A Reddit user recently posed a question that resonates with a lot of high-earning savers: at what point does contributing to a 401(k) become unnecessary because compound growth alone can handle the heavy lifting?

The 44-year-old poster has already accumulated $1.3 million and plans to retire at 59 1/2. He noted that even maxing out his contributions would represent just 1% of his account’s expected annual growth. His goal is clear: generate at least $100,000 per year in retirement income. Can he coast from here, or does stopping early carry hidden costs?

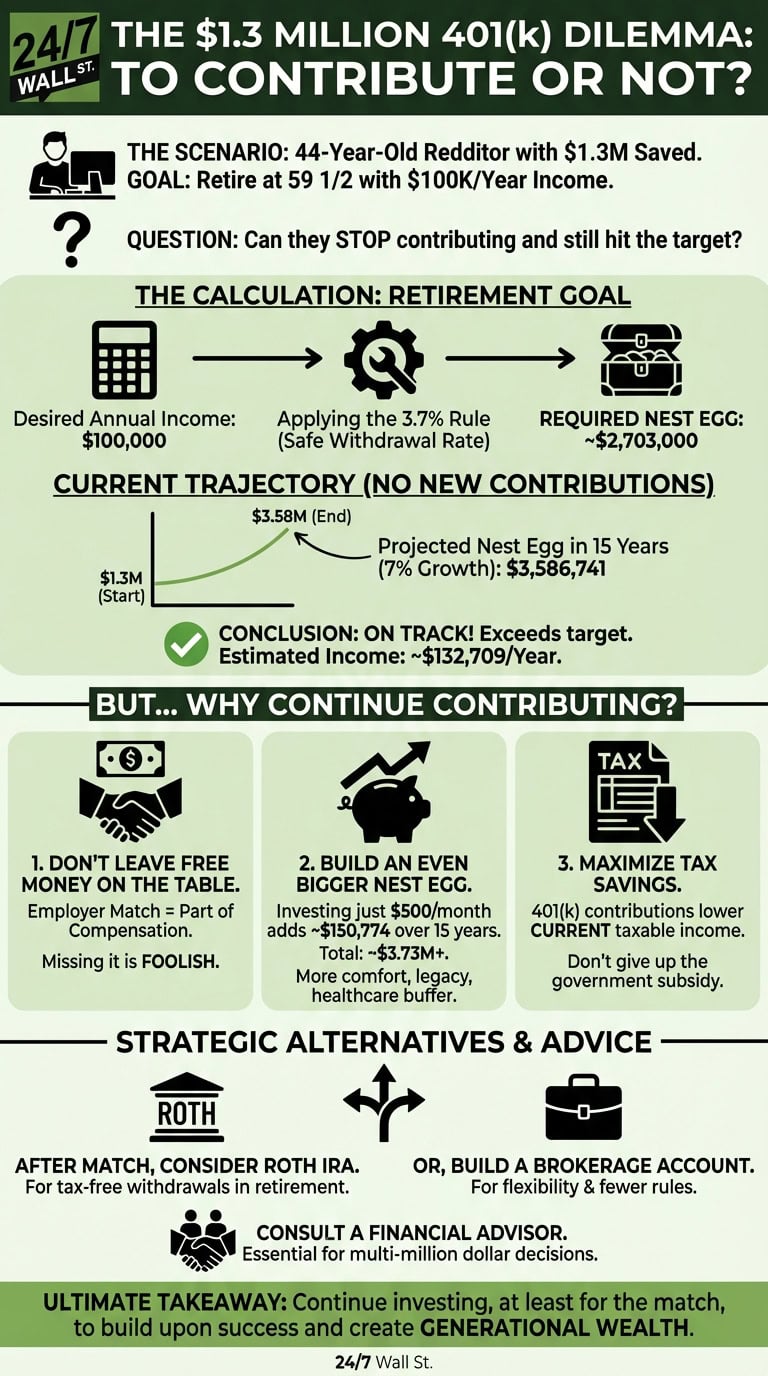

The answer hinges on how much he actually needs at retirement and what he gives up by stepping back now.

Calculating the retirement target

Before deciding whether to halt contributions, you need to know your finish line. How much wealth does it take to safely produce $100,000 per year in retirement without depleting the principal?

Financial planners have long referenced the 4% rule, which caps first-year withdrawals at 4% of the portfolio balance. That guideline continues to evolve. Morningstar’s 2025 “State of Retirement Income” report, published in December 2025, recommends a 3.9% starting withdrawal rate for retirees seeking steady, inflation-adjusted spending over a 30-year horizon. That is a modest improvement from the 3.7% rate the firm published in 2024, driven by updated capital-market assumptions. For retirees willing to accept some variability in annual spending, Morningstar found that flexible withdrawal strategies (such as a guardrails approach paired with delayed Social Security and Treasury Inflation-Protected Securities) can support a starting rate as high as 5.7%.

