The F.I.R.E. principle stands for Financial Independence Retire Early. At its core, it’s about calculating roughly 25 times one’s expenses, and then saving and investing enough to reach that sum and have passive income from which to maintain the desired lifestyle to pursue other interests. It is a solidly sound financial planning strategy that is a stark contrast to rampant spending and debt cycles that plague a large segment of the population. Although it may involve a lot of sacrifice and scrimping in the early years, the benefits to be enjoyed later on are well worth it for many. The wealth generated through F.I.R.E. adherence can give families a lot more options than those families who have not chosen to engage in it.

However, an early retirement should not automatically mean a total withdrawal from the workforce, especially for those who still have a decade or more of productive years ahead of them.

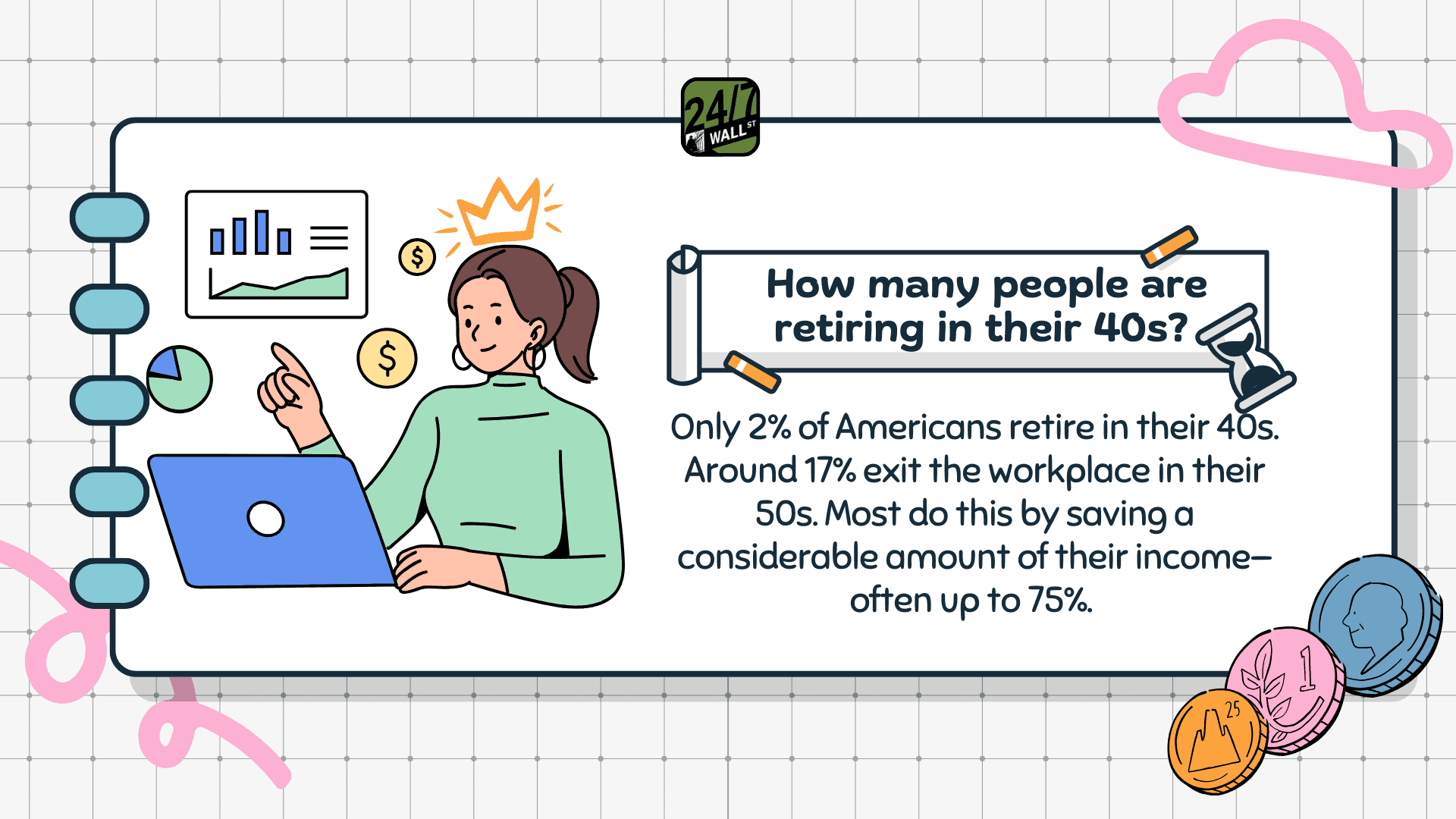

F.I.R.E. Success – But Is Retirement Advisable at Age 40?

The Financial Independence Retire Early strategy can build substanital wealth while one is still young enough to enjoy other pursuits.

If someone has successfully deployed the F.I.R.E. strategy to amass a nearly 8 figure net worth by the age of 40, the retire early portion of F.I.R.E. can be very tempting. A Reddit poster who came from an impoverished background went from sneaking condiments home from his workplace cafeteria to a successful career and a $9.5 million net worth. As a 40-year old married father of a 2-year old, his wife has already retired to care for the baby, and he is thinking of following her, as a result of new policies at his job to which he objects. His details are as follows:

- Current job in tech pays $300,000 per year and is very easy for his skill-set, while his final results continue to wow his peers and management.

- The new policies require more office time than previously, and he has little enthusiasm for his latest assigned project, which will likely take up more time away from his family than he would like.

- His family currently rents its home in a downtown urban area.

- His net worth is $7 million post-tax and $2.5 million pre-tax. No details on his investments or retirement plan are disclosed.

He says he is 95% leaning towards also joining her in retirement, but asks for other opinions.

Occupation Measures to Consider

Freelance work can be a well paying alternative for those in the tech industry who prefer remote work.

