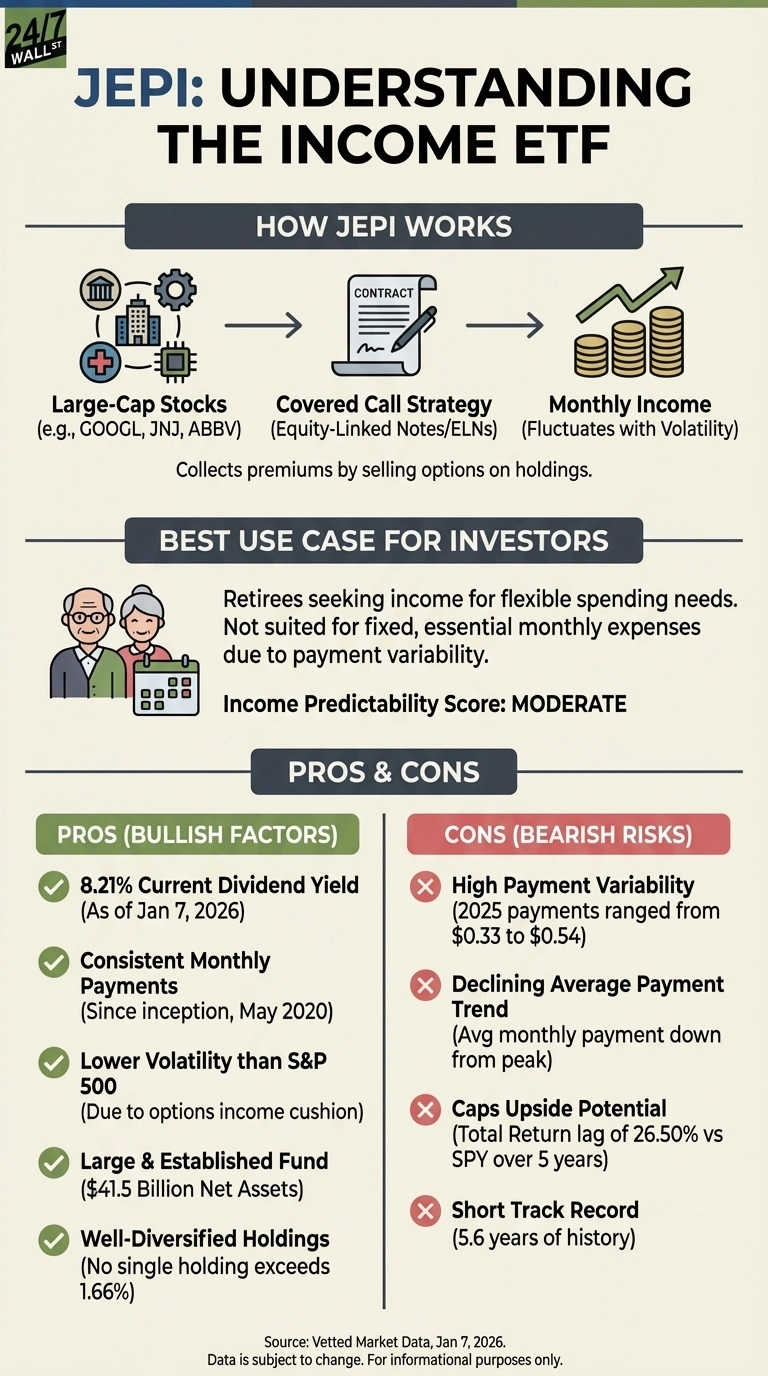

JPMorgan Equity Premium Income ETF (NYSEARCA:JEPI) has become a retiree favorite with its 8.21% yield and monthly distributions. The $41.5 billion fund delivers income through a covered call strategy using equity-linked notes (ELNs), collecting premiums by selling call options on a diversified portfolio of large-cap stocks. But can retirees count on this income stream remaining steady?

How JEPI Generates Income

JEPI employs a two-part approach: it holds roughly 130 large-cap stocks while simultaneously selling call options through ELNs. These equity-linked notes package covered call positions into contracts that mimic traditional covered calls. When volatility increases, option premiums rise and JEPI collects more income. When markets are calm, premiums shrink and distributions decline. This creates the fund’s defining characteristic: variability.

The Income Consistency Problem

JEPI’s monthly payments fluctuate significantly. In 2025, distributions ranged from $0.33 to $0.54 per share, a 66% swing from lowest to highest. December’s payment of $0.43 represented a 15% increase from November’s $0.37, but both fell below the June peak. This variability makes budgeting difficult for retirees with fixed monthly expenses.

The underlying portfolio provides some stability. Top holdings include Alphabet (NASDAQ:GOOGL | GOOGL Price Prediction) at 1.66%, Johnson & Johnson (NYSE:JNJ) at 1.64%, and AbbVie (NYSE:ABBV) at 1.63%. These quality names generate reliable dividends, but they contribute only a portion of JEPI’s total yield. The bulk comes from options premiums, which depend on market volatility and the fund manager’s ability to capture it efficiently.

Total Return Reality

While the 8.21% yield attracts attention, retirees must consider total return. JEPI returned 8.56% over the past year compared to 17% for the S&P 500. The covered call strategy caps upside participation during rallies. Since inception in May 2020, JEPI has delivered approximately 9.8% annualized returns versus 13.2% for the S&P 500. Retirees trading growth for income should understand this tradeoff.

The Safety Assessment

JEPI’s income is sustainable but not predictable. The fund has never missed a monthly payment since inception, and its $41.5 billion in assets provides operational stability. The 0.35% expense ratio is reasonable for active management. However, retirees cannot rely on consistent monthly amounts. Those needing $2,000 monthly for fixed expenses may receive anywhere from $1,900 to $3,100 depending on market conditions.

Consider JEPQ as an Alternative

For retirees seeking higher yield with more volatility tolerance, JPMorgan Nasdaq Equity Premium Income ETF (NASDAQ:JEPQ) offers 11.52% yield using the same covered call strategy on Nasdaq-100 stocks. JEPQ concentrates 41.7% in technology versus JEPI’s 14.6%, creating higher income potential but greater price swings. JEPQ holds $31.9 billion in assets and charges the same 0.35% expense ratio. JEPQ’s enhanced yield comes with tech-heavy exposure and similar income variability to JEPI.