The cost of a college education has become genuinely staggering. The debt burden students carry is, in large part, a product of overly abundant government grants and loans operating through a well-documented economic mechanism called the passthrough rate.

According to the Federal Reserve Bank of New York, for every $1 increase in the maximum amount of federally subsidized student loans, college tuition rises $0.60. The logic is simple: more federal money flowing into higher education gives colleges cover to raise prices, because students can borrow more to pay them.

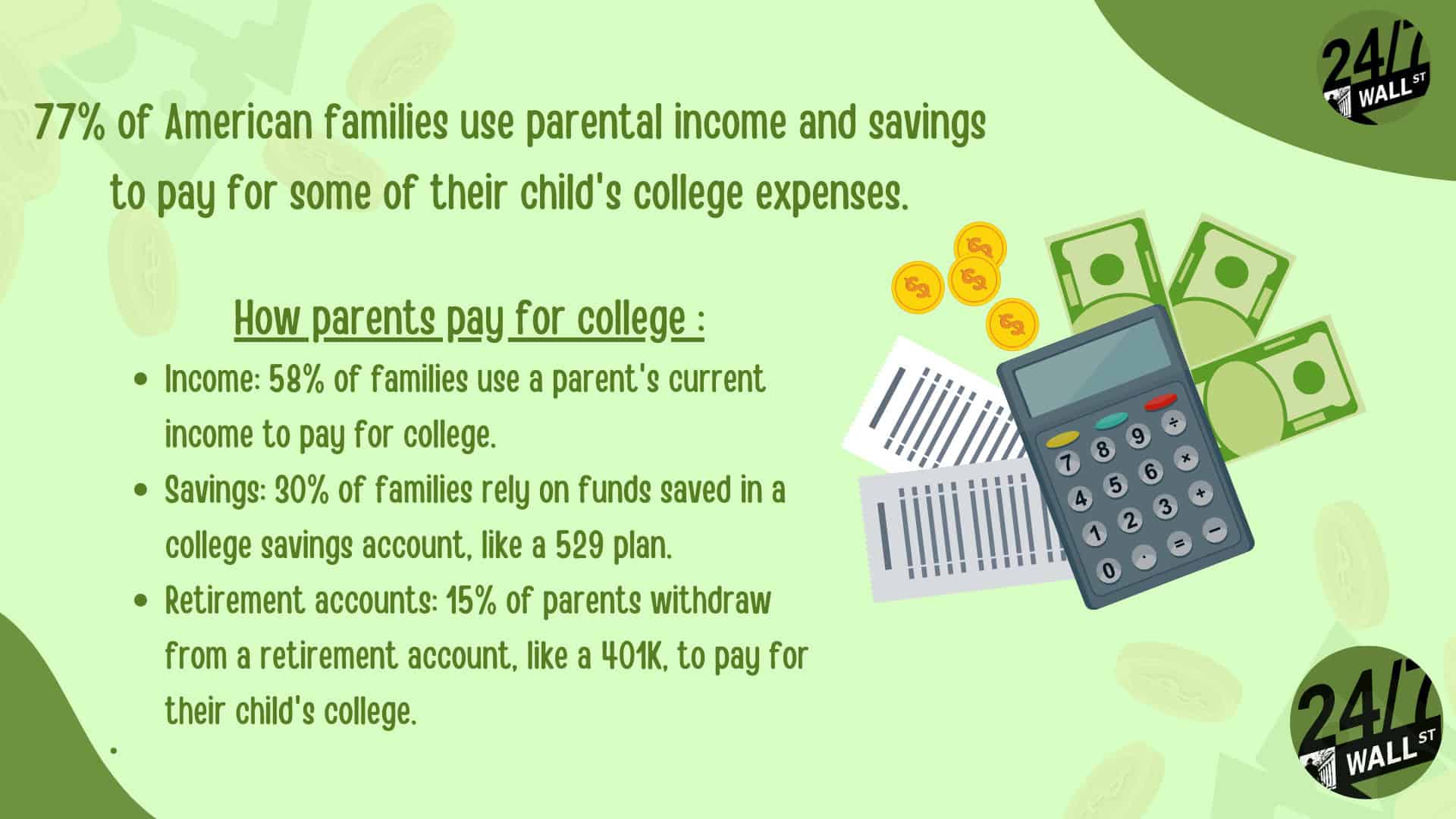

Americans now owe $1.87 trillion in federal and private student loan debt as of the first quarter of 2026, up 3.3% from a year earlier, spread across roughly 43 million borrowers. That total ranks as the second-largest category of consumer debt in the country, behind only mortgages. The weight of it saps the financial security of students and parents alike, and more families are now asking whether it still makes sense for parents to foot the bill for a child’s education at all.

That question was front and center for a Redditor on r/DaveRamsey, a community built around the personal finance principles of Dave Ramsey. The poster did not want to undermine his child’s opportunities, but he also could not ignore the damage that more debt would do to his own already precarious finances.

24/7 Wall St. Key Points:

- The ever-rising cost of college tuition has bankrupted the future of children and parents alike, with national student loan debt climbing to $1.87 trillion.

- Parents often find themselves choosing between paying for college and financing their retirement, a dilemma compounded by strict new borrowing caps.

