By Doug Clinton of Loup Ventures

In venture, our job is to swing for grand slams because venture returns follow a power law function where your biggest winner is going to provide the majority of your return. Base hits do not add up to a grand slam, even if they let you score a run.

Enough baseball.

[in-text-ad]

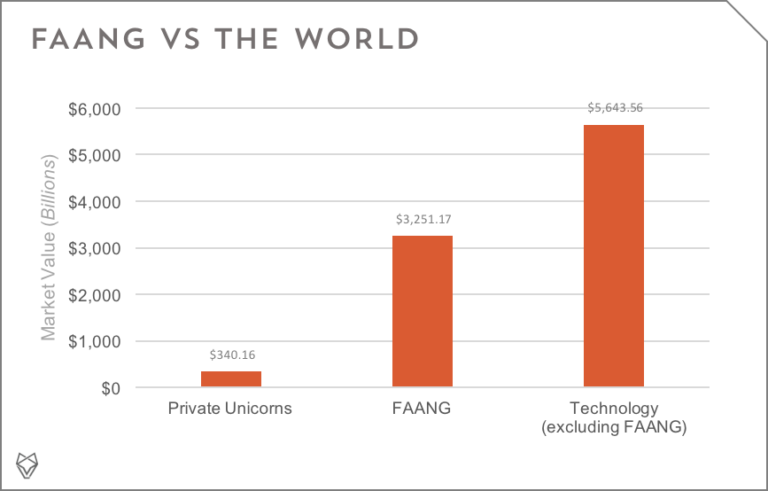

In a way, the same observation applies to the public markets. We all know the power of the FAANG stocks (Facebook, Apple, Amazon, Netflix, and Google), but it’s even more apparent when we put it into context with numbers. As of June 6th, those five stocks totaled over $3.25 trillion in market cap. By comparison, the 610 other stocks in the Technology sector total $5.6 trillion in value (excluding any FAANG stock in the Technology sector).

[nativounit]

And FAANG dwarfs the unicorn market too — the 65 known US-based unicorns as of the end of May total just about $340 billion in value, a tenth of FAANG. Certainly, some of these unicorns will continue to grow, but is there one we can justifiably argue will be big enough to insert itself into the FAANG conversation? Maybe Uber or Airbnb. Maybe Magic Leap if it delivers on its vision. Maybe some company that figures out artificial general intelligence.

Whatever the next FAANG-type company might be, it has to do something grand. Facebook and Google have transformed information consumption, Apple gives us products to interact with that information, and Amazon lets us have anything we want delivered to our door. They’ve meaningfully changed the world. Perhaps grand slam is too common to describe this occurrence. The FAANG companies are really quadruple doubles. Who plays baseball any more anyway?

Disclaimer: We actively write about the themes in which we invest: virtual reality, augmented reality, artificial intelligence, and robotics. From time to time, we will write about companies that are in our portfolio. Content on this site including opinions on specific themes in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making investment decisions. We hold no obligation to update any of our projections. We express no warranties about any estimates or opinions we make.

[recirclink id=469057]

[wallst_email_signup]

Contact [email protected] for any questions or corrections.