A 62-year-old retiree with $1.8 million faces a reality few anticipate: when they stop working matters as much as how much they’ve saved. The culprit is sequence-of-returns risk, where early retirement losses can permanently impair portfolio sustainability even when markets eventually recover.

One Reddit user planning to retire in 2026 at 55 captured this tension: “I do think at times about retiring at what could be near the top of the market. But I’m not all that worried about what’s commonly referred to around here as SORR.” Their solution? Building spending flexibility into their budget rather than timing the market.

| Scenario Element | Details |

|---|---|

| Portfolio Value | $1.8 million |

| Retirement Age | 62 years old |

| Key Risk | Sequence-of-returns impact on withdrawal sustainability |

| Current Market | SPY near $749 (mid-July 2026, off the June 2026 high of $760) |

The Math That Reveals the Danger

The SPDR S&P 500 ETF Trust (NYSEARCA:SPY) hit a 52-week low of $618.05 in mid-July 2025, then climbed to a 52-week high of $760.40 by June 2, 2026, before settling near $749 in mid-July 2026. That recovery of more than 22% in roughly a year illustrates the upside a patient investor captured. For a retiree who started drawing down at last summer’s low, however, the picture looks very different from one who retired at the June peak.

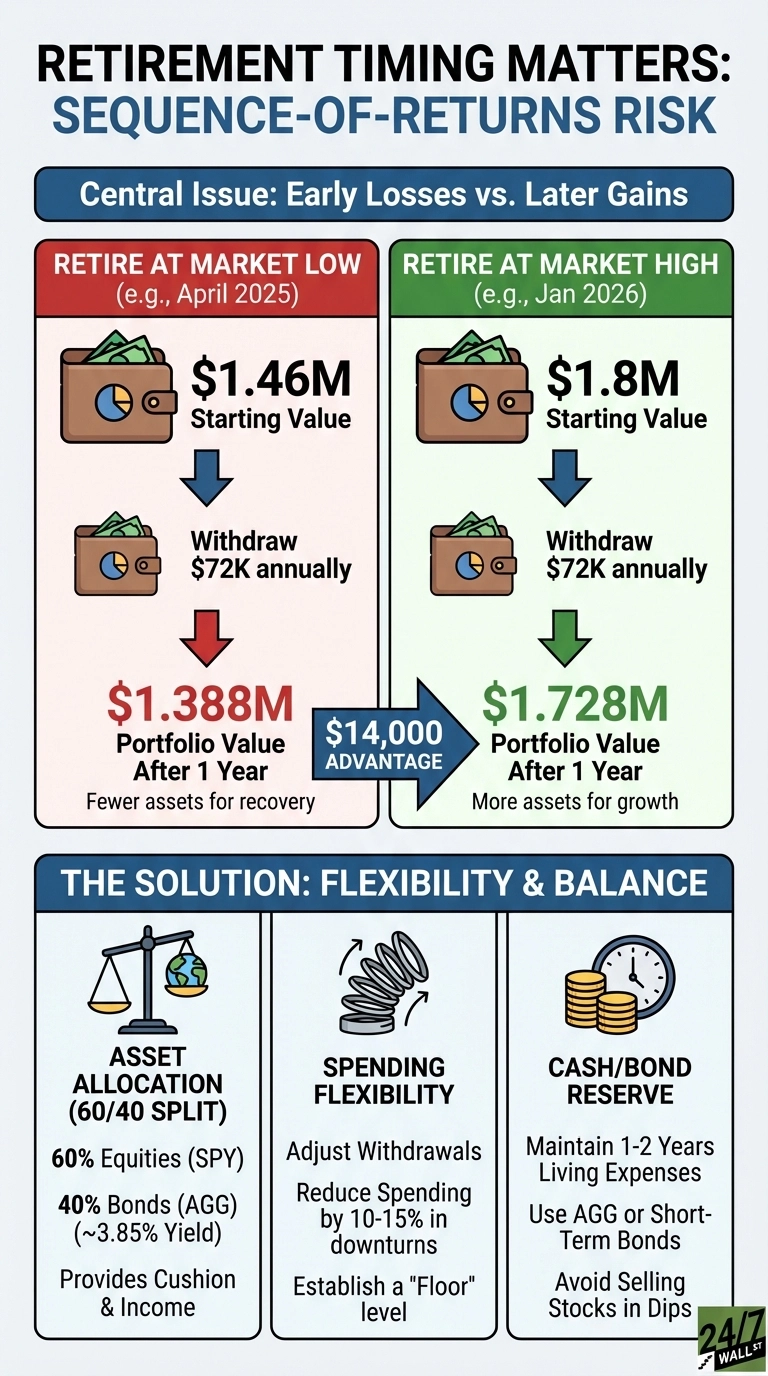

For a $1.8 million portfolio, this timing gap creates substantial structural variance from the opening day. Someone forced into withdrawals near the 2025 lows would have begun with a meaningfully smaller asset base, while a retiree entering at last year’s June high now faces a steeper cliff if a correction arrives quickly. The S&P 500 delivered roughly 17.9% in total return for full-year 2025, meaning anyone who retired before that rally locked in gains, but anyone drawing down into a sharp reversal immediately afterward faces the sequence problem head-on.

