A lot of people reach retirement age without much money saved. But if you worked hard and built a genuine nest egg, your challenge shifts from accumulating wealth to deploying it wisely. Managing withdrawals carefully can matter just as much as the years of saving that preceded them.

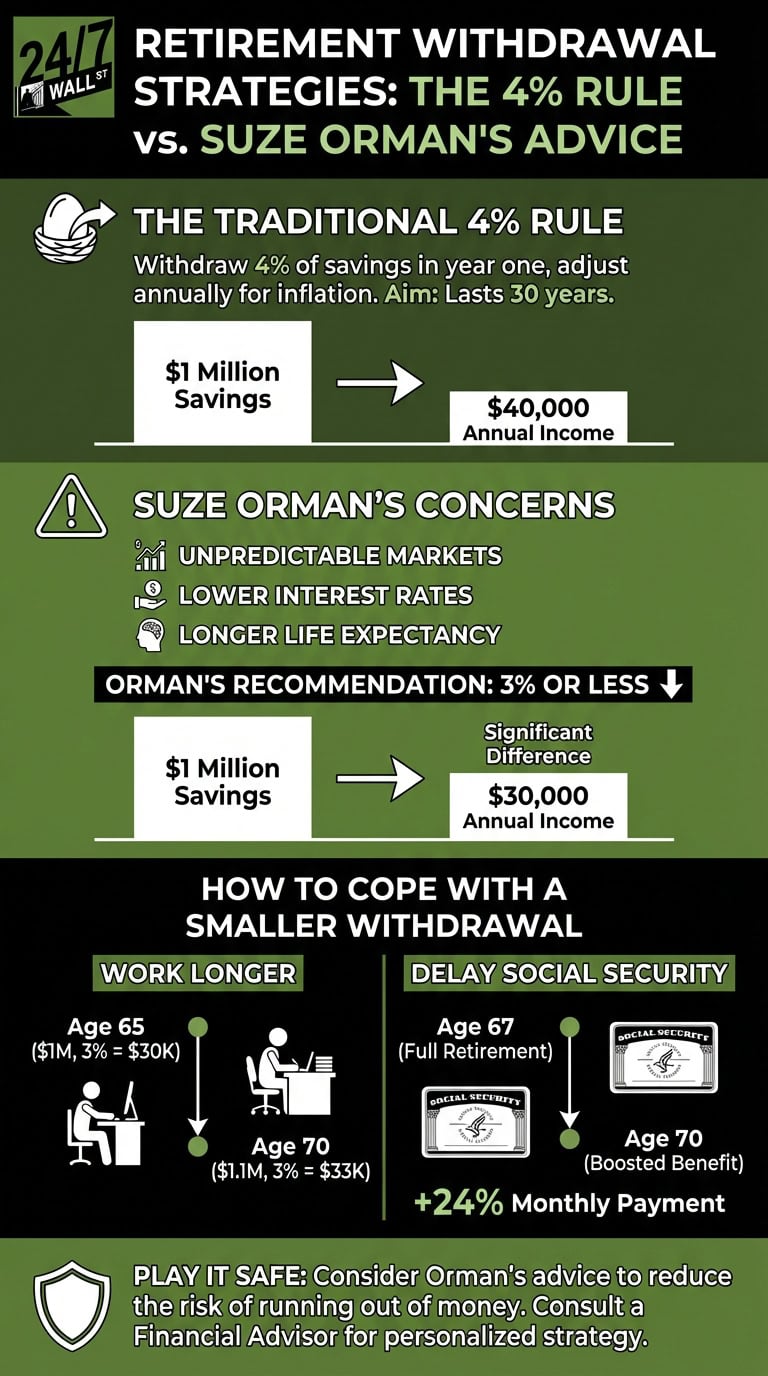

Many financial experts recommend a strategy called the 4% rule. It calls for withdrawing 4% of your savings balance in your first year of retirement, then adjusting each subsequent withdrawal for inflation. Financial planner Bill Bengen developed the rule in 1994, basing it on historical market returns from a balanced portfolio of roughly 50% stocks and 50% bonds. Followed faithfully, the strategy is designed to give your savings a high probability of lasting 30 years. Many financial insiders remain fans of the rule. Suze Orman is not among them.

Orman believes the 4% rule no longer serves today’s retirees well, and she recommends a fundamentally different approach to managing withdrawals.

Why Orman thinks the 4% rule is a problem

The 4% rule rests on assumptions that may no longer hold. It was calibrated to a specific interest-rate environment and a particular asset mix that prevailed decades ago. Orman argues that markets are unpredictable, that interest rates have shifted considerably since Bengen’s original research, and that Americans simply live longer than they did in 1994. That combination, in her view, makes the 4% rule genuinely risky for anyone who could spend 30 or 40 years in retirement.

