The semiconductor sector delivered extraordinary performance in 2025, with AI-driven demand reshaping the competitive landscape. After analyzing recent quarterly results, profitability metrics, and strategic positioning across major chip stocks, five companies emerged as the sector’s dominant performers that defined this transformative year.

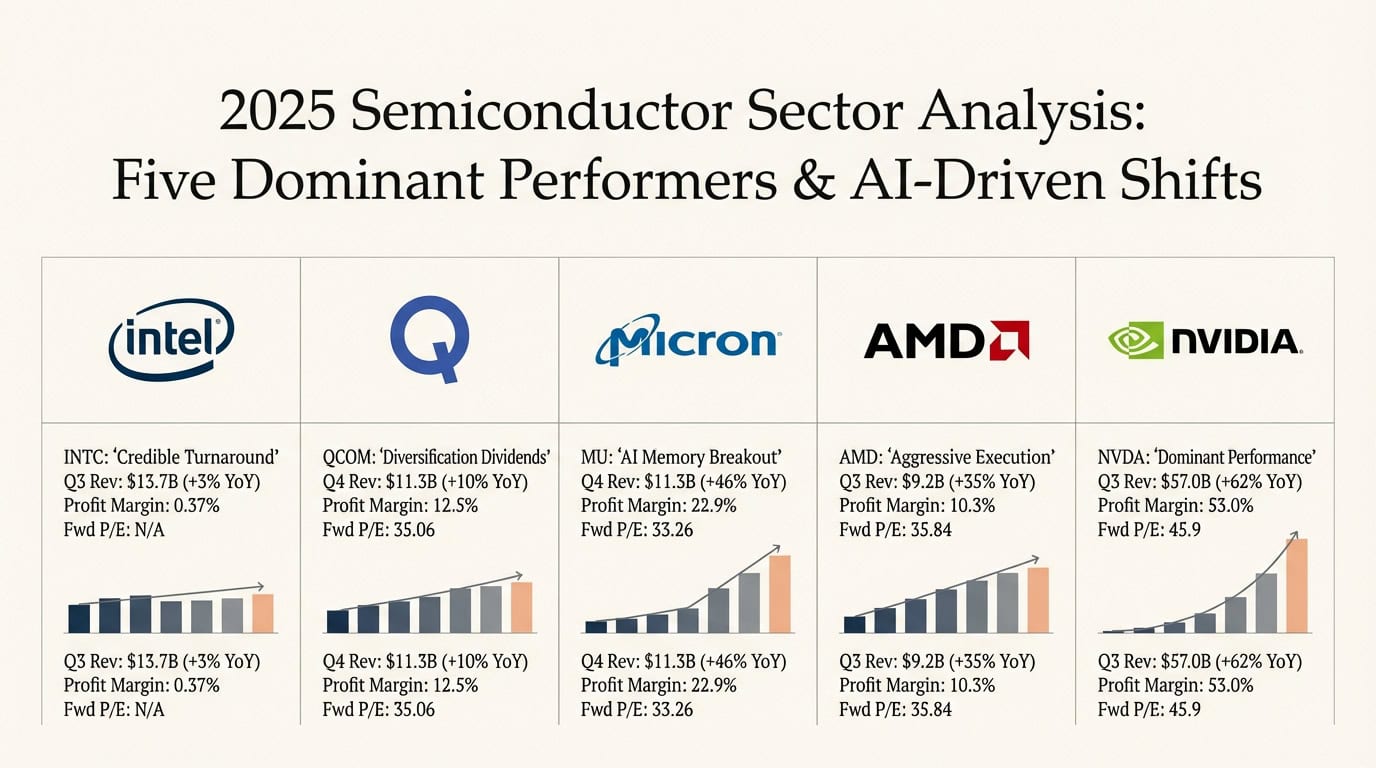

Intel Corporation (INTC)

Intel executed a credible turnaround under challenging conditions. The company reported Q3 2025 revenue of $13.7 billion, up 3% year-over-year, with non-GAAP EPS of $0.23 crushing estimates of $0.01. Client Computing grew 5% to $8.5 billion, while Data Center and AI revenue of $4.1 billion declined 1%.

