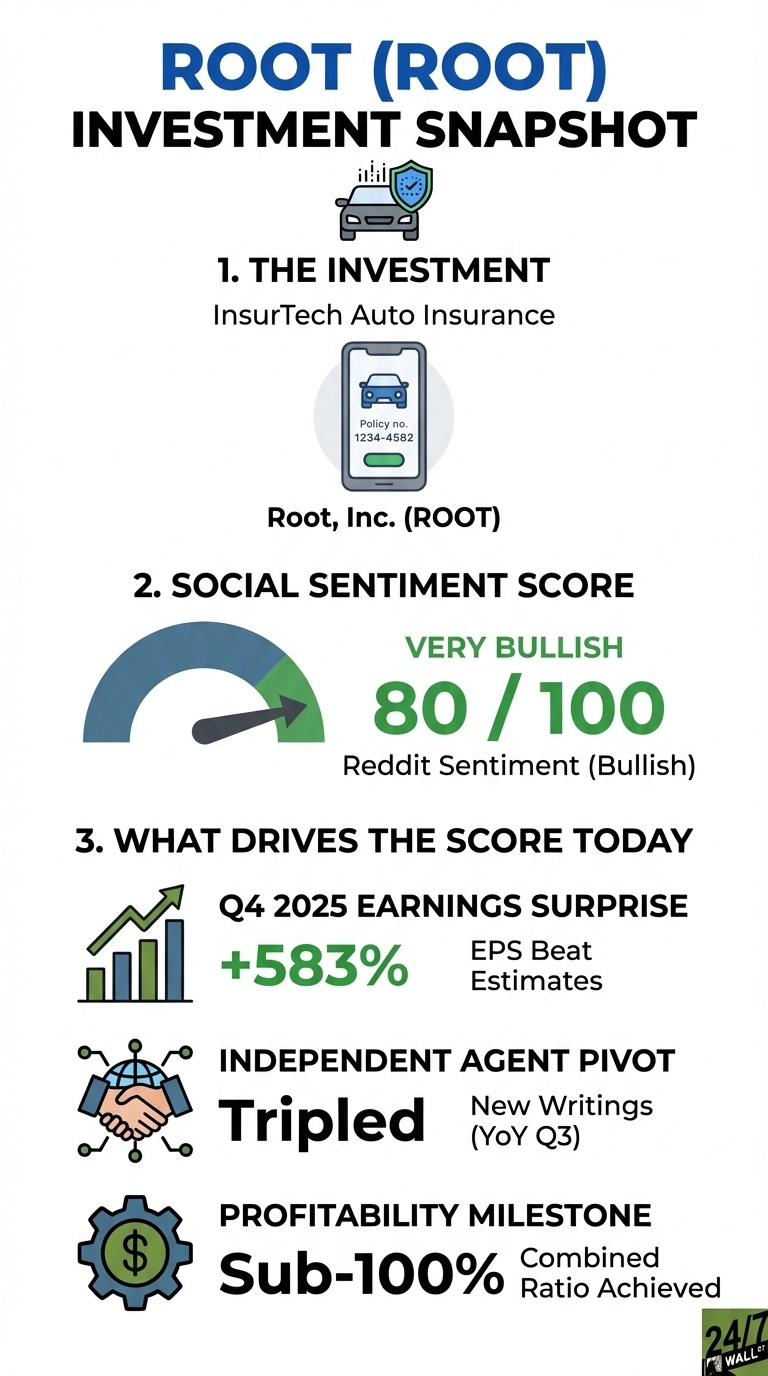

Calling itself a “disruptor” in the trillion-dollar insurance industry, Root, Inc. (NASDAQ:ROOT) stock is down 8.2% over the past week, and roughly 21% year-to-date, even as Reddit sentiment sits at 80 out of 100, firmly bullish. That disconnect tells the real story as investors who follow Root closely think the market is undervaluing a company that just crossed a genuine business milestone.

Showing itself (again) as a company to be watched in the space, Root posted full-year 2025 net income of $40.3 million, a 30% increase year-over-year on $1.5 billion in premiums. What’s more telling is how it got there as Root achieved a sub-100% combined ratio for the full year, meaning it is now profitable on underwriting alone. For an insurtech that spent years burning cash, that distinction matters.

The Independent Agent Channel Nobody Priced In

The February 25 earnings call made clear where growth is heading as the independent agent channel, which represents roughly one-third of the U.S. auto insurance market, is Root’s fastest-growing segment in a total addressable market management pegged above $100 billion. Independent agent new writings more than tripled year-over-year in Q3 2025, with momentum continuing into 2026. Root’s AI-driven pricing models delivered a 20%+ increase in estimated customer lifetime values over the past 12 months, sharpening its competitive pitch to agents.

WSB Noticed Before the Quarter Dropped

Reddit discussion is concentrated in r/wallstreetbets, where user DrSeuss1020 put $100k on the line before Q4 results, arguing:

ROOT $100k YOLO – EARNINGS TONIGHT 2/25

by u/DrSeuss1020 in wallstreetbets

“ROOT currently has a P/S ratio of .70 which is almost half the industry standard… ROOT is growing well, improving profitability and expanding partnerships… I believe they deserve a more fair re-rating back to the $100-150 range in due time.”

The post drew 82 comments and an 88% upvote ratio. The bull case rests on three points:

- Full-year 2025 net income of $40.3 million with a sub-100% combined ratio, crossing into genuine underwriting profitability for the first time

- Independent agent channel tripling new writings year-over-year in a $100 billion+ addressable market

- Roughly $600 million in cash against $200 million in debt, funding expansion to 36 states with all contiguous states targeted by end of 2027

Analysts Are Constructive, But 2026 Is a Prove-It Year

As it stands in late February, four analysts rate ROOT a Buy with zero Sell ratings, and a consensus price target of $108.40 implies roughly 87% upside. The catch is that management signaled planned investments and higher loss ratios will moderate 2026 net income. The Q4 beat was substantial, with $0.3935 reported versus an estimated loss of $0.0814, a 583% positive surprise, but that magnitude is unlikely to repeat. Whether independent agent policy counts keep scaling and whether the combined ratio holds below 100% as growth spending accelerates will determine if 2026 validates the bull case or exposes it.

Contact [email protected] for any questions or corrections.