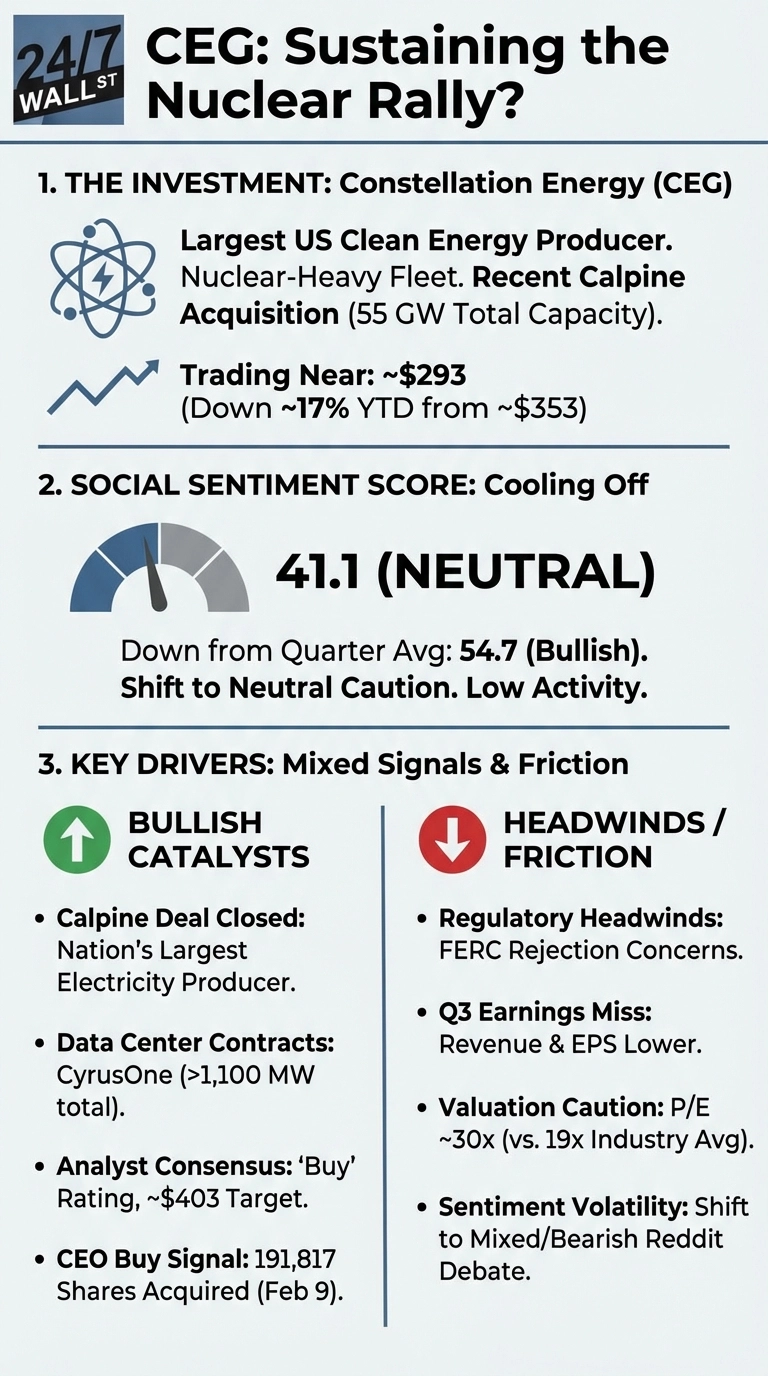

The largest producer of carbon-free energy in the United States, Constellation Energy (NASDAQ:CEG) is trading near $293, down 17% year-to-date after starting 2026 at on a high. Retail investor sentiment has cooled from 54.7 in the quarter to 41.1 this month, reflecting a shift from bullish conviction to neutral caution. This change in sentiment is arguably the result of a question facing investors: can the nation’s largest nuclear operator close the roughly $60 gap between its current price and its $353 starting price, or has the thesis fundamentally changed?

Why the Nuclear Story Hit Turbulence

Constellation’s pullback traces to two friction points, the first being FERC’s rejection of a behind-the-meter nuclear colocation deal between Amazon and Talen Energy in November 2024, which sent shockwaves through the sector. While Constellation wasn’t directly involved, the ruling raised questions about the viability of similar hyperscaler partnerships. Second, the company’s Q3 2025 earnings missed on both revenue ($6.57 billion vs. $6.63 billion estimate) and EPS ($3.04 vs. $3.13 estimate), with management narrowing full-year guidance to $9.05 to $9.45 per share.

Reddit discussion migrated from bullish options talk in r/stocks and r/options in January (sentiment scores of 73-78) to mixed debate in r/stockmarket by mid-February, where sentiment swung between 22 and 72 within 24-hour windows. In January, one r/stocks thread titled “Energy Plays – Tech, Space, Industrials, and even your mother’s basement need it” captured the bullish mood, with the post framing nuclear and energy infrastructure as essential to powering the next wave of tech and industrial growth. Meanwhile, an r/options post titled “CEG: Leveraging through Spreads + DCA” showed retail traders discussing options strategies around the stock, with the thread exploring spread structures and dollar-cost averaging approaches as ways to manage exposure. That volatility signals conflicting narratives rather than sustained conviction.

What’s Working: Calpine and Data Center Deals

Despite the headwinds, Constellation closed its Calpine acquisition on February 20, 2026, creating the nation’s largest electricity producer with 55 gigawatts of capacity serving 2.5 million customers. The company also signed a 380 MW agreement with CyrusOne in Texas, bringing total CyrusOne commitments above 1,100 MW.

As a result of these deals and other headwinds moving in Constellation’s favor, analyst support remains strong. For now, fourteen analysts maintain a consensus “Buy” rating, with 11 of 14 recommending “Buy” or “Strong Buy.” The $403 consensus price target is approximately 38% above current trading levels, though the stock trades at a 30x P/E versus a 19x industry average.

All of this said, it’s worth noting that insider activity tells a nuanced story as CEO Joe Dominguez acquired 191,817 common shares on February 9, the largest executive buy signal. But on the same date, he also disposed of 176,097 shares at $272.15, suggesting tax or rebalancing activity rather than pure conviction.

With Q4 2025 results still pending and the Calpine integration just beginning, the next quarter will determine if sentiment stabilizes or slides further. Currently trading approximately $60 below its January starting price of $353, the stock’s path forward hinges on whether Constellation can convert its nuclear positioning into earnings growth.