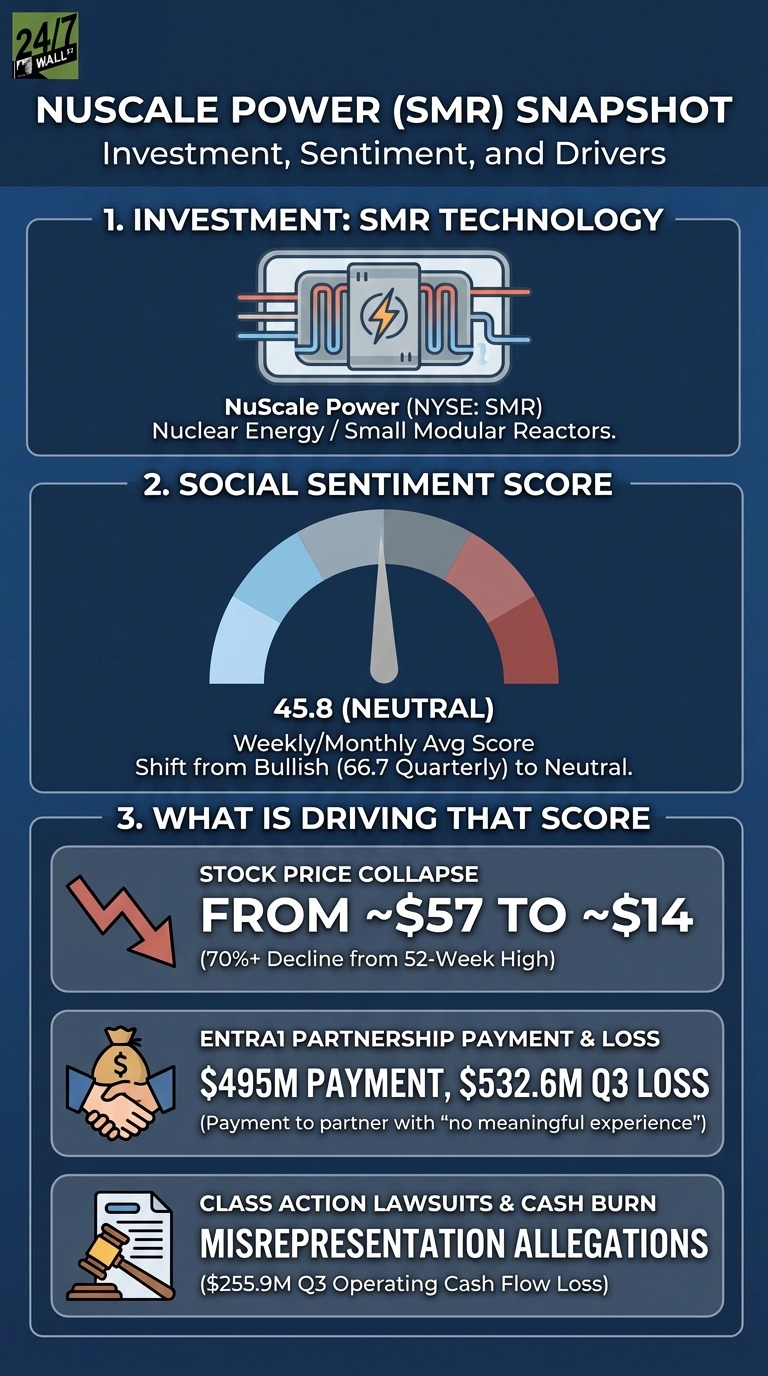

Over the last few months, the market has seen NuScale Power (NYSE:SMR) collapse from $57.42 to $14.24, erasing approximately 75% of shareholder value. You don’t even have to dig that deep to learn that the culprit wasn’t a failed reactor test or regulatory setback, but that the company bet its commercialization strategy on a partner that allegedly had no meaningful experience in nuclear power.

The ENTRA1 Problem That Broke the Stock

One catalyst for this stock move was NuScale’s Q3 2025 earnings, which revealed a $495 million milestone payment to ENTRA1 Energy, its global commercialization partner. That payment caused general and administrative expenses to balloon more than 3,000%, pushing the quarterly net loss to $532.6 million. Of course, the real shock came when multiple class action lawsuits alleged that ENTRA1 had never built, financed, or operated any significant nuclear projects. According to the complaints, NuScale misrepresented ENTRA1’s capabilities to investors during the May 13 to November 6, 2025, class period. Investors have until April 20, 2026, to apply as lead plaintiff.

Retail investor reaction to these developments has been sharply divided. On r/wallstreetbets, one post asked ‘Is there any hope for $SMR / $OKLO ?’ with commenters debating the uncertainty around the ENTRA1 partnership and whether NuScale could recover, with one commenter noting the stock had become “a waiting game on whether management can actually deliver a signed contract.” Separately, on r/stocks, a post titled ‘Nuclear. Are you in or out?’ drew 225 upvotes and 265 comments, with one commenter writing: “The technology is real, but the timeline keeps slipping — hard to stay bullish when cash burn is this severe.” The thread reflected a broad debate over the sector’s investment case.

Is there any hope for $SMR / $OKLO ?

by u/[username] in wallstreetbets

Nuclear. Are you in or out?

by u/[username] in stocks

The Tennessee Valley Authority agreement for up to 6 gigawatts of SMR capacity was supposed to validate the ENTRA1 partnership and it exposed the company’s reliance on an unproven partner, triggering a crisis of confidence.

Analysts Still See 140% Upside Despite the Wreckage

The big takeaway here is that Wall Street hasn’t given up, as the current consensus price target sits at $33.96, implying 140% upside from current levels, with 6 buy ratings, 8 holds, and 2 sells. NuScale remains the only SMR design with U.S. NRC approval and has 12 modules already in production with supplier Doosan.

The bull case hinges on government support for nuclear and AI-driven data center demand. The problem is that NuScale’s Romania project won’t reach commercial operations until July 2033, the TVA deal is non-binding, and trailing twelve-month revenue is just $64 million against a $4.14 billion market cap.

What Could Derail the Recovery

For now, three risks stand out as the ENTRA1 lawsuits create a legal and reputational overhang that could drag on for years. NuScale is burning $255.9 million per quarter in operating cash flow and surviving on equity dilution, selling 13.2 million shares in Q3 alone. And despite NRC approval, regulatory timelines remain slow while competitors like Oklo (NYSE:OKLO | OKLO Price Prediction) close the gap.

NuScale’s technology may be real, but the path from approval to profitable operations is proving far longer and more expensive than the market anticipated. Until the company signs binding contracts with creditworthy customers and demonstrates a clear path to positive cash flow, questions about its long-term viability are likely to persist.

Contact [email protected] for any questions or corrections.