The Merrill Lynch RIC Report always has some interesting figures and observations along with its monthly outlook. For investors, it also comes with many near-term and long-term assumptions for its readers. When you hear the panic about rising interest rates coming sooner rather than later it may cause panic about all fixed income classes. It turns out that not all bond classes are equal – and high-yield and leveraged closed-end municipal bond funds look like they are still going to be highly appropriate for more long-term aggressive bond investors and for those investors who are in the highest tax brackets.

The Merrill Lynch RIC Report always has some interesting figures and observations along with its monthly outlook. For investors, it also comes with many near-term and long-term assumptions for its readers. When you hear the panic about rising interest rates coming sooner rather than later it may cause panic about all fixed income classes. It turns out that not all bond classes are equal – and high-yield and leveraged closed-end municipal bond funds look like they are still going to be highly appropriate for more long-term aggressive bond investors and for those investors who are in the highest tax brackets.

Merrill Lynch is certainly not recommending that investors be all in bonds. Depending upon an investors risk profile, the firm has a total asset allocation for its traditional bucket clients as ranging from 11% to 55% in bonds, and 20% to 84% in stocks. The message to consider here is that municipal bonds, and in this case the closed-end funds (CEFs), are being given a very strong allocation depending upon tax brackets.

What investors have to consider about muni-bonds is that they are immune from federal taxes, which is implied to include an additional 3.8% surcharge (that means tax for those paying it) that gets taken away for the Affordable Care Act. While Merrill Lynch does not account for this, some states have state income taxes on municipal bonds if they are issued from other states than the state the investor lives in. In short, some of the stated muni-bond yields may literally be almost double the rate on an after-tax comparison to other traditional bond funds for some investors.

Take this as an example, without considering any state taxes: those in the 43.4% tax bracket getting a 6% tax-free yield have the same after-tax return as a 10.6% from a taxable yield.

24/7 Wall St. has included five of the RIC report closed-end funds which are leveraged municipal bond closed-end funds. Preference was given to those with discounts to Net Asset Value (NAV) and to those which are more actively traded. These closed-end funds include the following funds with Buy ratings at Merrill Lynch:

BlackRock MuniYield Quality Fund (NYSE: MYI) has a 6.3% distribution yield, measured recently with a 5.8% discount to NAV. This BlackRock fund trades about 125,000 shares per day.

BlackRock Municipal Income Trust (NYSE: BFK) was shown to have a 6.3% distribution yield, measured recently with a 4.4% discount to NAV. The BlackRock closed-end fund has an average daily volume of about 85,000 shares.

Nuveen Dividend Advantage Municipal Fund (NYSE: NAD) has a 6.3% distribution yield, measured recently with a 8.8% discount to its NAV. This Nuveen closed-end fund has an average volume of about 74,000 shares.

Pimco Municipal Income Fund II (NYSE: PML) has a 6.4% distribution yield, measured recently with a 0.8% premium to NAV. The Pimco Municipal Income Fund II closed-end fund trades about 125,000 shares per day.

Western Asset Managed Municipal Fund Inc. (NYSE: MMU) comes with a 5.6% distribution yield, measured recently with a 3.6% discount to NAV. The closed-end fund has an average daily volume of about 75,000 shares.

ALSO READ: The 10 Richest Cities & Townships in America

There are many more points made by Merrill Lynch’s May RIC Report stating the case for municipal bonds and muni funds within a fixed income allocation. Again, that is not meant to imply that investors should not be in stocks.

The RIC Report for May 2015 noted that closed-end funds are too often considered tactical investments used in investor portfolios when discounts are wide or when a positive outlook on the underlying sector warrants leveraged exposure. The report said:

We believe the evidence supports the case for a more structural, long term allocation to CEFs as a portion of an investor’s overall allocation to specific sectors that is in between all and nothing… The average annualized return (since 2004) for national leveraged muni CEFs has been roughly 6.5% versus 4.8% for the overall municipal bond market. The higher returns clearly indicate that some degree of exposure is warranted, but the higher volatility also illustrates the risks of overexposure.

Still, the RIC report shows that these are not for every type of investor. The warning said:

We believe investors seeking the least degree of volatility who are willing to give up the potentially higher returns should avoid leveraged muni CEFs altogether. And investors seeking the greatest potential returns without concern for potential volatility might consider 100% of their municipal bond allocation be in leveraged muni CEFs.

Merrill Lynch put the most efficient allocation to leveraged muni closed-end funds at 35% of overall muni allocation — appropriate for moderate risk investors. Aggressive investors were shown to consider a leveraged municipal bond closed-end fund allocation of 50%, but conservative investors should consider an allocation of only 20%.

While Muni-CEF’s have only an equal-weight allocation overall, the RIC report showed that CEF portfolio managers have shortened their durations in anticipation of rising interest rates ahead. This is being done to lower losses, even though Merrill Lynch said that leveraged muni CEF NAV total returns may underperform the total return of the muni market. Still, deep discounts to NAV could cushion the impact on share prices.

For most investors, the firm recommends diversifying muni CEF allocations among a few of the roughly 200 muni CEFs currently in the market. Two of the major components of performance for any closed-end fund are changes to NAVs and changes to the premium or discount to NAV — followed by income from distributions (dividends).

