Caterpillar (NYSE: CAT | CAT Price Prediction) and Deere & Company (NYSE: DE) both reported results showing the same headwinds hitting in very different ways. Caterpillar beat estimates with modest earnings pressure. Deere missed badly, with full-year net income down 29% as the agricultural downcycle crushed core segments.

One Diversifies Through the Storm. One Takes It on the Chin.

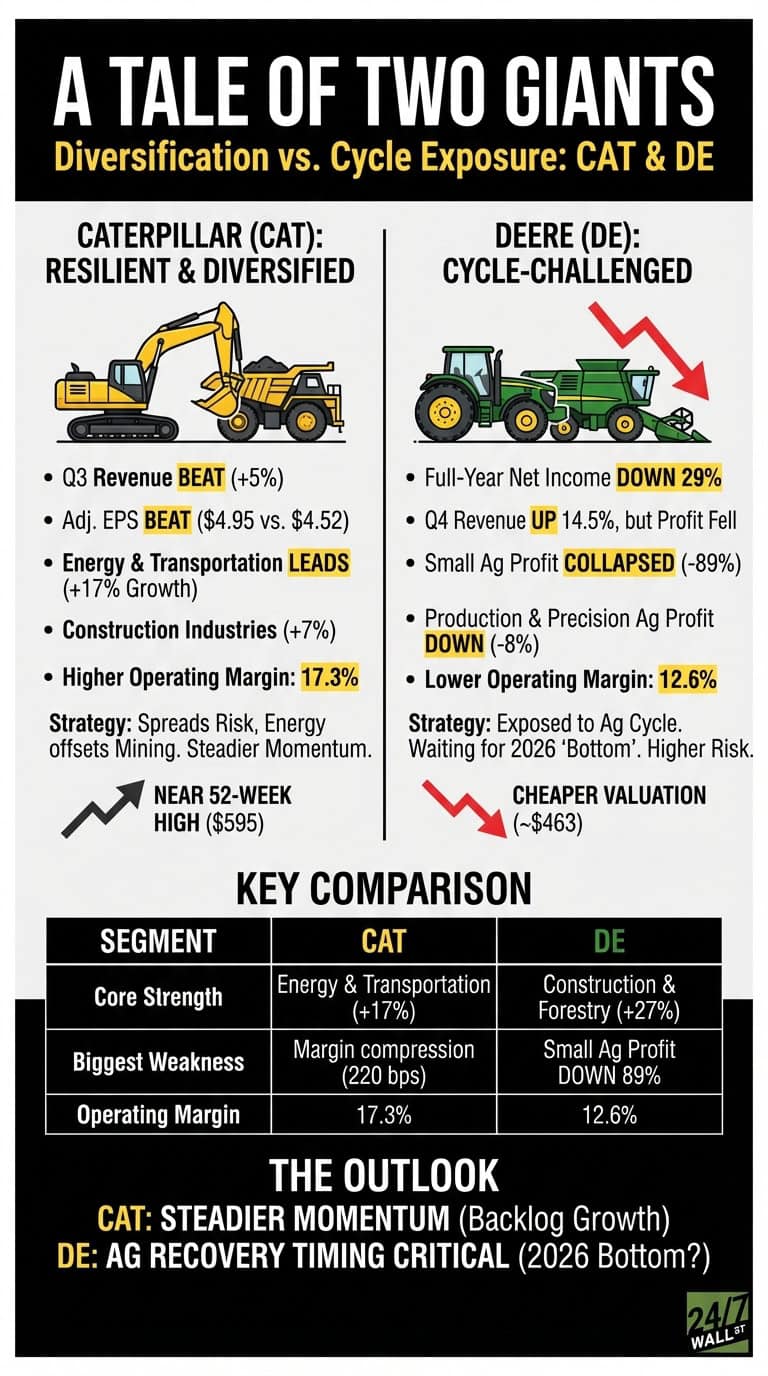

Caterpillar posted Q3 revenue of $17.64 billion, beating the $16.77 billion estimate by 5%. Adjusted earnings per share came in at $4.95, above the $4.52 consensus, though down 4.3% from $5.17 a year earlier. Operating margin fell from 19.5% to 17.3% as manufacturing costs and tariffs bit into profitability. CEO Joe Creed pointed to “resilient demand and focused execution,” with Energy & Transportation leading at 17% sales growth to $8.40 billion. Construction Industries grew 7%, and Resource Industries added 2%. Operating cash flow of $3.7 billion funded $1.1 billion in dividends and buybacks.

Deere reported Q4 revenue of $12.39 billion, up 14.5% year over year, but full-year net income dropped 29% to $5.03 billion. Production & Precision Agriculture saw a 10% sales increase to $4.74 billion but operating profit fell 8% due to higher production costs and tariffs. Small Agriculture & Turf operating profit collapsed 89%. Construction & Forestry was the bright spot, with sales up 27% to $3.38 billion and operating profit up 6%. CEO John May acknowledged “challenges and uncertainty” but emphasized “structural improvements” and called 2026 “the bottom of the large ag cycle.”

| Segment | CAT | DE |

| Core Strength | Energy & Transportation (+17%) | Construction & Forestry (+27%) |

| Biggest Weakness | Margin compression (220 bps) | Small Ag profit down 89% |

| Operating Margin | 17.3% | 12.6% |

Diversification Shields One. Cycle Exposure Punishes the Other.

Caterpillar’s three-segment model spreads risk. Energy & Transportation growth offset softer mining demand, and construction stayed steady. The 17.3% operating margin, while down, still reflects pricing power and operational discipline.

Deere is more exposed to agricultural cycles, and farmers are pulling back hard. The 89% operating profit drop in Small Ag & Turf shows how quickly margins evaporate when demand softens and costs rise. Construction & Forestry provided relief, but not enough to offset the ag decline. Operating cash flow of $7.46 billion, up 46%, shows strong working capital management, but the earnings trajectory is steep and negative.

Both companies cited tariffs and production costs as margin headwinds, but Deere absorbed more damage. Caterpillar’s diversification and higher margins gave it more cushion.

The Next Inflection Point Is Ag Recovery Timing

Deere’s guidance for fiscal 2026 net income of $4.00 billion to $4.75 billion suggests management expects stabilization, not recovery. May’s call that 2026 will mark “the bottom of the large ag cycle” is the key variable. If correct, Deere sets up for a rebound in 2027. If wrong, margins stay under pressure.

Caterpillar’s backlog growth and energy segment strength suggest steadier near-term momentum.

Different Risk Profiles Emerge

Caterpillar’s 46.3% return on equity and 17.3% operating margin reflect a more profitable, diversified business model with less exposure to cyclical agricultural markets. The stock trades near 52-week highs at $595.

Deere’s valuation is cheaper across metrics, with analysts projecting 14% potential gains from current levels around $463. The company’s performance depends heavily on the timing of agricultural cycle recovery, which management expects to bottom in 2026.

Contact [email protected] for any questions or corrections.