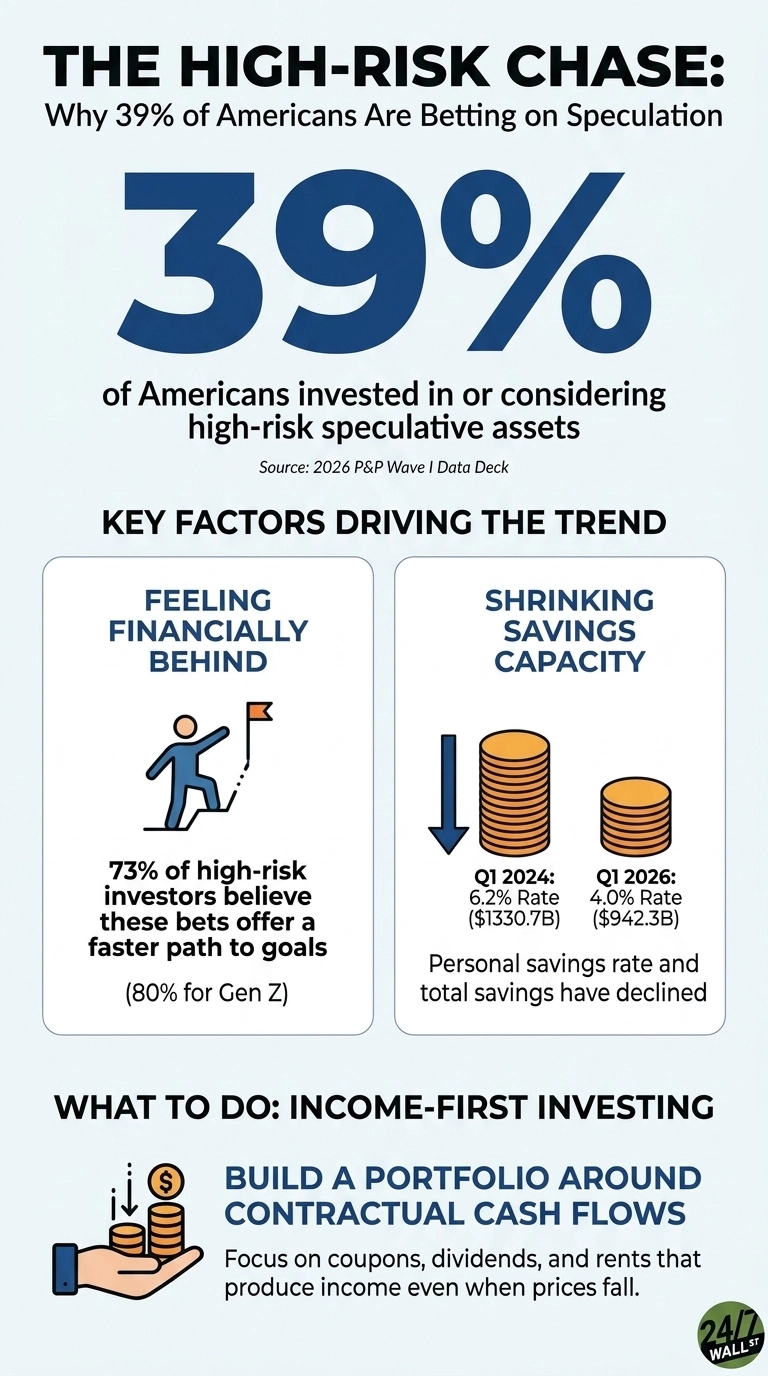

Something interesting is happening inside the Northwestern Mutual 2026 Planning & Progress Study data that does not resolve cleanly. More Americans feel financially secure today than at any point in recent years, with the share reporting confidence in their financial lives climbing meaningfully from the prior year. At the same time, roughly four in ten Americans are either invested in or actively considering high-risk speculative assets, including prediction markets, sports betting, and cryptocurrencies. Stated confidence is rising, and so is the willingness to pursue outcomes that carry no contractual claim to future cash flow. This trend persists even as the national Personal Prosperity Index sits at a resilient 68 out of 100, suggesting a sharp divide between personal stability and macro-economic anxiety.