Using the conservative 3.9% benchmark, you would need roughly $2.56 million to generate $100,000 annually. If this Reddit user’s $1.3 million grows at a 7% average annual return for 15 years with no additional contributions, the projected balance comes to approximately $3.59 million. That comfortably exceeds his target and would support around $140,000 in annual retirement income at a 3.9% withdrawal rate. One important wrinkle: the 3.9% figure assumes a 30-year spending horizon. Someone retiring at 59 1/2 and living into their 90s could face a horizon of 35 years or more, which argues for a somewhat more conservative initial withdrawal rate. Morningstar’s own research notes that retirees with a 20-year horizon can reasonably spend more than 5% of a balanced portfolio, providing useful context for how the math shifts as time horizons change.

On paper, stopping contributions now still gets him to his goal. But that narrow calculation misses several important considerations.

Why you might want to keep contributing anyway

The first reason to keep contributing is employer matching. Walking away from employer match dollars means forfeiting part of your total compensation. Unless the deferrals genuinely strain your budget, leaving that money on the table is one of the costliest mistakes a well-positioned saver can make.

The second reason is cushion. Contributing just $500 per month over the next 15 years at a 7% return would push the projected balance to roughly $3.89 million instead of $3.59 million, before factoring in any employer match. That extra $300,000 provides flexibility for unexpected healthcare costs, a bad market in the early years of retirement, or a larger inheritance. Sequence-of-returns risk, the danger that a downturn hits right after you stop working, makes that buffer more valuable than the raw number suggests.

The third reason is the immediate tax advantage. Every dollar deferred reduces current taxable income. Stop contributing and your tax bill rises, which means redirecting money to the IRS rather than a growing retirement account. For someone already in a strong savings position, that trade-off rarely makes sense.

Alternative strategies beyond the 401(k)

Continuing to save does not mean pouring everything back into your 401(k). Once you have captured your full employer match, other accounts may offer better advantages depending on your situation. For reference, the 2026 401(k) employee deferral limit is $24,500, up from $23,500 in 2025, leaving meaningful room to maximize the account if you choose. Workers aged 60 through 63 can contribute an even higher catch-up amount under SECURE 2.0 rules.

A Roth IRA, if you qualify based on income, provides tax-free withdrawals in retirement. For 2026, single filers with modified adjusted gross income below $153,000 and married filers below $242,000 can contribute the full $7,500 annual limit ($8,600 for those 50 or older). Building a Roth alongside a traditional 401(k) creates valuable tax diversification, giving you more control over your retirement tax bill by letting you draw from pre-tax and after-tax buckets strategically.

A taxable brokerage account is worth considering as well. Unlike retirement accounts, brokerage holdings carry no withdrawal restrictions or required minimum distributions, providing full liquidity and a broad range of investment choices. If the 401(k) already covers core retirement income needs, steering additional savings into a brokerage account can fund pre-retirement goals or serve as bridge income for someone who wants to retire before 59 1/2 without triggering early-withdrawal penalties.

A financial advisor can help weigh these options, particularly once a portfolio crosses seven figures. At that scale, decisions around tax strategy, asset location, and withdrawal sequencing can translate into tens of thousands of dollars over a retirement spanning three decades or more.

The case for staying invested

The original poster’s math does hold up. Stopping contributions entirely and relying on 15 years of compounding still gets him to his $100,000 income goal. But doing so means forfeiting employer match dollars, a larger safety margin, and meaningful annual tax savings.

At minimum, contributing enough to claim the full employer match is a straightforward win. Beyond that, a Roth IRA, taxable account, or additional 401(k) deferrals can each serve a distinct purpose in a well-structured plan. Retirement planning is about more than hitting a number. Building resilience against market volatility, optimizing taxes across multiple account types, and preserving options for the unexpected all matter as much as the projected balance. Someone already on track has a rare advantage: the ability to use it to build not just enough, but a genuine foundation for financial independence.

Editor’s note: This pass added Morningstar’s December 2025 publication date for its “State of Retirement Income” report, incorporated the research finding that retirees with a 20-year horizon can reasonably spend more than 5% of a balanced portfolio, noted the SECURE 2.0 enhanced catch-up contribution rule for workers aged 60 through 63, and clarified that the Roth IRA income phase-out for singles begins at $153,000 for 2026.

Contact [email protected] for any questions or corrections.