Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) and Intel (NASDAQ:INTC) both reported Q1 2026 results that reframe how investors should think about the AI compute race.

AMD posted a clean acceleration story powered by its Instinct and EPYC franchises. Intel delivered a noisy but improving turnaround quarter under CEO Lip-Bu Tan, with foundry traction and a surprise non-GAAP profit. Two very different businesses. One shared customer: the AI buildout.

Instinct Carries AMD. Foundry and Xeon Steady Intel.

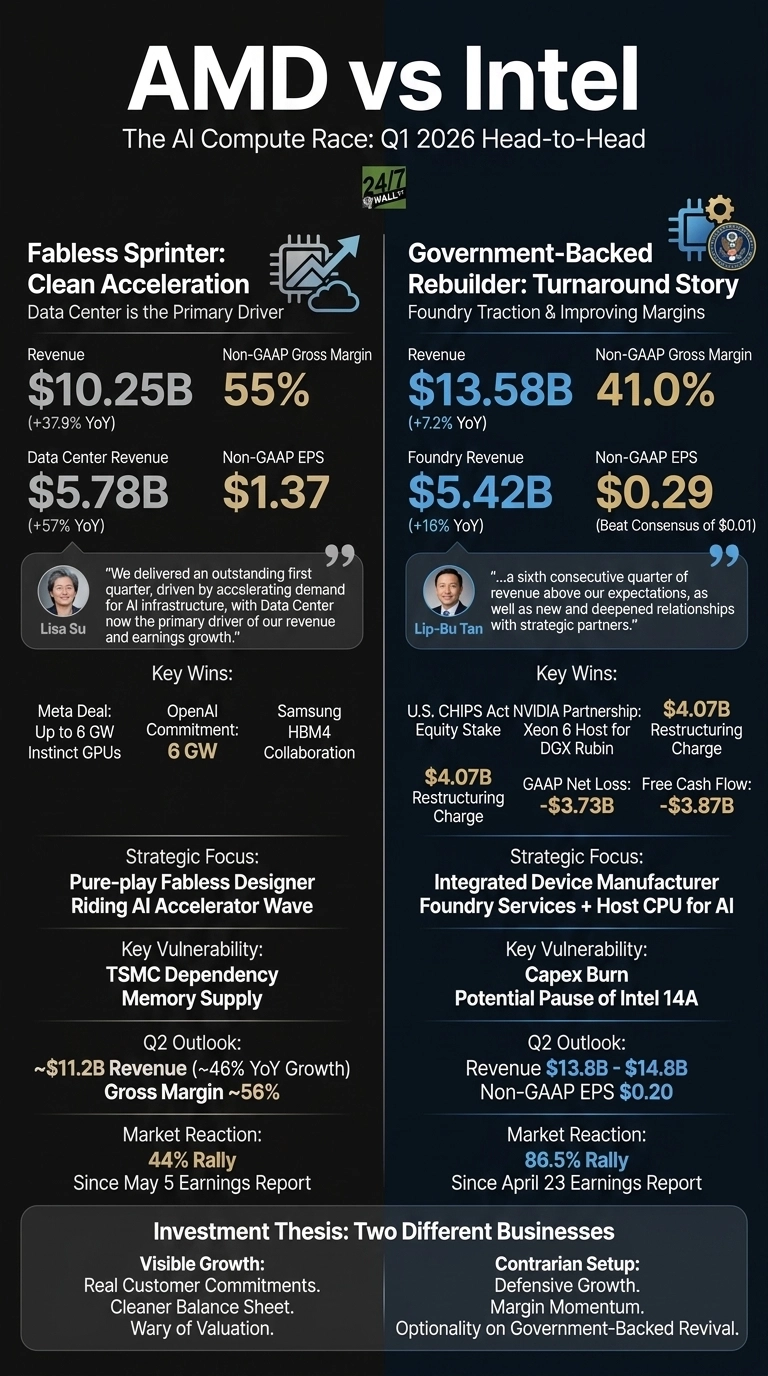

AMD’s quarter was a Data Center quarter. The segment delivered $5.78 billion in revenue, up 57% year over year, lifting total revenue to $10.25 billion and non-GAAP EPS to $1.37.

CEO Lisa Su called out “accelerating demand for AI infrastructure, with Data Center now the primary driver of our revenue and earnings growth”. The new Meta deal for up to 6 gigawatts of Instinct GPUs and matching 6 GW OpenAI commitment are the wins underwriting that confidence.

Intel’s mix tells a different story. Revenue reached $13.58 billion, up 7.2% YoY, with Data Center and AI up 22% and Intel Foundry up 16%. A $4.07 billion restructuring charge tied largely to Mobileye triggered a GAAP net loss of $3.73 billion, yet non-GAAP EPS landed at $0.29 against a near-zero consensus.

| Driver | AMD | Intel |

| Main growth engine | Instinct GPUs, EPYC | Xeon 6, Intel Foundry |

| Q1 revenue growth | +37.9% | +7.2% |

| Non-GAAP gross margin | 55% | 41.0% |

Fabless Sprinter vs. Government-Backed Rebuilder

The strategic split runs deeper than the income statement. AMD sticks to its fabless model, leaning on TSMC and partnering with Samsung on HBM4 supply for MI455X GPUs.

Intel is rebuilding as an integrated manufacturer, with a U.S. government CHIPS Act equity stake, a prior $5B NVIDIA investment, and Xeon 6 selected as host CPU for NVIDIA’s DGX Rubin NVL8. One company is selling accelerators into the AI race. The other is trying to host, package, and fabricate them.

| Lens | AMD | Intel |

| Core bet | MI450 and Helios racks | Intel 18A and foundry services |

| Key vulnerability | TSMC dependency, memory supply | Capex burn, FCF of negative $3.87 billion |

What I Want to See in Q2

AMD guided Q2 revenue to roughly $11.2 billion, implying about 46% YoY growth, with gross margin ticking to 56%. I will watch whether MI450 shipments convert the Meta and OpenAI pipeline into reported revenue.

Intel guided to $13.8 to $14.8 billion with non-GAAP EPS of $0.20. You should watch whether 18A wins enough external foundry customers to justify the spend, because the risk of a potential pause of Intel 14A on weak demand still hangs over the roadmap.

Why I Lean Toward AMD, But Find Intel Harder to Ignore

If I had to pick today, AMD fits my preference for visible growth. The 44% rally since the May 5 earnings report reflects real customer commitments, not just hope. I am wary of the valuation, and the Reddit chatter about AMD funding a customer to buy its chips deserves more scrutiny than bulls give it.

Intel is the more interesting contrarian setup. Shares are up 86.5% since April 23, yet the turnaround is one quarter old. If you want a defensive growth name with margin momentum, AMD reads cleaner. If you want optionality on a government-backed manufacturing revival, Intel earns a serious look.

Contact [email protected] for any questions or corrections.