Alibaba Group Holding Ltd. (NYSE: BABA) is set to report earnings on Thursday. Trying to second guess earnings ahead of time from a relatively new company, particularly a large Chinese company, is no smart effort. Still, investors are acting scared ahead of Alibaba’s report.

Alibaba Group Holding Ltd. (NYSE: BABA) is set to report earnings on Thursday. Trying to second guess earnings ahead of time from a relatively new company, particularly a large Chinese company, is no smart effort. Still, investors are acting scared ahead of Alibaba’s report.

Alibaba reports its fiscal fourth-quarter results on Thursday, and the consensus estimates were $0.43 in earnings per share (EPS) and $2.78 billion in revenue just at the end of last week. Those consensus estimates have now stayed static on revenue but the EPS forecast is down one cent to $0.42 per share.

One thing to consider is that the EPS estimate for this coming quarter was as high as $0.46 just 60 days ago. The consensus estimate of $2.79 in EPS for fiscal March 2016 is down from $2.86 just 60 days ago. That is not a massive drop for an earnings expectation consensus, but this is on the world’s largest initial public offering (IPO).

One recent concern may be that the Chinese online retail giant is in the midst of a hiring freeze. CEO Jack Ma even reportedly said that the company has grown much too quickly.

There are also concerns from some that Alibaba has been trying to play more fairly by clamping down on knock-off and counterfeit goods sold through its networks. That is a welcome sign for buyers and for companies with brands that want to be protected, but the reality is that policing sellers costs money — and it may even thwart some of the lower-end sales, hurting Alibaba revenues.

Short sellers remain active in Alibaba as well. Some of these players may simply be hedgers who are anticipating a larger share float ahead, or holders who wanted to get ahead of the next lock-up or event-risk. Still, the 56.5 million shares in the latest short interest may not be a peak, but it is close to four days to cover.

One last consideration about the fundamentals of Alibaba is that most U.S. investors just do not really have a firm handle on what Alibaba really is. It seems that it is an insult when you refer to Alibaba as the “Amazon of China.” After the previous earnings report and guidance, 24/7 Wall St. could not help but to ask whether it was fair to think that Alibaba duped Wall Street analysts and investors into thinking its growth rates were higher.

ALSO READ: 13 Analyst Stock Picks Under $10 With Massive Upside Targets

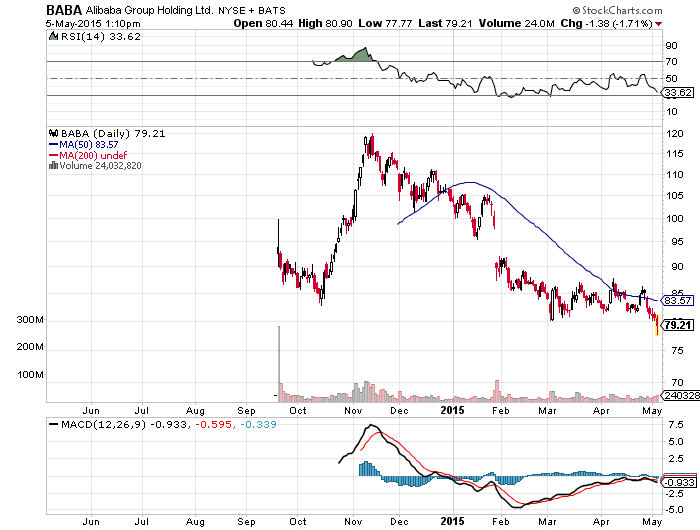

Unfortunately, all the things acting against Alibaba are coming when the stock is at a post-IPO low. Tuesday brought a new low of $77.77. Again, its shares have not even been public for a year. Alibaba’s chart below (from StockCharts.com) shows only a 50-day moving average because it hasn’t traded long enough to actually have a 200-day average yet. Still, what the chart does represent is that the hardline support was supposed to be $80 as of March. Now the shares have broken under $80, and some investors may worry that Alibaba’s $68 IPO price could become a true risk.

Again, it is probably not child’s play to try to guess what a Chinese company’s earnings are really going to be. That being said, what is the sentiment that you get when every single shareholder who ever decided to step up and buy Alibaba stock prior to this day is now sitting on a paper loss?

Alibaba shares ended trading at $81.17 on Friday, and the post-IPO range was $80.03 to $120.00.

The consensus price target is $106.61 currently, down slightly from the consensus $106.90 late last week. Now go back to the most recent earnings report, and the consensus price target was just over $120 before it announced results.

The good news is that Alibaba shares were back at $79 at the time this report was finished. The bad news is that, well, the bad news has been stated many times above.

The number of active buyers on Alibaba’s retail marketplaces totaled 334 million in the 12 months ended in December, up 45% year-over-year. It said that it added 48 million active users at that time, with over $1 billion in mobile revenues.

Alibaba further said with its last report that its mobile active users rose from 217 million at the end of September to 265 million at year-end. The company said that is nearly double the number of mobile buyers at the end of 2013.

The company’s CEO, Jonathan Lu, said with earnings one quarter ago:

Our unrivaled leadership and momentum in mobile continued — we added 48 million active users sequentially and delivered over US$1 billion in mobile revenue during the quarter. Our business continues to perform well, and our results reflect the strength of our ecosystem and the strong foundation we have for sustainable growth.

Also in the last quarter, Alibaba measured its performance on gross merchandise value (GMV), which is the total amount transacted on its marketplace websites. Alibaba said that the total GMV was $127 billion and mobile GMV accounted for $53 billion — or 42% — of that total. Sequentially that is a gain of 36% in mobile GMV. Prior to that report, analysts on Wall Street had looked for stronger growth in mobile transactions.

ALSO READ: 5 Oil and Gas Stocks Analysts Want You to Buy

And for the good things to consider: It often gets lost just what a large global footprint that is owned by Alibaba. The company claims more active users than the entire U.S. population. Still, this massive number represents barely a quarter of China’s population. There is still a lot of unharnessed growth for Alibaba to capture if it can figure out how to get China’s vast number of mobile users to shop from their phones — and if it can get anywhere close to earning on mobile users what it does on desktop users.

Contact [email protected] for any questions or corrections.