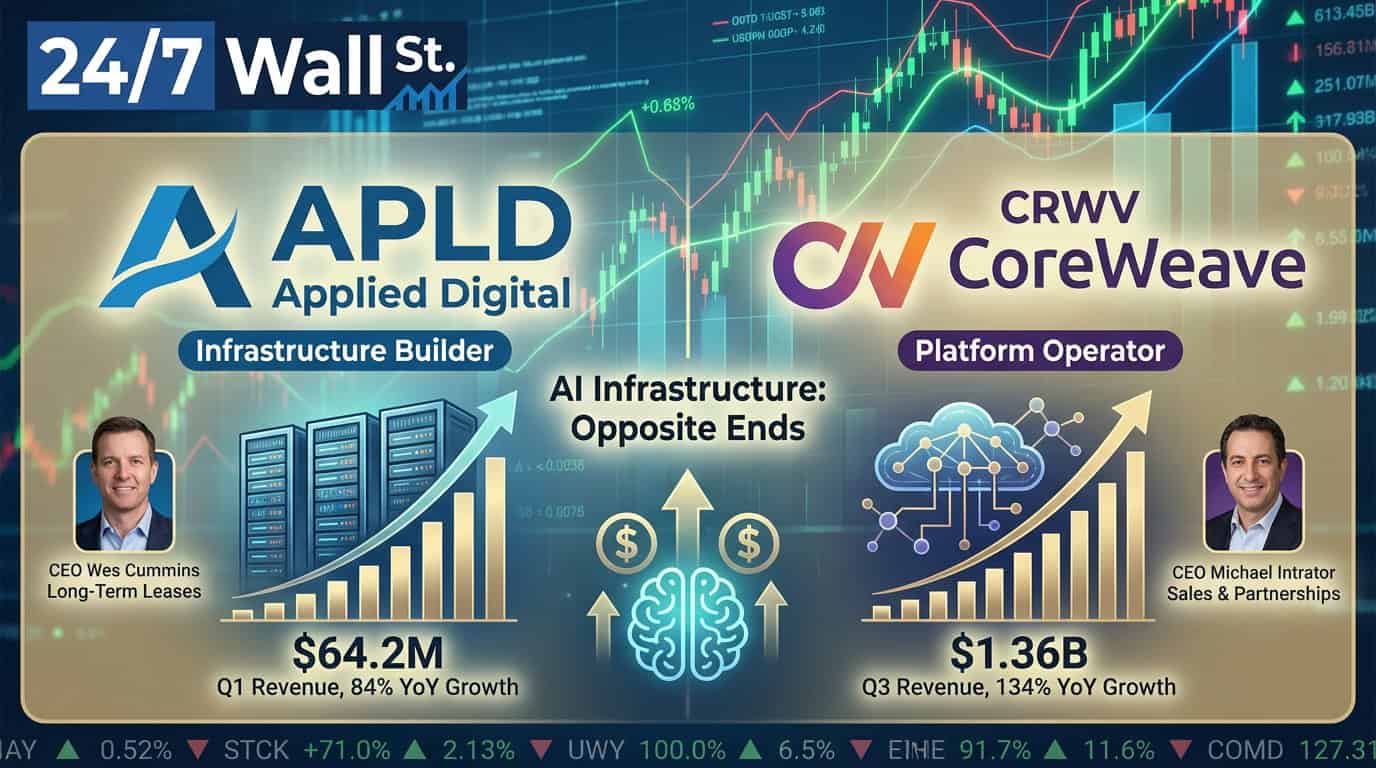

Applied Digital (Nasdaq: APLD) and CoreWeave (Nasdaq: CRWV) reported earnings showing two companies attacking AI infrastructure from opposite ends. Applied Digital builds and leases massive data centers to hyperscalers. CoreWeave operates the cloud platform running AI workloads for developers and enterprises.

Scale Tells Different Stories

CoreWeave reported $1.36 billion in Q3 revenue, beating estimates by 9.6% and growing 134% year over year. The company generated positive operating income of $51.9 million and nearly doubled its revenue backlog to over $55 billion. CEO Michael Intrator stated the company “delivered an exceptional third quarter, setting new records for revenue” while highlighting expanded partnerships with Meta and OpenAI.

Applied Digital posted $64.2 million in Q1 2026 revenue, crushing estimates by 32% with 84% year-over-year growth. Revenue included $26 million from tenant fit-out services in its HPC Hosting Business. The company secured a new 150 MW lease with CoreWeave at Polaris Forge 1, contributing to $11 billion in anticipated lease revenue. Applied Digital lost $27.8 million on an operating basis compared to CoreWeave’s profit.

| Metric | Applied Digital | CoreWeave |

| Q3/Q1 Revenue | $64.2M | $1.36B |

| YoY Growth | 84% | 134% |

| Operating Income | -$18.3M | $51.9M |

| Cash Position | $286.2M | $1.89B |

Infrastructure Builder vs. Platform Operator

Applied Digital focuses on long-term lease commitments with hyperscalers needing physical data center capacity. The CoreWeave lease validates this strategy. Management initiated construction on Polaris Forge 2 with $50 million in secured funding. CEO Wes Cummins emphasized the company is positioning itself “as a trusted strategic partner to the world’s largest technology companies.”

CoreWeave sells compute directly to AI labs, startups, and enterprises through a cloud platform. The $6.3 billion collaboration with NVIDIA deepens its hardware access. The company launched CoreWeave Ventures to support AI innovation across its customer base. This creates recurring revenue streams tied to actual AI workload consumption rather than fixed lease payments.

Applied Digital’s profit margin sits at negative 141% compared to CoreWeave’s negative 39%. Both remain unprofitable, but CoreWeave’s operating leverage appears stronger. Applied Digital trades at 50.31 times trailing sales while CoreWeave trades at 22.21 times sales despite being 21 times larger by revenue.

Who Benefits from the Next Wave

CoreWeave’s $55 billion backlog signals locked-in demand for years. Applied Digital’s lease structure provides similar visibility but depends on tenant fit-out execution and construction timelines. CoreWeave can scale faster by adding compute capacity to existing infrastructure. Applied Digital must build physical facilities first.

CoreWeave competes with AWS, Google Cloud, and Microsoft Azure for AI workloads. Applied Digital competes with Equinix and Digital Realty for hyperscale lease commitments. CoreWeave’s analyst coverage shows mixed sentiment with 52% buy ratings and 7% sell ratings across 27 analysts. Applied Digital enjoys 100% buy-side recommendations from 10 analysts.

Valuation and Risk Considerations

CoreWeave generates positive operating income while growing faster than Applied Digital. The company holds a $1.89 billion cash position for infrastructure expansion. CoreWeave’s direct customer relationships differ from Applied Digital’s lease-based model.

Applied Digital trades at 50x price-to-sales ratio with a 7.1 beta indicating high volatility. CoreWeave trades at 22x price-to-sales despite being 21 times larger by revenue. Applied Digital provides exposure to data center construction, while CoreWeave focuses on cloud operations.

Contact [email protected] for any questions or corrections.