The Iran war started on February 27, and the aluminum market has not been the same since. Alcoa CEO William Oplinger told investors on the company’s Q1 2026 call that London Metal Exchange prices had recently exceeded $3,600 per metric ton on tight inventories and Middle East supply disruptions. Reuters dubbed it a shock that has “rattled the global aluminum supply chain.” For the average American investor holding almost nothing in commodities directly, the question is whether to do anything about it. Kiplinger’s answer, laid out in its May 12 piece on inflation-hedging ETFs, is yes: a small, diversified commodity sleeve can blunt the inflation passthrough that wartime metal shocks produce.

The price move investors keep underestimating

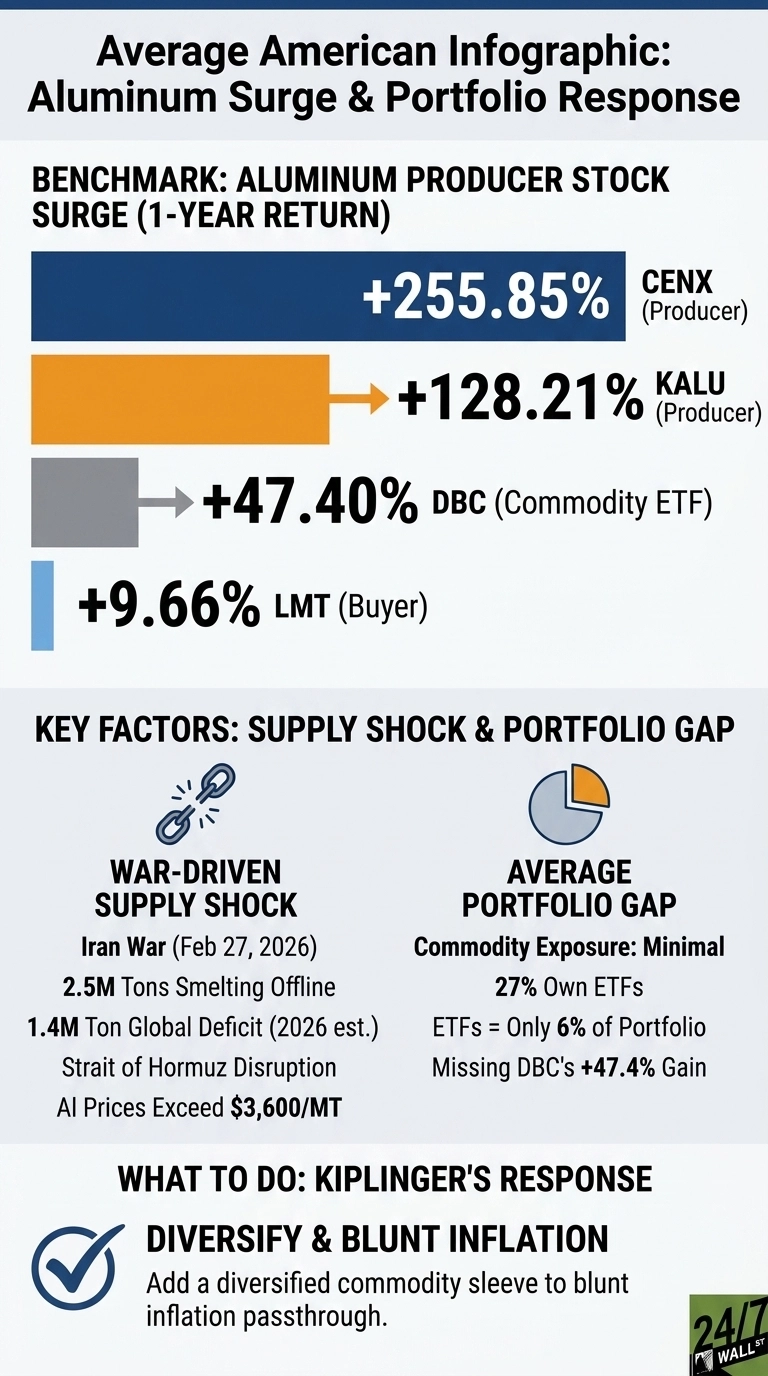

Aluminum is the cleanest read on the disruption, with Oplinger saying more than 2.5 million tons of annual smelting capacity and nearly 2 million tons of refining capacity have gone offline since the conflict began, much of it tied to the Strait of Hormuz, through which roughly 8.8 million tons of alumina and 6 million tons of bauxite transit each year. Century Aluminum CEO Jesse Gary put it in portfolio terms: “The Middle Eastern disruption has expanded our expected 2026 global deficit to 1.4 million tons.” Deficits of that scale do not unwind in a quarter.

The passthrough is already in the broad commodity benchmarks. The Invesco DB Commodity Index Tracking Fund (NYSEARCA:DBC) is up 39.30% year to date and 47.40% over the past year, with shares at $31.19. That is the move a household with no commodity allocation has missed.

Where the gains have actually landed

Alcoa (NYSE:AA | AA Price Prediction) reported Q1 2026 adjusted EBITDA of $595 million and adjusted EPS of $1.40, with the aluminum segment adding $174 million sequentially on higher metal prices. The stock has returned 111.83% over the past year.

Century Aluminum (NASDAQ:CENX) guided Q2 adjusted EBITDA to $315 million to $335 million, up from $231 million in Q1. The stock is up 255.85% over the past 12 months. Kaiser Aluminum (NASDAQ:KALU) reported $3.74 in Q1 2026 EPS against a $1.96 estimate, a 90.49% beat. Analysts had been resetting estimates upward all year and still missed.

The downstream side is more mixed. Lockheed Martin (NYSE:LMT) is up only 9.66% over the past year, with a trailing P/E of 25. Higher input costs and fixed-price defense contracts mean the aluminum surge hurts the buyer side of the chain even as it lifts producers.

