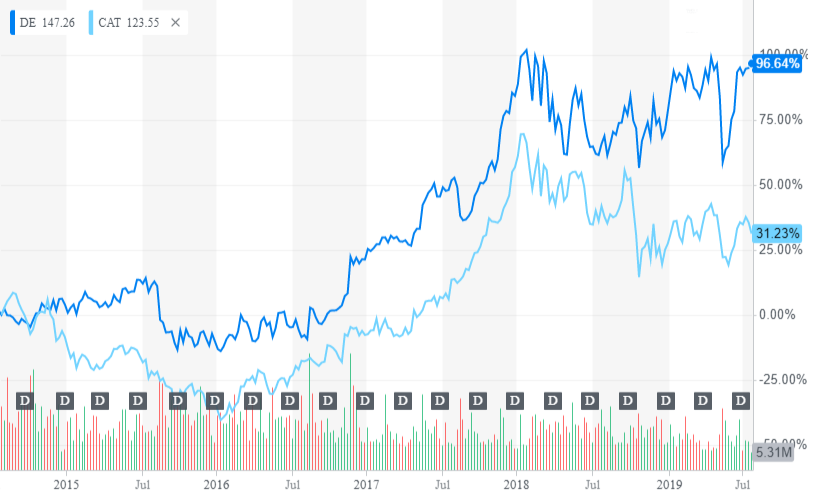

Over the past five years, shares of machinery manufacturer Deere & Co. (NYSE: DE | DE Price Prediction) have just about doubled. That includes a dismal 34-point dip after the firm reported first-quarter results in May.

Fellow heavy equipment maker Caterpillar Inc. (NYSE: CAT) reported disappointing second-quarter results Wednesday, cutting off a reversal of a recent low posted in late May. Over the past five years, Caterpillar’s stock has added nearly a third to its share price, but at the start of 2018, the gain was nearly twice that size.

Caterpillar reined in its guidance for 2019 earnings, citing rising costs, slowing demand and lower confidence in a recovery in the second half of this year. Sales are expected to improve slightly, assuming that the oil and gas industry business picks up and that the company’s dealers can reduce their existing inventories and swallow a price hike to help Caterpillar offset its rising costs.

[nativounit]

Here’s how Caterpillar and Deere stock prices matched up over the past five years.

When Deere reports on August 16, analysts are looking for earnings per share (EPS) of $2.86 and revenues of $9.4 billion. In the same quarter of 2018, Deere posted EPS of $2.59 and revenues of $9.29 billion. How likely is Deere to overcome the same drags on performance that hurt Caterpillar’s second quarter?

When it reported first-quarter earnings, Deere scaled back its projections for the current fiscal year, clearly nervous about the second half of the year in North America. U.S. farmers continue to suffer from the trade war with China and even if the federal government pays some compensation for the lost sales, farmers are unlikely to be spending the money on new tractors. Deere also characterized the economy for the rest of the year as “positive” for its forestry and construction businesses.

Since then, most projections for end-of-the-year economic growth have been scaled back. The International Monetary Fund recently revised its projections for global growth in 2019 from a prior estimate of 3.3% to 3.2% for 2020, down from 3.6% to 3.5%. The IMF called the global economy “sluggish and precarious” and said its lowered estimate “reflects negative surprises” for emerging and developing market growth offsetting some “positive surprises” in growth in the advanced economies.

If Caterpillar is pinning its hopes on an uptick in the oil and gas industry and on its ability to raise prices, those are mighty tenuous hooks on which the company is hanging is hopes. Likewise, Deere’s outlook on the economy is almost certain to be revised downward and with that revision, the company will be almost forced to revise its sales and profit expectations.

Of the four analysts who have weighed in on Caterpillar since it announced second-quarter earnings, three maintained their Buy ratings and one lowered its rating from Buy to Hold, and three of four lowered their price targets.

The four analyst moves on Deere so far in July have included two reaffirmed Buy ratings (with raised price targets), one upgrade from Neutral to Buy and one downgrade from Buy to Neutral. Following the company’s earnings report in May, every call but two that we’ve seen has reiterated a Buy or raised a Neutral rating to Buy. Of the other two, one reaffirmed a Hold and the other dropped a Buy rating to a Hold.

Deere’s stock traded down about 0.4% in the noon hour Thursday, after posting a small gain on Wednesday, while Caterpillar shares traded up about 1.7%, regaining almost half of Wednesday’s loss. Deere could continue to pay the price for Caterpillar’s sins until it reports next month. If that report either misses or does not beat expectations by a wide enough margin, Deere’s stock could take a nasty drop.

[recirclink id=563191]

[wallst_email_signup]

Contact [email protected] for any questions or corrections.