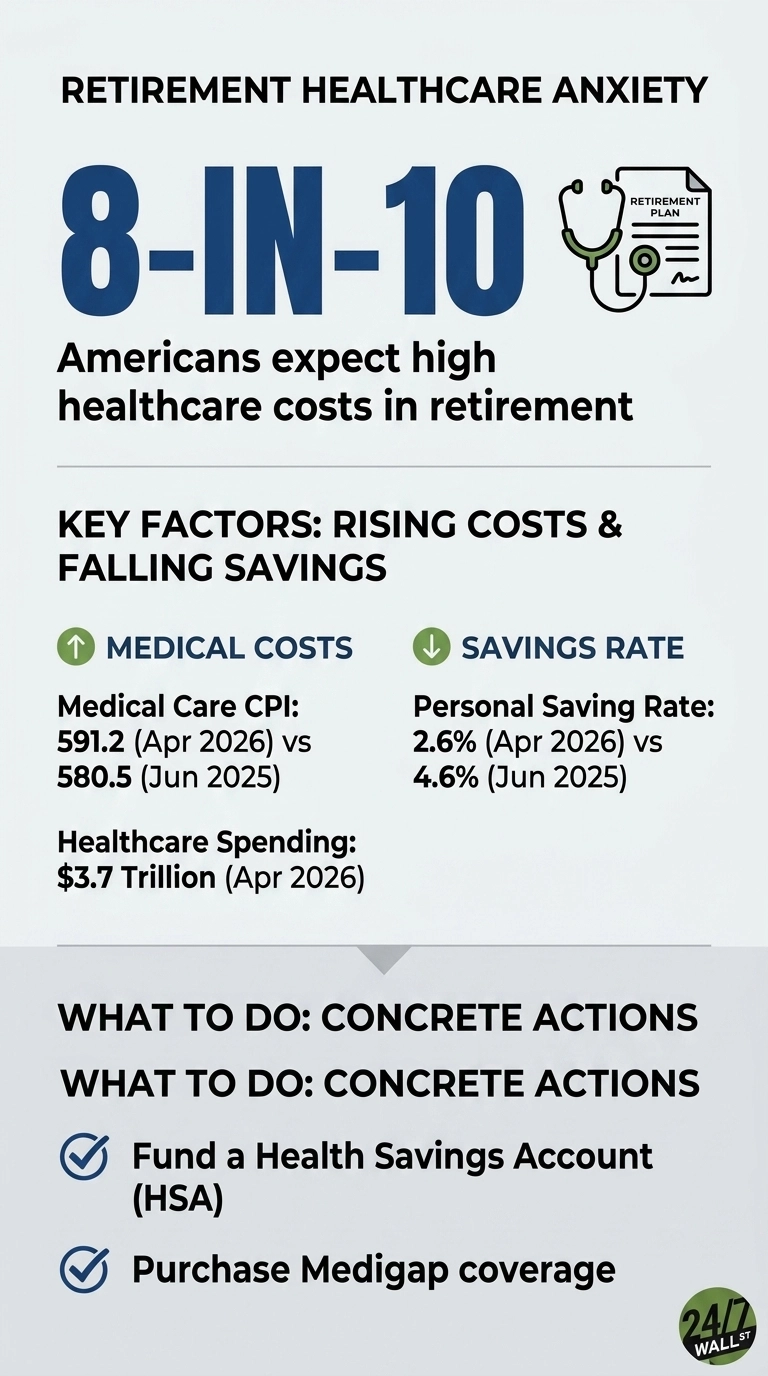

Healthcare in retirement has become the single highest cost Americans cannot reliably predict, and the anxiety around it is now mainstream. Fidelity’s 2026 retirement study finds that 8 in 10 Americans expect high healthcare costs in retirement. The Medical Care Consumer Price Index has climbed from 580.527 in June 2025 to 591.202 in April 2026, while overall consumer healthcare spending reached $3,700.1 billion in April 2026, up from $3,432.2 billion in January 2025.

Healthcare now accounts for roughly 24.5% of all service spending, second only to housing. The more useful the data, the more useful the response, and Fidelity’s data points to four specific moves Americans are making to prepare. Each one targets a different piece of the healthcare cost equation, and together they outline a fairly coherent strategy for households trying to get ahead of the problem.

Move 1: Funding a Health Savings Account

The first response is the most direct, as 25% of Americans are funding Health Savings Accounts specifically because of retirement healthcare concerns. HSAs occupy a unique tax position: contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, the account also functions like a traditional IRA for non-medical withdrawals, taxed as ordinary income with no penalty.

For a cost category that compounds faster than general inflation, the triple tax advantage matters. Core PCE, the Federal Reserve’s preferred inflation gauge, sits at 129.63 as of April 2026, up from 126.121 a year earlier, and medical care has historically run hotter than the headline number.

Move 2: Buying Medigap Coverage

Accordingly, 27% are purchasing Medigap coverage, the supplemental insurance that fills gaps in Original Medicare. Medicare Parts A and B leave retirees exposed to deductibles, coinsurance, and copayments that can add up quickly during a hospitalization or a chronic illness. Medigap shifts that exposure to a predictable monthly premium. With Medicare transfer payments reaching $1,301.0 billion in the first quarter of 2026, up from $1.1 trillion a year earlier, the system itself is under strain. That growth reflects more enrollees and higher per-person costs, both of which translate into larger out-of-pocket exposure for the share Medicare does not cover.

Move 3: Long-Term Care Insurance

Finally, 22% are obtaining long-term care insurance, addressing the cost category most likely to drain a retirement plan. Neither Medicare nor Medigap covers extended custodial care, which includes assisted living and most nursing home stays. A multi-year long-term care episode can run into six figures annually, and self-funding that risk requires a substantial asset base. Long-term care insurance, including the newer hybrid life-and-LTC policies, transfers a defined portion of that risk in exchange for premiums paid during working years.

Move 4: Higher Retirement Contributions

The fourth move is broader, as 40% are contributing more to retirement accounts overall in response to healthcare concerns. This is the lever most workers can pull immediately, and it carries through every retirement spending category, not just medical. The constraint is capacity, as the personal saving rate has fallen from 4.6% in June 2025 to 2.6% in April 2026. Households want to save more for healthcare, but the room to do so has narrowed.

Consumer confidence reflects that squeeze, as the University of Michigan consumer sentiment dropped to 49.8 in April 2026, deep in recessionary territory and well below historical baselines.

The Planning Layer

Fidelity also reports that 74% of Americans say they have a plan in place to reach their retirement goals. Healthcare anxiety, in other words, is functioning as a planning catalyst. The four moves above are not mutually exclusive, and the households making the most progress are usually combining them. An HSA addresses pre-Medicare costs and tax-advantaged accumulation. Medigap handles routine gaps after 65. Long-term care insurance covers the tail risk. Higher contributions fund the rest.

The economic backdrop is not making any of this easier, and per capita disposable income reached $68,359 in the first quarter of 2026, up from $66,095 a year earlier, but most of that gain has been absorbed by consumption rather than saving. For households starting now, the practical path is to pick one of the four moves, automate it, and add the next when capacity allows.

Contact [email protected] for any questions or corrections.