I keep adding to my position in Alphabet (NASDAQ:GOOGL | GOOGL Price Prediction), and the July 22 earnings report will reinforce the trade. What earns my capital, quarter after quarter, is one specific proof point: Google Cloud has quietly turned into the fastest-growing hyperscaler on Earth, and the market is still pricing this company like a search company with an AI problem rather than an AI company with a search franchise attached.

The Cloud Number That Keeps Me Buying

In Q1 2026, Google Cloud revenue grew 63% year-over-year to $20 billion, while Microsoft Azure grew 40% and Amazon AWS grew 28% over the same period. That gap is the whole thesis in one line. Backlog nearly doubled sequentially to $462 billion, and CFO Anat Ashkenazi told investors “just over 50% of the backlog” converts to revenue over the next 24 months. Revenue from products built on Alphabet’s generative AI stack, meanwhile, grew nearly 800% year-over-year. This is enterprise AI at scale, sold by the only vendor that owns the silicon, the models, and the distribution.

Cloud operating income tripled to $6.6 billion, with segment margin expanding to 32.9% from 17.8%. High-margin growth is the phrase I keep circling in my notes.

The Rest of the Business Is Keeping Pace

Consolidated revenue hit $109.90B, up 21.8% year-over-year, with operating margin at 36.1%. EPS of $5.11 versus a $2.63 estimate was the fourth consecutive EPS beat. Search revenue grew 19% to $60.4 billion with queries at an all-time high. And 350 million paid subscriptions gives me a recurring-revenue base that did not exist five years ago. The company just raised the dividend 5% to $0.22 per share, which is still a token yield, but the direction of travel matters.

Why Not Microsoft or Amazon

I own the other names too. I am not buying them here. Microsoft’s Azure is growing at 40%, and Amazon’s AWS at 28%. Both are excellent businesses. Neither is compounding cloud revenue at 63%, and neither trades at Alphabet’s forward multiple. GOOGL sits at a forward P/E of 25 with return on equity of 38.9%. That is a growth-cloud business priced like a mature ad platform. I will take that mispricing every time.

The Risk I Actually Take Seriously

Capex more than doubled, up 107.44% year-over-year to $35.67B, pushing free cash flow down 46.63%. Full-year 2026 capex guidance now sits at $180 billion to $190 billion, and management expects 2027 CapEx to significantly increase. If AI demand softens, this spend becomes a stranded asset conversation. What holds the thesis together for me is that Cloud is “compute constrained” at these growth rates. You do not spend $185 billion when demand is a mystery. You spend it when the backlog is $462 billion and doubling.

The Forward Case

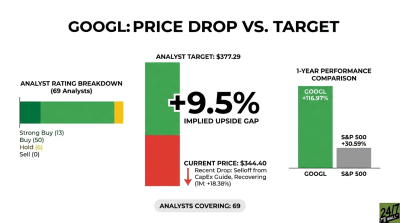

Analyst consensus sits at 57 buys, 7 holds, zero sells against a target of $431.72. The stock is up 94.28% over the past year and still trades below its 52-week high of $408.37. I am buying a compounder that owns the full AI stack, prints $45.79 billion in quarterly operating cash flow, and just raised its dividend for the second time. The July 22 report is a checkpoint on a position I intend to keep adding to for years.

Contact [email protected] for any questions or corrections.