The damage compounds when static withdrawals begin. A traditional 4% rule means pulling $72,000 annually from a $1.8 million base. When markets drop early in retirement, the retiree is forced to sell more shares to generate that cash, permanently shrinking the asset base that could otherwise recover when prices rebound. As Schwab notes, “Not only does that drain your savings more quickly, but it also leaves you with fewer assets that can generate growth and returns during potential future recoveries.”

The “Guardrails” Framework Override

Generic asset shifts provide a basic cushion, but mitigating true sequence risk demands systematic execution rules. Jonathan Guyton and William Klinger’s Decision Rules establish absolute guardrails for a $1.8 million asset base, requiring a retiree to track their current withdrawal rate dynamically against the initial 4% benchmark. Research by Wade Pfau quantifies why precision matters here: the returns earned in the first ten years of retirement account for roughly 77% of the final long-term outcome, which means early guardrail triggers are far more consequential than late ones.

The Capital Preservation Rule is straightforward. If a sharp market drop pushes the withdrawal rate more than 20% above its starting level, crossing the 4.8% threshold, the retiree automatically implements a 10% spending reduction. The Prosperity Rule runs the opposite direction: if portfolio growth causes the active withdrawal rate to fall 20% below the starting point, dropping under 3.2%, spending can scale upward to capture equity gains safely. That removes the paralysis that often comes with retiring into near-record market levels.

Strategic Paths: Dynamic Buffers over Fixed Rules

The right goal is not to avoid retiring during volatility. It is to build specific withdrawal flexibility into the plan from day one. A balanced 60/40 portfolio split between equities (SPY) and bonds (the iShares Core U.S. Aggregate Bond ETF (NYSEARCA:AGG)) provides a concrete buffer. With AGG carrying a 30-day SEC yield near 4.5%, the fixed-income sleeve generates dependable income without requiring capital liquidation during equity drawdowns. Morningstar’s 2026 retirement income research supports this logic: portfolios with equity allocations above 50% can sustain only a 3.9% withdrawal rate at 90% success over 30 years, meaning the bond allocation is not just defensive padding but a structural necessity.

Rather than holding a static cash drag, consider a Valuation-Based Cash Buffer strategy. When equity forward multiples and index levels approach historic thresholds, retirees expand their defensive allocation to a full three years of living expenses. When a structural correction occurs, the buffer is deliberately drawn down to zero without being refilled from equities, fully insulating the core equity allocation through a typical 18-to-24-month recovery cycle.

De-Risking via the Discretionary “Floor”

To balance math with behavioral realities, retirees benefit from defining a non-discretionary spending floor explicitly. This means separating outlays into a baseline survival budget (housing, healthcare, basic food) and a variable lifestyle budget (travel, leisure). If a retiree’s household floor is $50,000 and guaranteed mechanisms like Social Security cover $30,000, the portfolio only needs to bridge a net $20,000 gap during an active market crisis. That kind of precision sharply reduces the emotional weight of short-term market tracking and keeps the guardrails from being abandoned at precisely the wrong moment.

What to Evaluate Now

Financial advisors typically focus on three factors when stress-testing a sequence-of-returns exposure: spending flexibility (the ability to reduce expenses by 15-20% during market stress), asset allocation (balanced portfolios with 30-40% in bonds rather than a pure equity position), and retirement timing relative to current valuations. Building in automated decision guardrails, dynamic cash buffer targets, and a segregated spending floor addresses all three simultaneously.

The core mistake is assuming that $1.8 million behaves identically regardless of when withdrawals start. The data, and the math, say otherwise.

Editor’s note: This article was updated to reflect SPY’s current trading level near $749 and its 52-week high of $760.40 reached on June 2, 2026, replacing the earlier May 2026 figure of $741.25. The AGG 30-day SEC yield was revised to approximately 4.5% based on June 2026 data. New context was added on the S&P 500’s roughly 17.9% total return for full-year 2025, Morningstar’s 2026 finding of a 3.9% safe withdrawal rate for equity-heavy portfolios, and Wade Pfau’s research showing the first decade of retirement drives about 77% of long-term portfolio outcomes.

Contact [email protected] for any questions or corrections.