There is one thing that closed-end investors have figured out if they have invested in closed-end funds for years. That lesson is never to go all-in just because of a large discount to the NAV. There may be a real reason for that discount, and it could be an overexposure to worries and areas that are less favorable on and off through time – California, tax bonds, Puerto Rico, Detroit, and on and on. The RIC Report said:

There is a tendency for investors to gravitate toward those funds trading at the deepest discounts. And while deep discounts are certainly an attractive feature of some funds, in our opinion, it is more useful to determine how far above or below a fund may be trading from fair value. We assess fair value as being a function of distribution rates based on NAVs, given the strong tendency for higher yielding funds to trade at higher valuation levels and vice versa. In our opinion, those funds trading the furthest below fair value offer the best value. Very often, these funds are not trading at the deepest discounts.

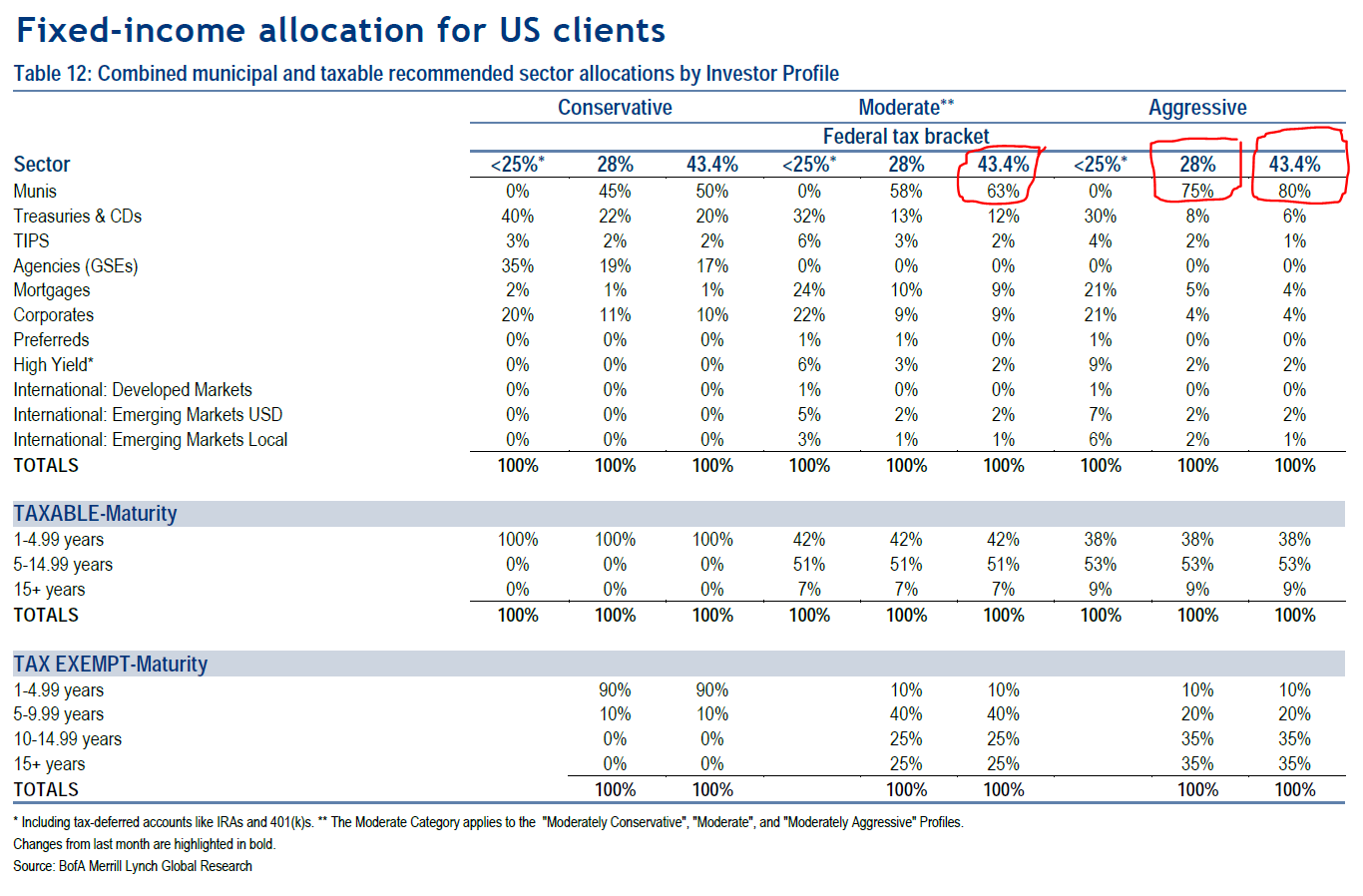

So, what about those allocations? 24/7 Wall St. included one of the RIC Report’s tables showing the proper fixed income allocations for Conservative, Moderate, and Aggressive investors. This was shown to represent allocations based upon tax brackets as well, and those tax brackets peak out at 43.4% based on Federal taxes (including healthcare tax on other asset class income) — but effective tax rates can be higher depending upon income levels and depending upon state income taxation rates if states tax other states were the source of income.

Aggressive fixed income investors were shown to be at 80% municipal for the highest Federal bracket, and even 75% if they were in the 28% tax bracket. That is shown on an expandable table below.

ALSO READ: Wider Losses Seen Coming To Sprint

24/7 Wall St. has a takeaway here for investors in the higher tax brackets. This take is after more than two decades of evaluating bond funds, stock funds, ETFs and other similar asset classes. This view from Merrill Lynch may not be the most breaking news, but it is not common at all for a firm as large as Merrill Lynch to be this heavily weighted in municipals under the right circumstances for this dominant of a muni-fund call within fixed income allocations.

Another view is that there is a hidden message here. To be in the highest tax brackets you have to have high income. That hidden message is that this strategy is what wealthy investors and high-net worth investors are being told to invest in for their proportional fixed income allocations.

Contact [email protected] for any questions or corrections.