Intel secured a $2 billion investment from SoftBank and announced a collaboration with NVIDIA, signaling industry validation of its foundry ambitions. However, with gross margins at 38.9% and profit margin of 0.37%, Intel remains in early recovery stages. Q4 guidance of $12.8-13.8 billion revenue suggests continued pressure, but the partnerships demonstrate its technology roadmap is gaining credibility.

Qualcomm Incorporated (QCOM)

Qualcomm’s diversification strategy paid dividends in fiscal 2025. The company posted Q4 revenue of $11.3 billion, up 10% year-over-year, with non-GAAP EPS of $3.00. QCT revenue reached $9.82 billion, up 13%, driven by 18% growth in non-Apple revenues and 17% growth in automotive to $1.05 billion.

The company’s gross margin of 55.3% and profit margin of 12.5% reflect a healthy, diversified business model. With Q1 fiscal 2026 guidance calling for $11.8-12.6 billion in revenue, Qualcomm is successfully reducing smartphone dependence while capturing growth in automotive and IoT markets. The stock trades at a forward P/E of 35.06.

Micron Technology (MU)

Micron delivered a breakout year driven by AI memory demand. Q4 fiscal 2025 revenue hit $11.3 billion, up 46% year-over-year, with non-GAAP EPS of $3.03. Net income surged 261% to $3.20 billion, demonstrating operating leverage as memory prices recovered. Cloud memory revenue reached $4.54 billion, highlighting Micron’s position as a critical AI infrastructure supplier.

The company’s gross margin of 44.7% improved substantially from the prior year’s downturn, with guidance calling for margins exceeding 50% on $12.5 billion in revenue. This represents a complete reversal from the memory market trough. Micron’s profit margin of 22.9% and forward P/E of 33.26 reflect a business hitting its stride as AI data centers demand high-bandwidth memory solutions.

Advanced Micro Devices (AMD)

AMD demonstrated aggressive execution across multiple product lines. Q3 2025 revenue reached $9.2 billion, up 35% year-over-year, with non-GAAP EPS of $1.20 beating estimates of $1.17. Net income jumped 155% to $1.97 billion, though profit margin of 10.3% trails the leaders.

Data Center revenue grew 22% to $4.3 billion, while Client and Gaming surged 73% to $4.0 billion on record Ryzen processor sales. The OpenAI partnership validated AMD’s AI accelerator strategy. With Q4 guidance projecting $9.6 billion in revenue (up 25% year-over-year) and non-GAAP gross margins at 54%, AMD is gaining share in both PC and data center markets.

AMD’s forward P/E of 35.84 versus trailing P/E of 115.43 reveals high market growth expectations. Alpha Vantage data shows quarterly earnings growth of 60.3%, supporting this premium valuation. Notably, 40 of 51 analysts rate AMD as Buy or Strong Buy, with zero sell ratings.

NVIDIA Corporation (NVDA)

Of course, NVIDIA delivered the sector’s most dominant performance in 2025. Q3 fiscal 2026 revenue hit $57.0 billion, up 62% year-over-year, with GAAP EPS of $1.30 beating estimates of $1.27. Net income reached $31.9 billion, up 65%, producing an extraordinary profit margin of 53.0% – five times AMD’s margin and more than double Micron’s.

Data Center revenue of $51.2 billion, up 66% year-over-year, dwarfs the competition. CEO Jensen Huang described Blackwell sales as “off the charts,” with cloud GPUs sold out for the foreseeable future. The company’s gross margin of 73.4% reflects unmatched pricing power in AI accelerators. Q4 guidance of $65 billion (±2%) signals no demand deceleration.

NVIDIA has beaten earnings estimates in eight consecutive quarters, with annual EPS exploding from $0.333 in fiscal 2023 to $3.16 in fiscal 2026 – nearly 10x growth in three years. The stock gained 33.27% year-to-date through December 9, building on a 22,592% return over the past decade. At a market cap of $4.50 trillion and forward P/E of 45.9, NVIDIA commands a premium valuation justified by its dominant position in the AI revolution.

While Reddit discussions in early December reflected debate over valuation and competitive threats from Google’s full-stack AI approach, the fundamentals remain unassailable. NVIDIA’s combination of revenue scale, profitability, and technological leadership positioned it as the sector’s dominant performer in 2025.

Contact [email protected] for any questions or corrections.