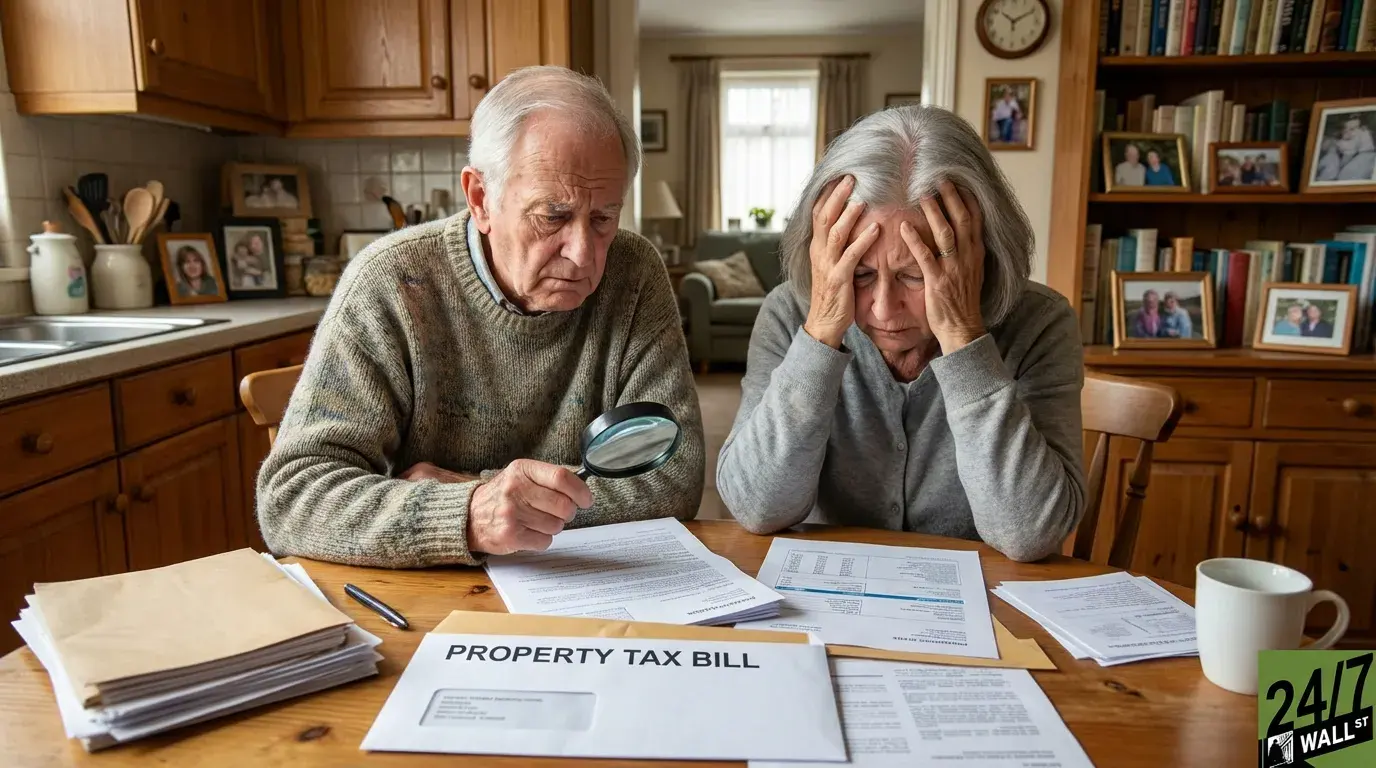

Retirees who spent decades paying off their homes now face an unexpected financial squeeze: property tax bills that keep climbing even as their incomes remain fixed. This challenge has intensified as home values surged during the pandemic era, triggering reassessments that ignore retirement budget realities.

The Fixed-Income Trap

The scenario plays out across the country: retirees living on fixed Social Security and pension income watch their property tax bills double or triple as home values surge. While appreciation looks impressive on paper, it translates to tax obligations that consume an ever-larger share of monthly budgets.

The math becomes brutal when property taxes claim a significant portion of fixed income. Meanwhile, inflation rose 2.0% year-over-year through December 2025, eroding purchasing power on essentials like groceries, utilities, and healthcare.

Why Taxes Keep Rising

Property taxes operate through assessed values and millage rates. Your local assessor determines your home’s market value, then applies a millage rate—typically expressed as dollars per $1,000 of assessed value. As home values rise, tax bills increase proportionally.

States reassess properties on varying schedules, from annual to five-year cycles, though some wait up to 10 years. The problem: real estate values measured by the Vanguard Real Estate ETF climbed 53% from 2005 through early 2026, with a particularly sharp spike during 2020-2021. Many retirees now face tax bills based on peak valuations, even as housing starts fell 16.4% year-over-year, signaling potential market softening ahead.

Relief Programs Worth Pursuing

Many states offer homestead exemptions that reduce assessed values for primary residences. Some jurisdictions provide additional senior exemptions or property tax freezes for homeowners over 65 meeting income thresholds.

California’s Property Tax Postponement Program allows seniors to defer current-year taxes as a lien against the home, payable when the property sells. Other states offer circuit breaker programs that cap property taxes as a percentage of income.

Strategic Responses

Research your state and county programs immediately. Application deadlines often fall early in the tax year, and missing them means waiting another 12 months. Appeal your assessment if comparable sales suggest your home is overvalued—assessors make mistakes, and successful appeals can save thousands.

For those facing unmanageable bills, downsizing to a smaller home or relocating to a lower-tax jurisdiction may be necessary. While emotionally difficult, this beats depleting retirement savings or taking on debt to cover annual tax obligations.