Finance expert Suze Orman had some important commentary about New Year’s Resolutions that everyone should read as 2026 approaches.

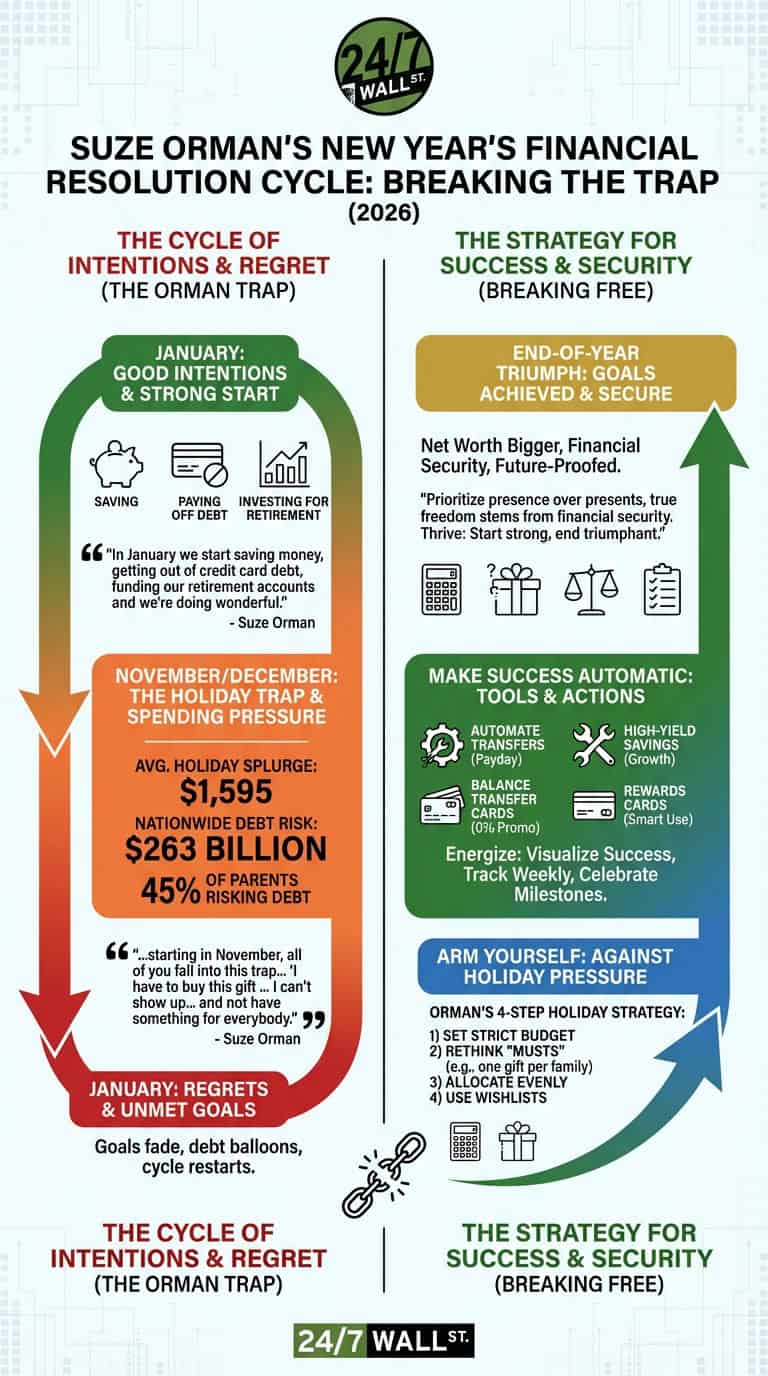

Orman said, “In January we start saving money, getting out of credit card debt, funding our retirement accounts and we’re doing wonderful. Then, every single year like clockwork, starting in November, all of you fall into this trap that says, ‘I have to buy this gift … I can’t show up at this party and not have something for everybody.”

Orman’s words were a warning about how we all start the year with good intentions, but then reality gets in the way. This does not have to happen to you, though. You can set financial goals for the New Year, stick to them, and actually end the year richer. You just need to set the right goals and understand the pitfalls that prevent most people from achieving financial success.

Are your resolutions on Orman’s list?

When talking about January goals, Orman listed a number of things that many people often do to start off the year right. She said that many people begin by:

- Saving

- Paying off credit card debt

- Investing for retirement

While your own situation should dictate what your New Year’s resolutions are, any one of the goals on this list would likely be a good one for most people.

If you owe money on your credit cards, paying it off should most likely be a top priority as the costs of carrying a balance are too high, with the Federal Reserve reporting the average interest rate at 21.39%. Investing — especially enough to earn your full employer match — is also important if you don’t want to end up a broke retiree as Social Security only replaces about 40% of pre-retirement income. And, short-term savings can help you avoid debt that adds to your costs.

Now, you may want to adopt these specific resolutions, but you can also make your own as well — such as saving for a house or finally getting control of your student loan debt. Whatever you decide, the key is to go into January with some very concrete financial goals you are excited about — if you want to improve your finances meaningfully in the new year.

Don’t let your goals fade away unfinished

Orman wasn’t just suggesting some good New Year’s Resolutions when she mentioned starting January off right. She was warning that while you may go into the year with good intentions, you’ll often forget about them quickly and find ways to justify not following through.

You don’t want that to happen, though, or you could get to December and find yourself full of regrets. To avoid that, try to make the process of achieving your goals as automatic as you can. For example, if you’re paying off credit card debt or investing more, set up automated money transfers to your credit cards and your bank account on payday.

You can also use the right tools to help you achieve your goals. For example, a high-yield savings account could make it easier to begin saving and grow your account balance. Or, using a balance transfer credit card and moving your debt from an expensive card to one offering a promotional o% rate could make debt payoff much easier. The right credit card can also help you keep interest costs down if you must carry a balance and can help you earn generous rewards that make purchases cheaper.

If you automate the process and make effective use of these financial tools, you can start off January doing wonderfully, as Orman says — but you can also finish the year with your goals achieved and your net worth a little bigger. Prioritize presence over presents, true freedom stems from financial security. Thrive: Start strong, end triumphant, future-proofed.

Contact [email protected] for any questions or corrections.