- Prioritizing college over retirement planning can foster a child’s sense of entitlement while potentially ruining the chance for a secure financial future for both.

The 2026 Reality: Gen X Is Bearing the Brunt

The standard advice to start saving for a child’s college education at birth, typically through a 529 plan, deserves more scrutiny than it usually gets. Contributions to a child’s education fund should never come before maximizing your own retirement savings. Department of Education data through December 2025 shows that borrowers aged 35 to 49 now hold $681.5 billion in federal student loan debt, the largest share of any age group. That burden lands precisely during the years when wealth accumulation matters most.

If you have not fully maximized every retirement option available to you, a child’s education savings should come second. Footing the entire college bill is an increasingly costly choice, and one that can actively undermine the child’s own sense of financial responsibility. The Class of 2024 left school with an average of $29,560 in federal and private student loan debt, a figure that sounds manageable until interest begins compounding on a modest starting salary.

The Redditor in question was divorced, paying alimony, carrying significant debt, and still working to stabilize his own finances. He wanted a bright future for his child, and that impulse is admirable. The most valuable conversation he could have had would have started years earlier, with an honest discussion about the real cost of college and the limits of what parental support can realistically cover. Shifting the focus from parental funding to individual responsibility is not abandonment. It is preparation.

The Parent PLUS Trap Just Got Tighter

For parents weighing whether to borrow on a child’s behalf, the regulatory landscape shifted dramatically when President Trump signed the One Big Beautiful Bill Act into law on July 4, 2025. Under that legislation, Parent PLUS loans taken out on or after July 1, 2026 are capped at $20,000 per year per dependent student and $65,000 in total per dependent student. These limits are combined across all parents of a given student, meaning two parents cannot each borrow $20,000 for the same child. Previously, parents could borrow up to a school’s full cost of attendance with no hard cap. The same legislation also eliminated the Graduate PLUS Loan program for new borrowers beginning July 1, 2026, further tightening the federal credit available to families.

The repayment landscape changed just as sharply. For new loans disbursed on or after July 1, 2026, SAVE, PAYE, and ICR no longer accept new enrollments; those three plans sunset entirely by July 1, 2028. New borrowers after that date have two options: the new Repayment Assistance Program (RAP) or the new Standard Repayment Plan. Borrowers who took out loans before July 1, 2026 can remain on their current plan, switch to IBR, or opt into RAP voluntarily. Adding another wrinkle, new Parent PLUS loans disbursed after July 1, 2026 are not eligible for income-driven repayment at all. That combination of a hard borrowing cap and stripped-down repayment options adds substantial risk for any parent signing onto federal debt now.

The opportunity cost of carrying that debt is worth spelling out plainly. A $100,000 parent loan balance on a 25-year standard repayment schedule runs roughly $770 a month in cash outflows. That same $770 a month invested over 25 years at a historically average 8% market return would grow to more than $730,000 in a retirement portfolio. The math alone should give any parent pause before signing on the dotted line.

Better Alternatives to Sacrificing Your Retirement

Breaking this cycle starts with expanding the menu of options students explore. Scholarships, grants, work-study arrangements, and part-time employment can meaningfully reduce the gap between what a family can afford and what a school costs. Since 2024, SECURE 2.0 has allowed employers to match an employee’s qualified student loan payments with contributions directly into that employee’s 401(k), giving borrowers a path to build retirement savings even while paying down debt. Large employers including Kraft, Workday, and Comcast were early adopters of the provision, and the practice has grown steadily. For households with compressed cash flow, a well-constructed FAFSA financial aid appeal letter can also unlock additional institutional aid that a standard application misses.

If a parent decides to help, a cleaner approach is to have the student take on federal student loans directly, which carry more repayment flexibility than Parent PLUS, while the parent contributes to the monthly payment as a third party. The parent never owns the primary debt. Beyond the loan question itself, a four-year private university is not the only path to a quality credential. Community college followed by a transfer to a four-year institution can cut total borrowing sharply, and the financial headroom that creates gives a young graduate a meaningful head start on building their own savings.

Do Not Sacrifice Your Financial Future

Investing in a child’s future ultimately means raising a financially capable adult. Vocational training, apprenticeships, and trade certifications all offer documented wage premiums and, critically, far less debt than a four-year degree. A parent who helps their child find that path is doing something more valuable than writing a tuition check.

The conversation about college costs should begin long before a college application is filed. When children grow up understanding that college is an investment with a real price tag and real consequences, they approach it with more seriousness and more strategy. Parents who choose not to go into debt for a child’s education are not failing their kids. They are modeling exactly the financial discipline they want their children to develop.

Editor’s note: The repayment section has been corrected to clarify that under the One Big Beautiful Bill Act, it is SAVE, PAYE, and ICR that stop accepting new enrollments on July 1, 2026 (sunsetting by July 1, 2028), while IBR remains available for pre-July 2026 borrowers. The section also now reflects that new Parent PLUS loans disbursed after July 1, 2026 are not eligible for income-driven repayment, and that the $20,000 annual Parent PLUS cap is a combined limit across all parents of a given student. The average debt figure for the Class of 2024 ($29,560) has been added, sourced from LendingTree.

Contact [email protected] for any questions or corrections.