How the average American is actually positioned

The Charles Schwab Modern Wealth Survey found that 27% of American investors own ETFs, but those funds account for only 6% of the average investor’s portfolio. Within that 6%, dedicated commodity exposure is minimal. The Federal Reserve’s Survey of Consumer Finances shows that household financial assets are roughly 53% equities on average, with the balance in cash, bonds, and retirement accounts, which are themselves overwhelmingly equity-tilted.

That allocation worked during the disinflation of the 2010s. It does not work during a wartime supply shock. When a single-commodity ETF like DBC outpaces the S&P 500 by a wide margin over five months, a portfolio with zero commodity exposure takes the inflation hit on the cost side, with no offset on the asset side.

What Kiplinger’s framework actually says

Kiplinger’s May 12 ETF guide recommends a diversified inflation hedge rather than a single-metal bet, noting that a broad commodity fund like DBC currently holds roughly 29.9% in energy, 29.3% in metals, and 27.8% in agriculture as of April 2026. The same geopolitical event lifting aluminum is also lifting WTI crude, which traded between $98 and $114 per barrel through April and early May after starting the year near $57 per barrel. A diversified vehicle captures the correlated move without single-commodity risk.

For a household evaluating its own allocation, the practical questions are narrow. First, is there any commodity exposure in the 401(k) or brokerage account, or is it 100% equities and bonds? Second, if exposure is added, is it through a broad-basket fund such as DBC, or through individual producers where earnings leverage is higher but volatility is much greater? Century Aluminum’s 1.916 beta functions as an amplifier of commodity moves rather than a stable inflation hedge.

For now, the timing of when the Strait reopens or when the deficit closes remains unknown. What the data shows is that the average American portfolio entered this shock with almost no commodity allocation and has missed the offset that a small one would have provided. That gap is the story, and it’s something that investors, even those of the retail variety, should move on before it’s too late.

Contact [email protected] for any questions or corrections.