundry, AIP) for U.S. defense, intelligence, and commercial markets. After reaching a $207.52 high in February, the stock unwound to the low $130s, with Polymarket pegging a 99.5% probability close in the $132 to $134 band.

NVIDIA designs the GPUs powering hyperscale AI build-outs. It sits at a roughly $5.46 trillion market cap with partnerships across Meta, Anthropic, AWS, Azure, Oracle, and CoreWeave, and guided Q1 FY27 revenue to $78.0B, ahead of prior expectations.

Why the AI bull case still has legs

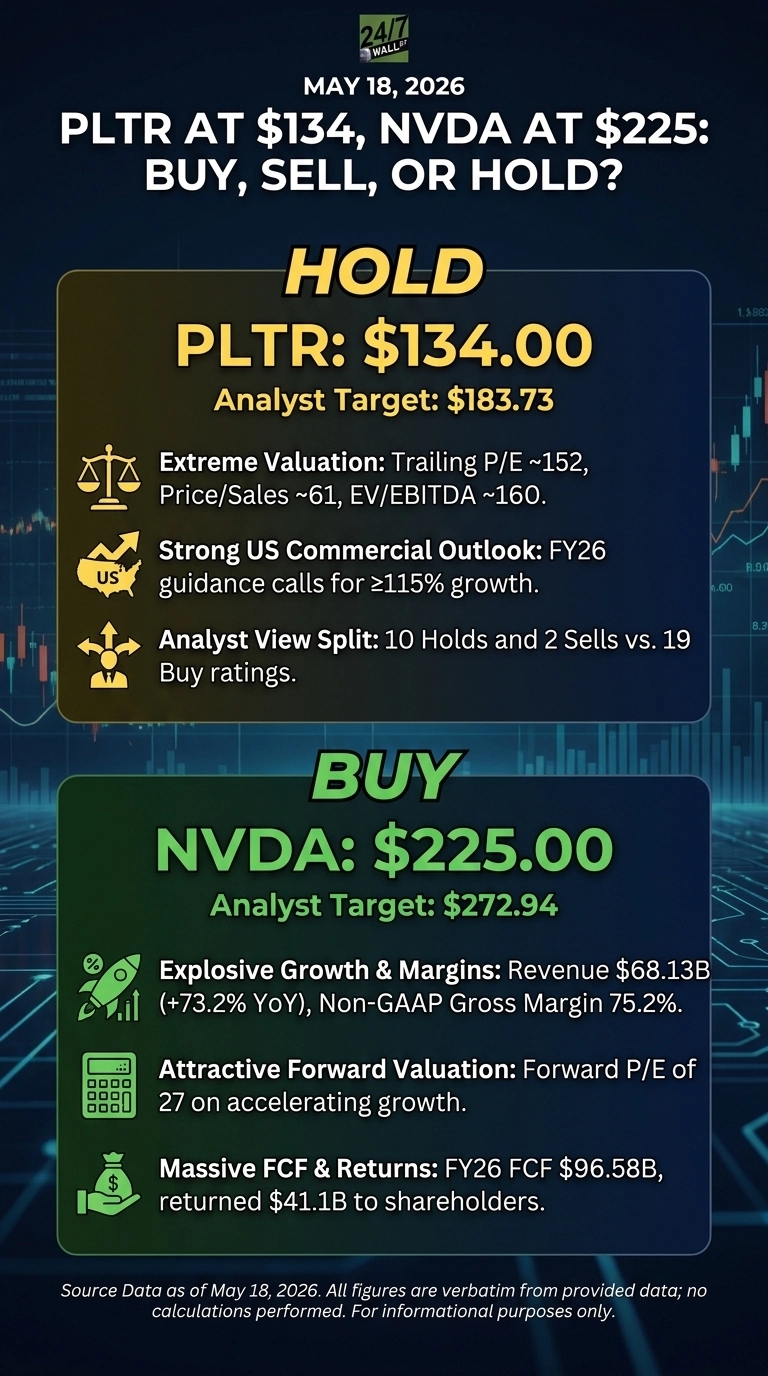

NVIDIA’s most recent quarter delivered $68.13B in revenue, up 73.2% YoY, with Data Center hitting $62.31B (+75%) and Networking up 263%. FY26 free cash flow reached $96.58B, and management returned $41.1B to shareholders. A forward P/E of 27 on accelerating growth is rare at this scale.

Palantir posted Q1 FY26 EPS of $0.33, beating the $0.28 estimate, extending six beats in eight quarters. FY26 guidance calls for revenue of $7.182 to $7.198 billion (61% YoY growth) with U.S. commercial up at least 115%. The pullback from $207 to $134 offers a cheaper entry into a software story still compounding rapidly.

Where the bear thesis bites

Palantir trades at a trailing P/E near 152, price/sales of 61, and EV/EBITDA of 160. Even strong execution leaves little room for error. Stock-based compensation of $684M for FY25 and customer concentration in terminable government contracts add risk.

For NVIDIA, the Q1 FY27 guide explicitly excludes any Data Center compute revenue from China, and a $4.5B H20 charge showed how export rules can bite. Supply constraints, gross margin pressure, and $95.2B in supply commitments raise stakes if AI capex cools.

The case for holding Palantir

Palantir’s growth is real, but valuation dominates at these levels. The 50-day moving average sits at $144.40 against a 200-day of $163.35, and the consensus analyst target of $183.73 is above today’s price but below the February peak. With 10 Holds and 2 Sells against 19 Buy-side ratings, the Street is split. The next quarter’s U.S. commercial growth versus the 115% bar is the cleaner trigger.

How the numbers stack up

PLTR trades near $133.99 against a consensus target of $183.73, implying roughly 37% upside across about 31 analysts. NVDA trades near $224.41 with a target of $272.94, about 22% upside, and 58 of 61 analysts rate it Buy or Strong Buy.

NVIDIA is up 18.83% YTD and 65.53% over one year, versus the S&P 500 at roughly 8.2% YTD and 25.2% over one year. PLTR has lagged the index year-to-date after its February drawdown.

The verdict at these prices

At $134, Palantir screens as fully valued. The business executes, but the multiple embeds aggressive forward growth, and the chart shows distribution between the $166 support and $190 resistance bands. Wait for either sustained reacceleration above 115% U.S. commercial growth or a deeper reset toward the moving averages.

At $225, NVIDIA screens favorably on the fundamentals. Forward earnings of 27x on revenue compounding above 70% with 75.2% non-GAAP gross margins and $96.58B in FCF is a clean setup.

The Q1 FY27 guide excludes China, so the bar is conservative, and Blackwell-to-Rubin demand from Meta, Anthropic, and hyperscalers point to multi-year visibility. China policy and supply shocks are thesis-breakers to watch.

Palantir’s story is intact, but its price is doing the heavy lifting; NVIDIA’s price matches the fundamentals.

Contact [email protected] for any questions or corrections.