The survey documents the motivation behind that apparent contradiction, and the explanation is worth sitting with. Among those pursuing speculative assets, nearly three-quarters say they are doing so because they feel financially behind and believe these bets offer a faster path to their goals than traditional methods. Among Gen Z, that figure climbs to eight in ten. Researchers have begun calling the pattern financial nihilism—a response to a world where the “magic number” for retirement has surged to $1.46 million in early 2026. This belief suggests that conventional saving simply cannot close the gap fast enough, making a low-probability, high-payoff swing feel like the only logical play available.

Why the Math Feels Broken

The frustration behind that belief is not imaginary, and the report data helps explain where it comes from. Inflation ranks as the single biggest obstacle to financial security for more than four in ten Americans, well ahead of concerns such as lack of savings, personal debt, and healthcare costs. The squeeze is visible in the data: the personal saving rate fell to 3.6% in the most recent Bureau of Economic Analysis release, a decline from the 4.0% seen earlier in the quarter. When the gap between what things cost and what people earn keeps widening despite working and saving, the logic of slow and steady starts to feel less convincing.

Consumer sentiment reflects the same squeeze. The share of Americans who expect the economy to weaken in 2026 outnumbers those who expect improvement, and that pessimism cuts across generations. This is compounded by a “confidence gap” where even 49% of millionaires report their financial plans need improvement. Gen Z and Millennials are feeling it most acutely, which helps explain why those cohorts are the most likely to describe their speculative activity as a response to falling behind rather than a considered portfolio decision. When the baseline feels broken, the appeal of a faster solution grows regardless of the odds attached to it.

The Planning Gap Inside the Portfolio

The same survey identifies a structural blind spot beneath the speculative behavior and connects the two patterns in a way that matters. More than half of Americans acknowledge they place too much emphasis on building and growing assets without adequately protecting them or managing risk. However, the nature of these assets is shifting; as Bitcoin tests the $80,000 psychological barrier in May 2026, the line between “gambling” and institutional asset class adoption via spot ETFs continues to blur. A portfolio tilted entirely toward upside remains risky, but the institutionalization of crypto is forcing a re-evaluation of what constitutes a “speculative” asset in a modern framework.

The discipline trend in the same report runs in the opposite direction and deserves equal weight. The share of Americans who describe themselves as disciplined financial planners has climbed to a majority in 2026. Data shows that 71% of people working with financial advisors feel secure compared to those without, likely because they utilize the “Advisor Advantage” to navigate volatility. These households tend to pair contribution targets with protection layers, automate savings decisions, and maintain a plan for what to do when markets fall. The gap between that group and the speculative cohort is a framework gap that is becoming the defining characteristic of financial success in 2026.

Why Income-First Holds Up Better

Income-first investing offers a fundamentally different structure for someone who genuinely feels behind, and the case for it does not require dismissing the frustration behind financial nihilism. Dividends, coupons, and rental income arrive on a schedule and can be reinvested at whatever rates the market offers, which is the engine of compounding that speculative assets cannot replicate. A portfolio built around contractual cash flows yields a measurable metric even when prices fall, and it provides a “Prosperity Index” of one’s own to track progress against, regardless of macro volatility.

The real cost of a speculative bet gone wrong is not just the capital lost; it is the income that was never built in its place and the compounding that never started. Gen Z sits on the longest investment horizon of any working generation, yet they are the most susceptible to the “catch-up” trade mindset. By shifting the focus from price appreciation to contractual cash flow, investors can bridge the gap between their current standing and the $1.46 million retirement threshold without relying on the low-probability swings that define financial nihilism.

Editor’s Note: This article has been updated with May 2026 economic data, including the new $1.46 million retirement “magic number,” the decline in the BEA personal savings rate to 3.6%, and the introduction of the Personal Prosperity Index. Further context was added regarding the institutionalization of cryptocurrency and the statistically significant security gap between advised and unadvised investors.

Contact [email protected] for any questions or corrections.