A married couple, both 66, sits on $2 million in total retirement assets. They have $1.4 million in a traditional IRA/401(k), $350,000 in a Roth, and $250,000 in a taxable brokerage. They plan to claim roughly $40,000 a year in combined Social Security at age 67. On paper, they are millionaires twice over. In practice, once taxes, healthcare, and inflation take their cut, this portfolio funds a lifestyle closer to a comfortable middle-class household.

Charles Schwab’s 2025 401(k) survey pegged the retirement “magic number” at $1.6 million, with the average expected retirement age at 66. A $2 million balance beats the average, but let’s explore what that means in annual spending.

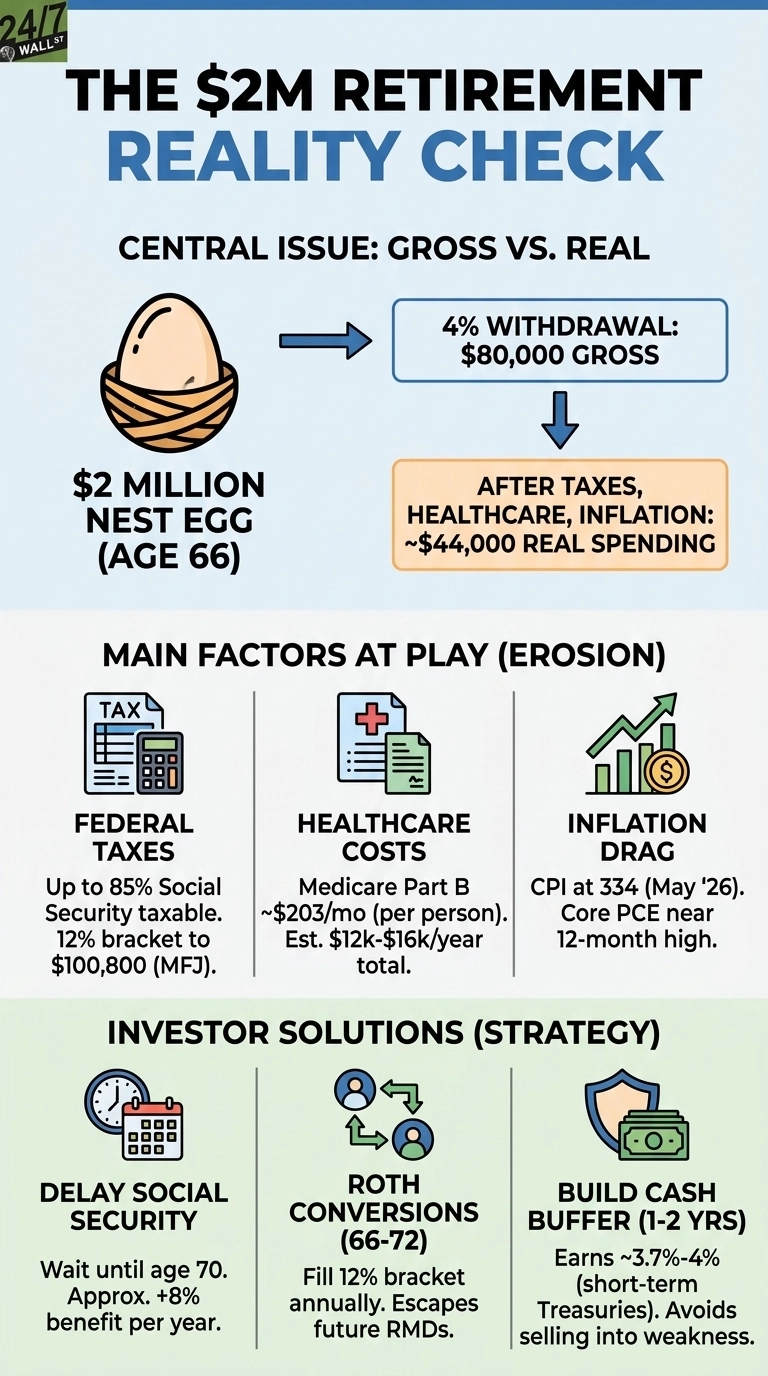

Walking the $80,000 Down to $44,000

The 4% rule says this couple can pull $80,000 from the portfolio in year one. But remember that’s the gross figure. Here are all the things that take a cut:

Federal tax on ordinary income. Most of the withdrawal comes from the traditional IRA, taxed as ordinary income. Up to 85% of Social Security becomes taxable once provisional income clears the threshold. After the 2026 married filing jointly (MFJ) standard deduction of $32,200, the couple lands inside the 12% bracket, which runs to $100,800. Expect federal tax in the low five figures.

Healthcare. The standard 2026 Medicare Part B premium is about $203 per person per month at modified adjusted gross income (MAGI) at or below $218,000. That totals about $4,870 a year for the couple before Part D, a Medigap supplement, dental, vision, and out-of-pocket costs. All-in, plan on $12,000 to $16,000 a year.

Inflation drag. Core PCE, the Fed’s preferred gauge, has climbed to the 91st percentile of its 12-month range. The 2026 Social Security COLA near 3% helps, but does not fully offset a roughly 3% erosion of the fixed pieces of the budget.

Add this all up and the $80,000 gross becomes roughly $44,000 of real discretionary spending. With Social Security, it is livable. But a $2 million balance feels tighter than expected.

The traditional IRA is the taxable engine of this plan. Every dollar out is ordinary income, and required minimum distributions eventually force withdrawals regardless of need. That makes the window between 66 and 72 the most valuable tax planning years. Many advisors call this the “Roth Window.”

Two Moves to Change the Trajectory

- Delay Social Security to 70 and bridge with the IRA. Each year of delay past 67 adds roughly 8% to the benefit, and that larger base is inflation-adjusted for life by the annual COLA. Pulling more from the traditional IRA between 66 and 70 funds living expenses and drains the pre-tax account before RMDs kick in, cutting future forced income.

- Bracket-fill Roth conversions in the 66 to 72 gap. With the 12% bracket running to $100,800 for MFJ, the couple can convert traditional IRA dollars to Roth up to that ceiling at a known, low rate. Every converted dollar escapes future RMDs and future tax-rate risk. Pair this with a 1- to 2-year cash buffer so market drawdowns never force selling equities into weakness. With the 10-year Treasury near 4.6%, that buffer earns a real return while it waits.

State income tax is another lever. Relocating from a high-tax state to one with no income tax (Florida, Texas, Tennessee, Nevada, Washington, Wyoming, South Dakota, Alaska) can add thousands to spendable income annually without changing a single investment.

What to Do First

Model the year-one tax bill in actual software before choosing which account to tap. The conventional order (taxable first, then traditional, then Roth) is a starting point. But for this couple the better move is usually blended: draw enough from the traditional IRA to fill the 12% bracket, top up from the taxable account, and let the Roth compound untouched as the last-resort and estate asset.

Treat the $2 million as three pools with three different tax personalities. The sequence in which they are drained will decide whether the real annual number stays near $44,000 or drifts meaningfully higher over the next 20 years.

Contact [email protected] for any questions or corrections.