From my perspective, I think that a complete withdrawal from the workplace at age 40 can be dangerous, especially if a sudden medical or personal disaster drains the family’s nest-egg and he has been out of circulation for several years. Since he seems to generally enjoy his work but prefers the flexibility of remote work, I might suggest the following:

- Before quitting the current job, try speaking to some recruiters who specialize in tech personnel with high demand skill sets, perhaps from competitors of the current employer. Offers may come in from companies who are more flexible on remote work and may offer even higher compensation.

- If the poster does not already have a LinkedIn presence, I would advise creating one and commence networking with others in the tech industry to gauge the demand for his skills in the marketplace and the kind of projects requiring them. If a regular job is too restrictive, freelance opportunities may offer both more intellectual challenges, as well as more lucrative payment.

- To maintain the current lifestyle, more than $300,000 annually will be required, as raising a child to age 18 can cumulatively cost more than what the poster has calculated. Having active income throughout his 40’s and 50’s are statistically the years where he can earn the most.

- The poster admits to having an impoverished childhood. While $9.5 million sounds like a lot, taxes and other unforeseen expenses can quickly erode it unless it is prudently managed and can generate sufficient passive income to render tapping the principal unnecessary.

Investment Measures to Consider

- Since it is undisclosed, I am assuming that the $2.5 million pre-tax is in a tax deferred retirement account, i.e., a 401-K or IRA. Given that the poster is only 40, a growth oriented strategy with diversification to mitigate risk would be advised.

- A portion of the unencumbered $7 million should wisely be invested in a real-estate based asset for solid, dependable passive income, in the event that the poster decided to go the retirement route. If he wishes to be a passive real estate investor, there are numerous REITs with long track records that can be considered.

- If the poster does retire early, he will be responsible for his family’s health care after COBRA term expires, so additional passive income or medical insurance from a new employer will be required to cover those costs.

The above comments are solely opinions, and not to be construed as financial advice. Should financial planning for retirement or other types of counseling be desired, professional advisors should be sought.

Contact [email protected] for any questions or corrections.