Orman therefore recommends starting with a 3% withdrawal rate, or even less, depending on how the portfolio is invested. For a retiree with $1 million in savings, that translates to $30,000 a year instead of $40,000. Bridging that $10,000 gap requires deliberate planning, but several modern strategies make it more manageable. Independent research from Morningstar is consistent with Orman’s caution: the firm’s 2025 State of Retirement Income report puts the safe starting withdrawal rate at 3.9% for a 30-year horizon (up slightly from 3.7% in 2024), suggesting the debate is very much alive and the right number depends heavily on market conditions at the moment of retirement.

Modern strategies to cope with smaller withdrawals

Running out of money ranks among the most common fears retirees express. A lower withdrawal rate, however, does not have to mean a lower quality of life. Several legislative and planning tools can help close the gap.

Utilize SECURE 2.0 “Super Catch-Ups”

Orman recommends working longer to keep your nest egg growing. Under current tax law, those extra years are more rewarding than ever. SECURE Act 2.0 allows workers who turn ages 60, 61, 62, or 63 during the calendar year to make super catch-up contributions to their employer-sponsored retirement plans. For both 2025 and 2026, that enhanced limit is $11,250. Workers aged 50 and older who fall outside that 60-to-63 window can contribute up to $7,500 in extra catch-up dollars in 2025 and $8,000 in 2026. Directing those additional dollars into a tax-advantaged account during your final working years can meaningfully increase the nest egg you carry into retirement.

Implement Dynamic Guardrails

Rather than locking into a rigid 3% or 4% rate from day one, many planners now favor a “dynamic guardrails” approach. The idea is straightforward: withdrawals rise when the portfolio is performing well, but you commit in advance to pulling back if the balance falls below a predetermined floor. That built-in flexibility can support a higher starting withdrawal than the strict 3% Orman recommends, while still protecting against the sequence-of-returns risk that can devastate a portfolio in a rough early stretch. Morningstar’s 2025 research found that a guardrails strategy applied to a 40% equity / 60% bond portfolio can support a starting withdrawal rate of 5.2%, and that retirees who pair guardrails with delayed Social Security can push that figure as high as 5.7%. The trade-off is a willingness to accept some year-to-year variability in spending, which is most tolerable for retirees whose fixed living expenses are already covered by income sources outside the portfolio.

Beware the IRMAA Surcharge

One of the most underappreciated threats to retirement income is the Income-Related Monthly Adjustment Amount (IRMAA). Medicare uses your Modified Adjusted Gross Income (MAGI) from two years prior to determine whether you owe a surcharge on top of your standard Part B and Part D premiums. In 2026, the standard Part B premium is $202.90 per month, up from $185.00 in 2025. IRMAA kicks in once MAGI exceeds $109,000 for single filers or $218,000 for married couples filing jointly, up from $106,000 and $212,000 in 2025. Because IRMAA operates as a cliff (crossing a threshold by even one dollar triggers the full surcharge for that tier), coordinating withdrawal amounts and Roth conversion timing with these brackets can preserve thousands of dollars each year.

Income Layering and Synthetic Dividends

A growing number of retirees are turning to “income layering” to reduce their dependence on portfolio withdrawals. This approach combines Social Security, bond ladders, and options-based income strategies (sometimes called synthetic dividends) to build a reliable cash-flow floor. Writing covered calls on existing stock holdings, for example, can generate income without forcing a sale of shares, which is especially valuable during market downturns when selling at depressed prices would lock in losses.

Maximizing Social Security

Orman is a firm advocate of delaying Social Security until age 70. For workers whose full retirement age is 67, waiting until 70 permanently increases their monthly benefit by 24%, reflecting an 8% boost for each of the three additional years. That guaranteed, inflation-adjusted income acts as a counterweight to a lower portfolio withdrawal rate and significantly reduces the risk that the portfolio runs dry in the later decades of retirement. Morningstar’s research reinforces this point: delaying Social Security pairs especially well with flexible withdrawal strategies, because it shrinks the share of spending that depends on volatile market returns. Congress is also paying closer attention to how people understand these choices: legislation proposed in 2025 would rename age 70 the “maximum benefit age” in Social Security communications, an acknowledgment that the current terminology obscures the financial advantage of waiting.

Talking with a financial advisor about your specific circumstances is always worthwhile. A good advisor can assess your portfolio mix, project your income needs, and design a tiered income plan that balances steady cash flow with long-term principal preservation.

Editor’s note: This update adds Morningstar’s finding that a guardrails strategy can support a 5.2% starting withdrawal rate (and up to 5.7% with delayed Social Security), and notes that the 2026 IRMAA income thresholds rose to $109,000 for single filers and $218,000 for joint filers, up from $106,000 and $212,000 in 2025. The Social Security section was expanded to include the 2025 Claiming Age Clarity Act proposal, which would designate age 70 as the “maximum benefit age.”

Contact [email protected] for any questions or corrections.