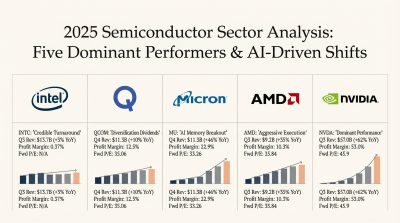

Shares of Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) are pulling back slightly midday Thursday, but the stock’s run over the past month has been historic. AMD stock is up 55% over the past month, compared with just 17% for Intel (NASDAQ:INTC) stock. That kind of gap raises a fair question for Intel’s loyal shareholders.

Should Intel stockholders rotate into AMD now? The math is more complicated than a one-month chart suggests. Year to date, Intel is actually beating AMD, up 205% versus 148% for AMD.

Both names are riding the AI infrastructure wave, but their stories look very different right now. Here’s what’s powering the divergence, and what investors should think about before reallocating their exposure.

AI Data Center Demand Powers AMD’s Breakout

Advanced Micro Devices reported Q1 2026 revenue of $10.25 billion, up 38% year over year (YoY), with non-GAAP EPS of $1.37 beating the $1.29 consensus. Furthermore, the company’s Data Center revenue hit $5.78 billion, up 57% YoY.

CEO Lisa Su declared, “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.” Meta Platforms (NASDAQ:META) committed to deploying up to 6 gigawatts of AMD Instinct GPUs, and OpenAI announced a similar 6 GW partnership.

Advanced Micro Devices’ Q2 2026 guidance calls for revenue near $11.2 billion, implying 46% YoY growth, with gross margin near 56%. That’s a notable acceleration profile for a company of AMD’s scale, and it helps to explain why the news sentiment around the name remains constructive.

Intel’s Turnaround Is Real, Just Slower

Intel posted Q1 2026 revenue of $13.58 billion, up 7% YoY, with non-GAAP EPS of $0.29. Moreover, Intel’s Data Center and AI revenue grew 22% YoY to $5.05 billion.

That’s solid progress, but AMD’s Data Center segment is now nearly as large as Intel’s entire DCAI business and growing more than twice as fast. Intel CEO Lip-Bu Tan is executing a credible reset, with a sixth consecutive quarter of revenue above expectations.

Intel also locked in a $5 billion NVIDIA (NASDAQ:NVDA) equity investment and a multiyear CPU and ASIC collaboration with Alphabet‘s (NASDAQ:GOOGL) Google. The Intel 18A ramp could be a meaningful catalyst, but the gap with AMD in AI accelerators remains wide.

The Valuation and Sentiment Tell a Cautious Story

AMD stock trades at a P/E ratio of 173x, with a market cap of $863.2 billion versus Intel at $542.5 billion. AMD analysts carry 41 Buy ratings with a consensus target of $479.77, sitting below the current price near $529.38.

Reddit sentiment for AMD stock sits at 28 (bearish), with the top retail post titled “AMD’s price has massively detached from forward earnings expectations.” That’s a notable disconnect from the rally.

Intel stock’s analyst consensus target of $88.71 implies 21% downside from current levels. Both stocks look stretched after huge year-to-date runs.

What to Watch Next

Investors should be cautious about chasing AMD stock purely off the one-month move. The fundamentals support a premium valuation, yet analyst targets on both names sit below current prices, and retail sentiment is unusually skeptical given the price action.

Intel shareholders sitting on a triple-digit year-to-date gain don’t need to rush a full rebalancing. A more cautious approach could involve sizing measured exposure to both names rather than rotating one’s entire position into AMD based on a one-month chart.

Watch for Advanced Micro Devices’ MI450 ramp commentary and Intel’s 18A volume numbers next quarter. Those data points could reset both stories, and they’re the moments that may decide whether this month’s gap widens or starts to close.

Contact [email protected] for any questions or corrections.