Both Lowe’s (NYSE: LOW | LOW Price Prediction) and TJX Companies (NYSE: TJX) reported Q4 results before the bell on Wednesday, but morning trading revealed a clear split verdict. Both beat expectations, but TJX traded higher while Lowe’s pulled back. Here’s where things stand midday.

Lowe’s: Acquisition Growth, but Guidance Falls Short

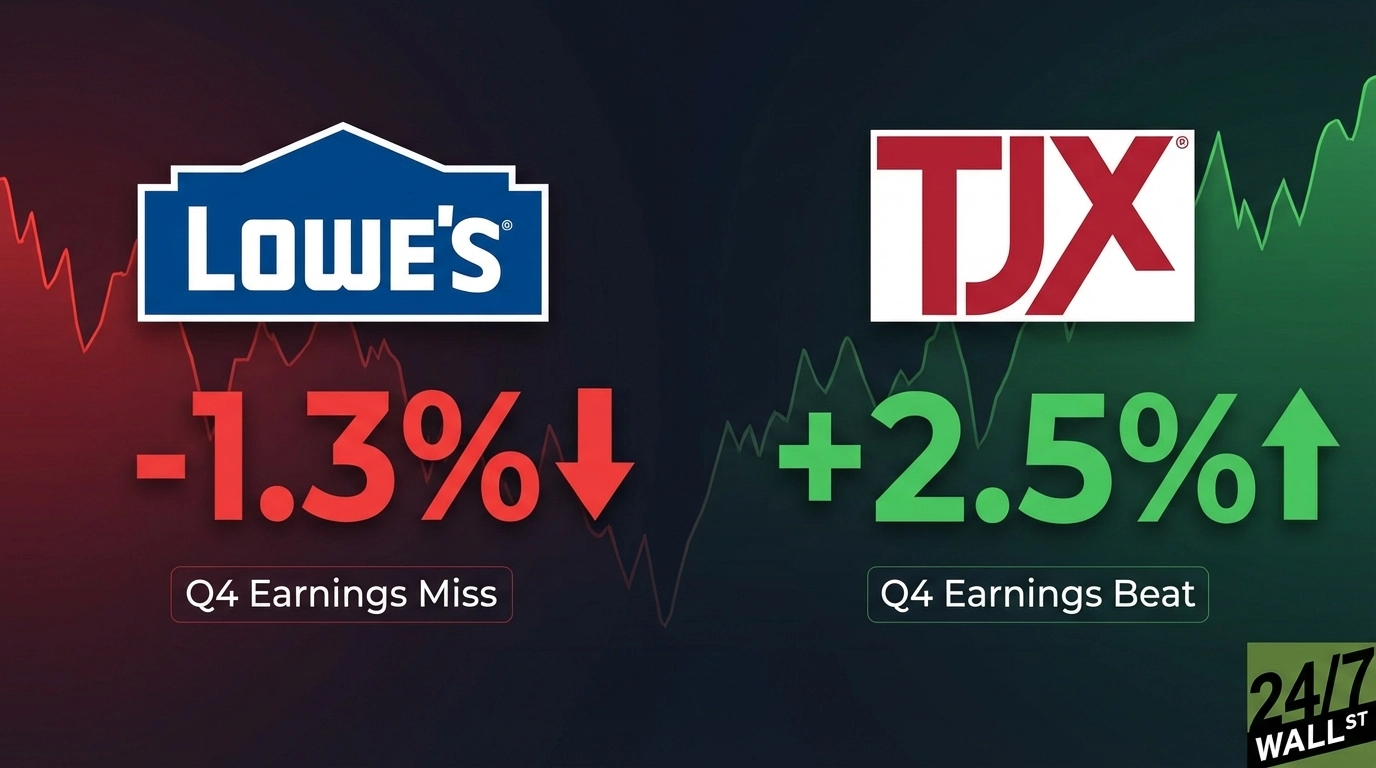

Ahead of the report, the housing macro was the central question for Lowe’s. The answer came through in the numbers. LOW is trading at $266.25 in the late morning, down from $269.65 at filing, reflecting investor disappointment with the results and guidance.

- Adjusted EPS came in at $1.98, topping the $1.94 estimate by roughly 2%.

- Revenue of $20.58 billion grew 10.9% year over year, though that growth was largely acquisition-driven via FBM and ADG.

- Comparable sales rose just 1.3%, with Pro, online, and home services as the primary contributors.

- Adjusted operating margin contracted 41 basis points year over year to 9.02%.

For FY26, Lowe’s guided to total sales of $92 billion to $94 billion and adjusted EPS of $12.25 to $12.75. The midpoint of that EPS range is essentially flat with FY25’s $12.28, which likely explains the muted market reaction. Moreover, housing starts declined 5.8% year over year through December 2025, giving CEO Marvin Ellison’s cautious tone real macro grounding. Ellison noted: “While the housing macro remains pressured, we are focused on directing what is within our control.”

TJX: Strong Beat, Shares Respond

TJX delivered the cleaner story. TJX is trading at $158.87, up from $155.29 at filing, as investors rewarded a broad-based beat.

- Adjusted EPS of $1.43 beat the $1.39 estimate (the GAAP figure of $1.58 includes a one-time $221M litigation settlement and is not the cleaner operating comparison)

- Comparable sales grew 5%, well above plan, with HomeGoods up 6% and TJX Canada up 7%

- Adjusted pretax profit margin expanded 60 basis points to 12.2%

- Full-year revenue crossed $60B for the first time

Management’s tone was notably confident. CEO Ernie Herrman said, “the first quarter is off to a strong start and availability of quality merchandise continues to be outstanding.” For FY27, TJX guided to comp sales growth of 2% to 3% and adjusted EPS of $4.93 to $5.02, alongside a 13% dividend increase to $0.48 per share. With consumer sentiment down 12.8% year over year as of January 2026, the off-price value proposition continues to work in TJX’s favor.

What to Watch Next

For Lowe’s, the key question is whether the Pro customer segment and online momentum can offset a still-pressured housing market through FY26. For TJX, watch whether the strong Q4 comp trajectory carries into Q1 guidance delivery, and how analysts revise price targets following this morning’s beat.

Contact [email protected] for any questions or corrections.