Lowe’s (NYSE:LOW | LOW Price Prediction) just delivered its fourth consecutive quarter of positive comp sales, yet the stock sits 9.01% lower year-to-date and 13.02% off its April peak. That disconnect is the foundation of our call.

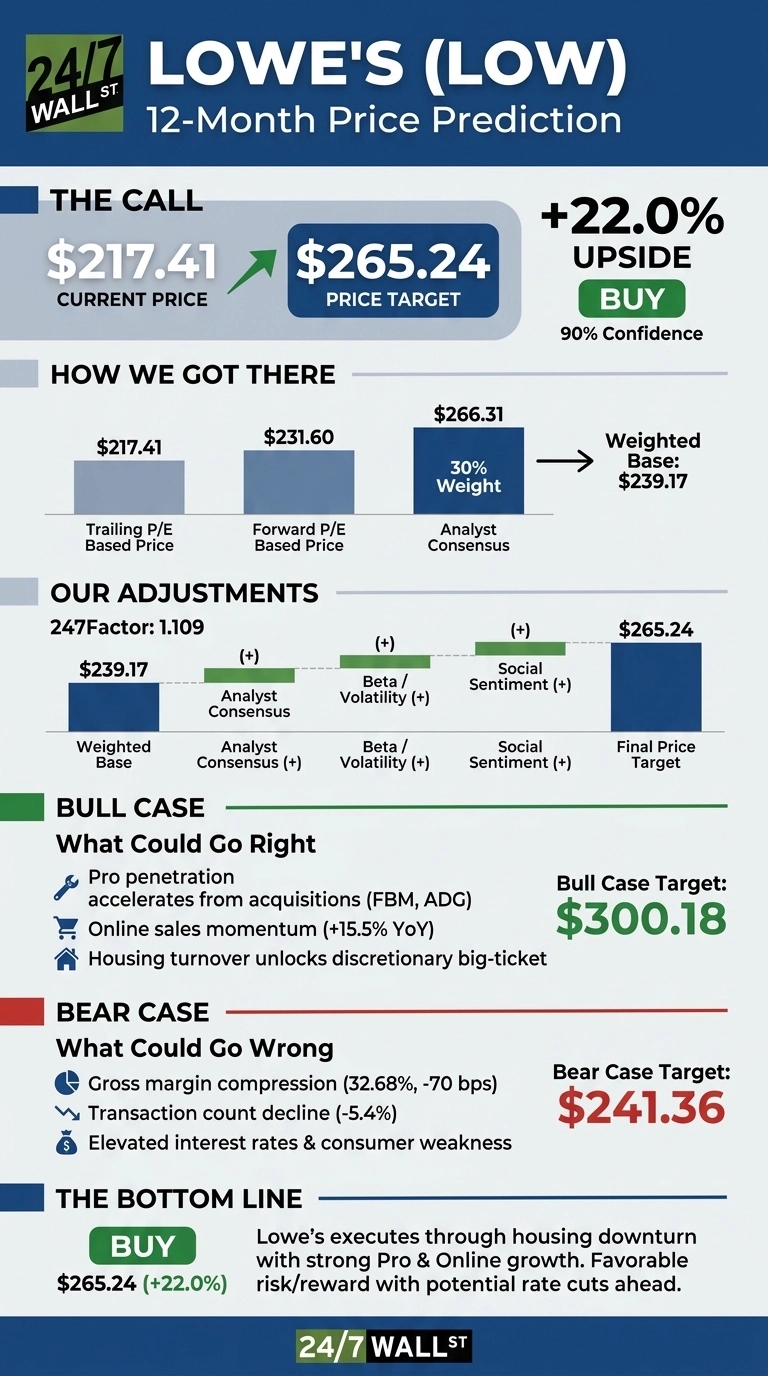

Our 24/7 Wall St. price target for Lowe’s is $265.24 over the next 12 months, implying 22% upside from the current $217.41. The recommendation is buy, with high confidence at 90%.

| Metric | Value |

|---|---|

| Current Price | $217.41 |

| 24/7 Wall St. Price Target | $265.24 |

| Upside | 22.0% |

| Recommendation | BUY |

| Confidence | 90% |

A Spring Selling Season That Beat the Mood

The selloff has been sharp. LOW is down 2.77% over the past week and 2.51% over one year, even as the broader story improved.

Q1 FY27 results, reported May 20, 2026, showed revenue of $23.08 billion, up 10.3% YoY, lifted by the Foundation Building Materials and Artisan Design Group acquisitions. Adjusted EPS of $3.03 narrowly missed the $3.06 consensus, comparable sales rose 0.6%, and online grew 15.5%.

CEO Marvin Ellison framed the quarter directly: “Strong spring execution and continued momentum in Pro, Appliances, Online, and Home Services supported a solid start to the year.”

Management affirmed FY2026 guidance for $92B to $94B in sales and adjusted EPS of $12.25 to $12.75. Shares trade at roughly 19x earnings, a discount we view as unjustified given guidance integrity.

The Case for $300+

Our bull case lands at $300.18, a 38.07% total return. The thesis: Pro penetration accelerates as the $8.8B Foundation Building Materials and $1.31B Artisan Design Group deals deliver synergies.

Online momentum at +15.5%, the $250M tradesperson training program, and the Mylow AI advisor (5M associate questions) all expand the addressable wallet. If mortgage rates ease alongside expected Fed cuts, housing turnover unlocks the discretionary big-ticket purchases currently in hibernation.

Analyst sentiment supports this scenario, with 22 buy ratings against just 1 sell, and insider activity tilts net buying across 27 recent transactions.

The Risks Worth Watching

Our bear case targets $241.36, an 11.02% return. The risks are concrete: gross margin compressed 70 bps to 32.68% on intangible amortization, comp transactions fell 0.9%, and the balance sheet now carries -$9.27B in shareholders equity with higher interest expense.

The counterfactual matters. That margin pressure stems from acquisition amortization, a non-cash item tied to deal integration. Gross profit still grew 15.34% YoY to $7.54B, and management is investing through a soggy housing cycle that JPMorgan research expects to remain rate-sensitive and soggy into 2026.

Lowe’s Price Prediction 2026-2030

The 24/7 Wall St. price target of $265.24, a buy at 90% confidence, rests on one tipping factor: Lowe’s is executing through the housing downturn while building Pro share that compounds when the cycle turns.

The bull thesis holds for investors with a 12 to 18 month horizon who expect Fed cuts to unlock housing turnover. The bear thesis holds if mortgage rates remain elevated through 2027 and consumer big-ticket weakness deepens.

Looking further out, here is where our model projects LOW could trade, extending the base case 12.72% annualized return.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $265.24 |

| 2027 | $276.24 |

| 2028 | $311.37 |

| 2029 | $350.98 |

| 2030 | $395.56 |

These projections assume Lowe’s continues executing on its Total Home strategy. Significant upside or downside could result from the housing cycle inflection or sustained pressure on big-ticket discretionary spending.

Contact [email protected] for any questions or corrections.