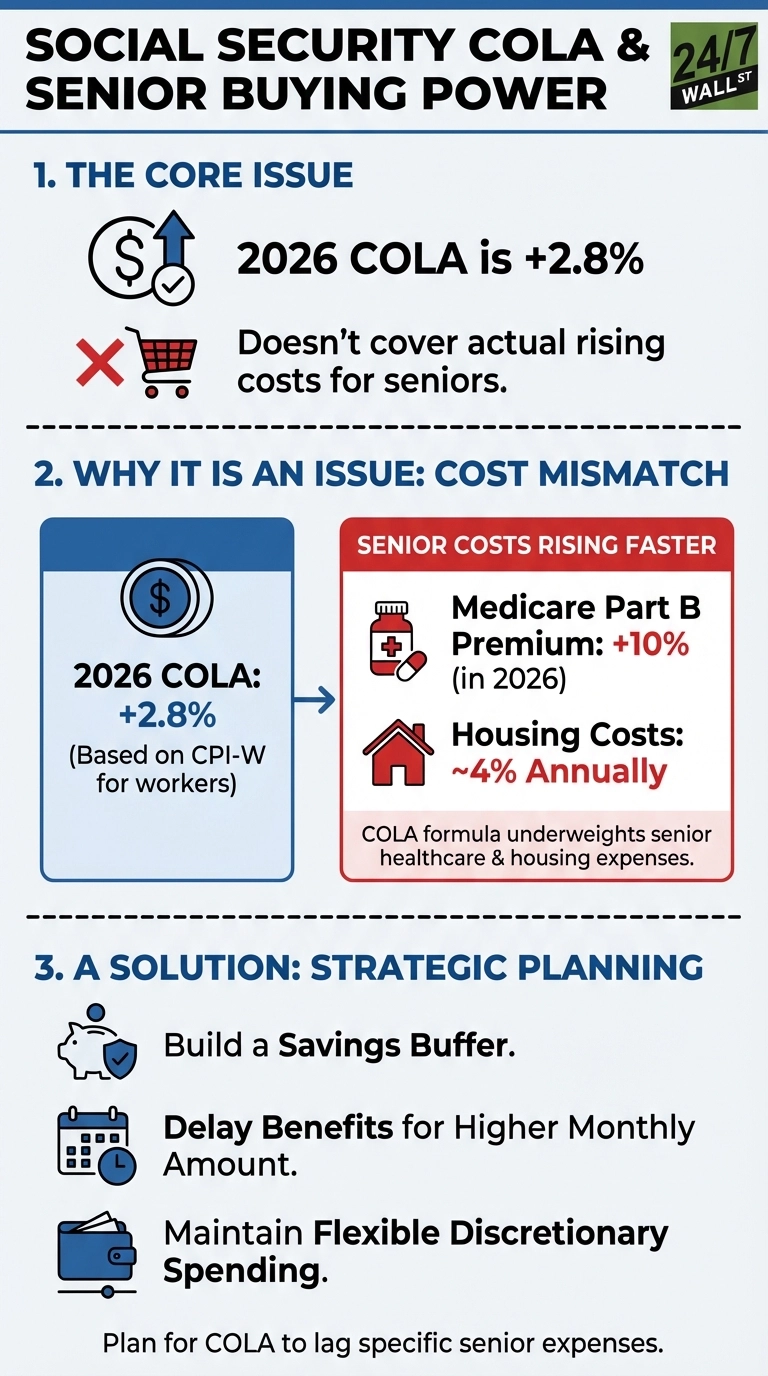

When the Social Security Administration announces the annual cost-of-living adjustment each October, many retirees feel relieved. The 2.8% increase for 2026 sounds like protection against inflation. But for millions of beneficiaries, that adjustment doesn’t quite cover the rising costs they actually face.

The issue comes down to how COLA is calculated and what expenses matter most in retirement. Social Security uses the Consumer Price Index for Urban Wage Earners and Clerical Workers, known as CPI-W. This index tracks spending patterns of working Americans under age 62, not retirees. The calculation compares third-quarter averages from one year to the next, and the SSA announces the result every October.

That methodology creates a mismatch. Working-age consumers spend differently than retirees do. Healthcare represents a much larger share of senior budgets, yet it carries less weight in the CPI-W formula. Housing costs also hit retirees hard, particularly those who rent or face rising property taxes and maintenance expenses.

Medicare Part B premiums illustrate the problem. The monthly premium jumped to $202.90 in 2026, a 10% increase from the prior year. This single expense consumed a significant portion of the 2.8% COLA before beneficiaries could address any other rising costs, demonstrating how healthcare inflation creates unique pressure on senior budgets that general inflation measures don’t fully capture.

Housing costs for seniors have climbed around 4% annually in recent years, consistently outpacing COLA adjustments. Combined with healthcare expenses that dominate senior budgets, this creates a cost structure that diverges sharply from the spending patterns of younger workers used to calculate COLA. The Bureau of Labor Statistics tracks an experimental index for Americans 62 and older that reflects this reality, consistently rising faster than the CPI-W used for Social Security adjustments.

This gap matters most for beneficiaries living primarily on Social Security. When your monthly check represents your main income source, even a 1% difference between COLA and actual expenses erodes buying power over time. The effect compounds year after year.

Understanding this dynamic helps with planning. If you’re approaching retirement, assume Social Security will maintain its nominal value but may not fully keep pace with your specific expenses. Building a buffer in savings, delaying benefits to increase your monthly amount, or maintaining flexibility in discretionary spending can offset the gradual squeeze. The COLA provides valuable protection, but it’s designed around a different household than yours.

Contact [email protected] for any questions or corrections.