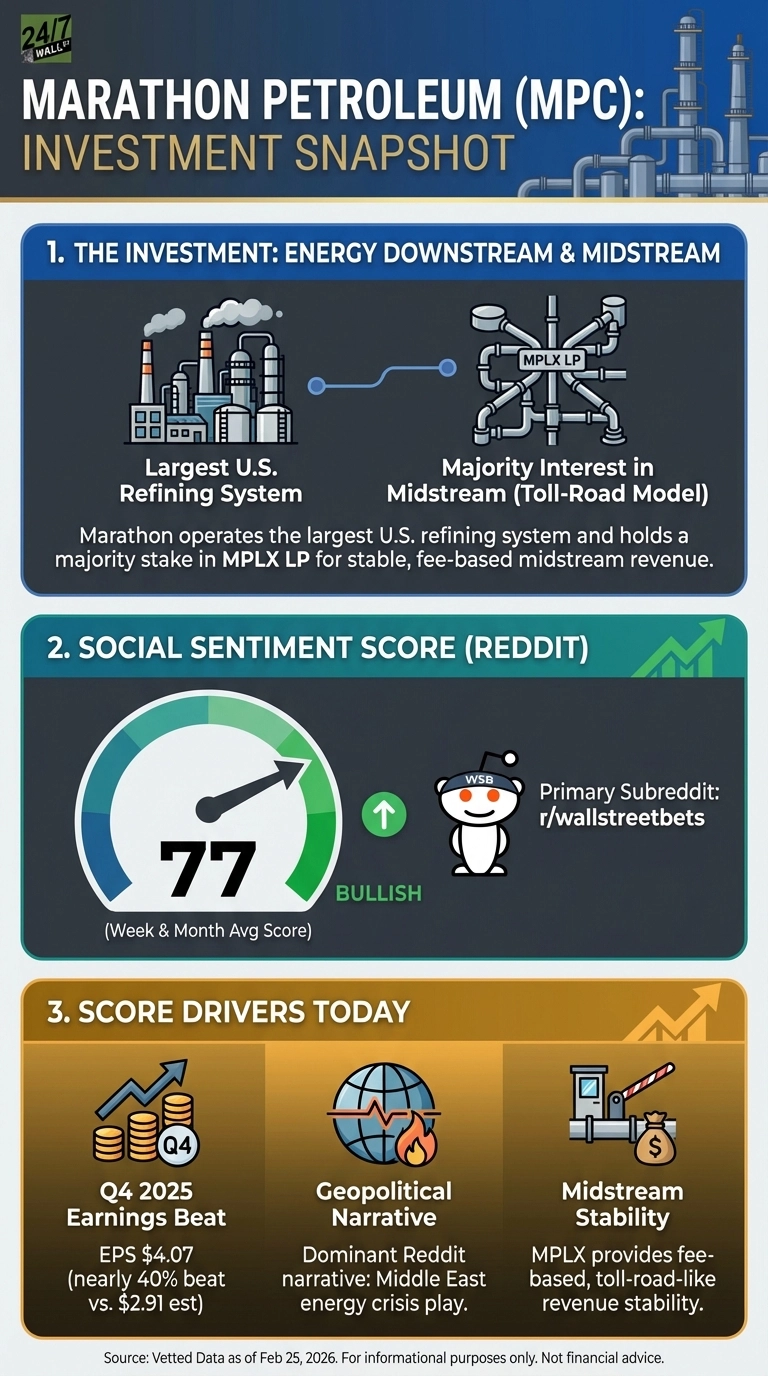

Marathon Petroleum might be a household name for retail investors, but it (NYSE:MPC) has climbed 19% year-to-date and more than 28% over the past year, with Reddit sentiment tracking right alongside it. Marathon’s proprietary Reddit sentiment score sits at 77 out of 100 on both a weekly and monthly basis, reflecting growing conviction around the company’s earnings power and its position straddling two valuable parts of the energy chain.

Marathon’s Q4 Earnings Just Changed the Conversation

As for the company’s Q4 numbers, it reported EPS of $4.07, nearly 40% above the consensus estimate of $2.91, while net income nearly doubled year-over-year to $1.5 billion from $371 million in Q4 2024. Full-year free cash flow totaled $8.3 billion, up 389% from the prior year, and the refining business ran at 95% utilization with a $18.65 per barrel margin.

What makes Marathon structurally interesting is the midstream layer. Through its majority stake in MPLX LP, Marathon collects fee-based revenue from gathering, processing, and transporting energy regardless of where crude prices sit. That segment generated $1.7 billion in EBITDA in Q4 2025, essentially flat quarter over quarter, providing a floor for earnings that pure refiners lack.

Why Reddit Is Paying Attention to Marathon Right Now

Discussion volume is low but conviction is high. A post on r/wallstreetbets titled “Buckle up for a Middle East Energy Crisis with Marathon Petroleum” has drawn 92 upvotes and 59 comments. The author writes: “Two massive US Gulf Coast export-oriented refineries positioned to capitalize on global refining crunch and clean product disruptions.”

Buckle up for a Middle East Energy Crisis with Marathon Petroleum

by u/gbaked in wallstreetbets

The Reddit bull case rests on three points:

- Marathon operates the largest U.S. refining system, giving it unmatched scale if global refining capacity tightens

- The MPLX midstream segment generates stable, fee-based cash flows that cushion earnings during commodity downturns

- $4.4 billion in remaining share repurchase authorization and a 10% dividend increase in Q3 2025 signal management’s confidence in sustained cash generation

Analyst Consensus Backs the Retail Thesis

BMO Capital raised its price target to $225 from $200 on February 9, 2026, maintaining an Outperform rating. Of the 13 analysts covering Marathon, not one rates it a Sell, and the consensus 12-month price target is $204.15. At a forward P/E of roughly 14x and a dividend yield near 2%, Marathon trades at a modest valuation relative to its cash generation capacity.