We would point out that the data period for this report was a bit aged compared to the August 2014 release date. The data collection began September 17, 2013 and ended on October 4, 2013, and was based upon the complete responses of just over 4,100 respondents.

It turns out that education related debt of some kind was held by some 24% of the population. This included 16% who had debt for their own education, some 7% holding debt for their spouse’s or partner’s education, and 6% who held debt for their children’s education.

Here is where the rub is. The average amount of debt tied to respondents’ own education was $25,750. The average debt for their spouse or partner was $24,593. Average debt size for a child was lower at $14,923. The Fed’s report said, “Of those who reported having debt for their own or a family member’s education, the average total of all education debt was $27,840, with a median of $15,000.”

ALSO READ: America’s Best Companies To Work For

Having debt is also different from problems tied to servicing that debt. The Fed’s report showed that 18% of those with debt were behind on payments in some way for their student debt. That includes 9% who had their student loans in collections.

This may seem somewhat self-serving, but it does suggest an underlying drag that could be present for years and years into the future. Of those who failed to complete the program they borrowed money for, they were far more likely to say that the costs of the education outweighed any financial benefits they received from the education.

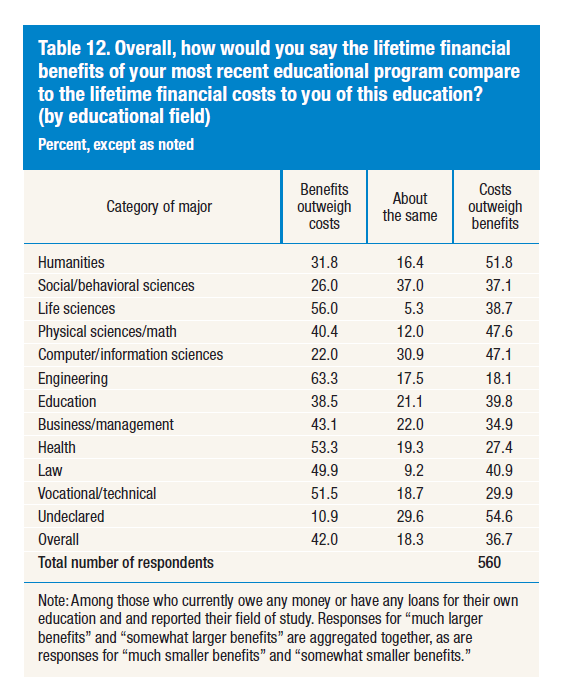

Now, we looked closer at respondent claims about whether the costs outweigh the benefits of taking on that debt. This was under a financial well-being test in educational fields of study. Some of the figures seem very odd, but some seem to be in line with what someone might expect by major (see below). The caveat here – it was based solely upon 560 total respondents, something that should be generally too few for statistical precision outside of directional implications.

What is becoming obvious is that the debate over student debt will only continue for years into the future. It seems hard to imagine that those with secondary education would ultimately say that they feel the net benefits over the course of a life would turn on their education and say that the extra pay was not worth the cost of the education. Still, that just may be yet another disappointment in the new reality.

Another coming crisis was also covered from this same broad report – Many Americans aged 45 and older have no earthly idea about how they will pay for their retirement expenses.

ALSO READ: The Highest Paying Companies To Work For

The New York Federal Reserve issues separate readings on consumer debt. In February of 2014, the New York Fed reported that the outstanding student loan balances reported on credit reports as of the end of 2013 had risen to $1.08 trillion.

Contact [email protected] for any questions or corrections.