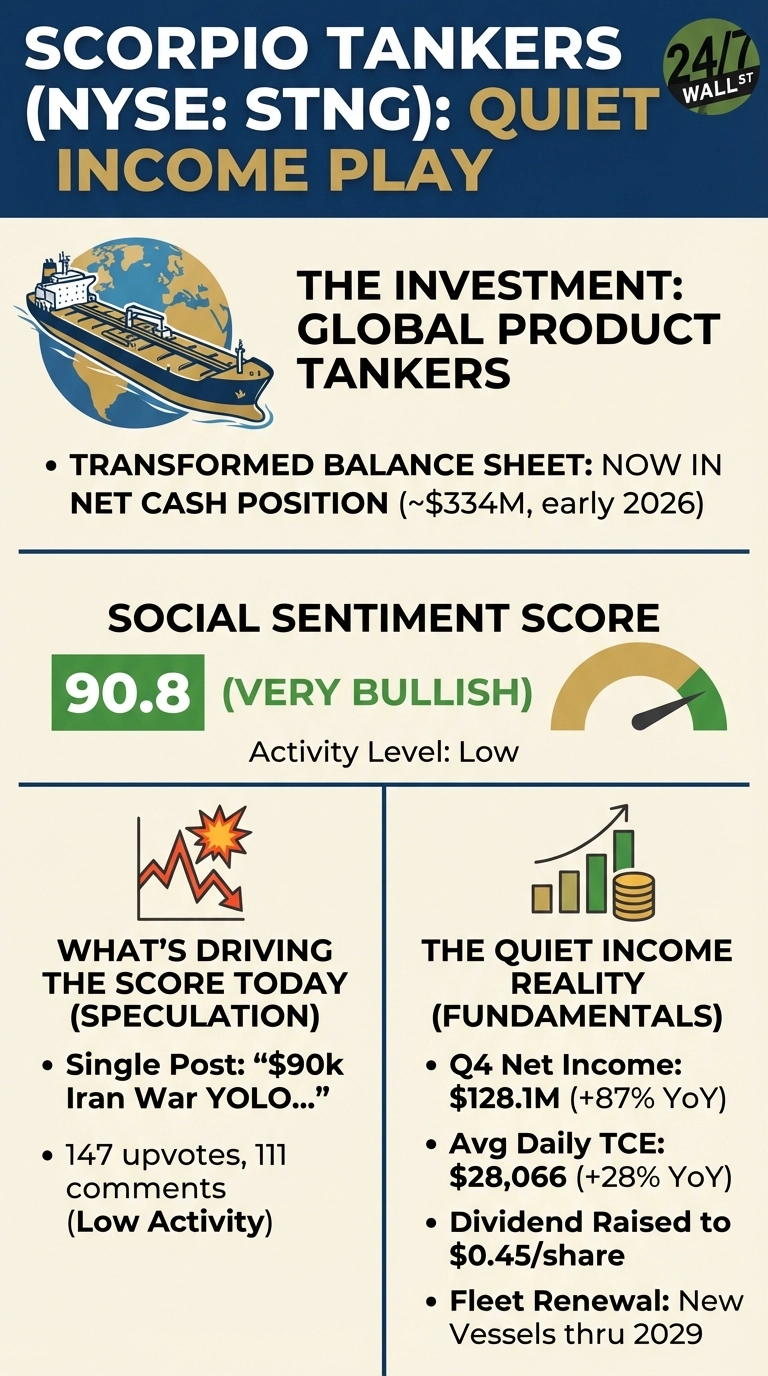

Engaging in the seaborne transportation of crude oil and petroleum worldwide, Scorpio Tankers (NYSE:STNG) has moved from $3.1 billion in net debt in 2021 to a net cash position of roughly $332 million as of early 2026. That shift changes what kind of stock this actually is. Reddit sentiment sits at 90.8 out of 100, firmly “very bullish.” The catch: that score is driven almost entirely by one speculative post, not a broad income thesis.

WSB Is Playing a War Trade. The Balance Sheet Tells a Different Story

User stealnova dropped $90,000 into STNG call options betting on an Iran conflict:

$90k Iran War YOLO Oil Tanker Calls

by u/stealnova in wallstreetbets

“I’m pretty sure $STNG calls are the absolute best hedge if a war with Iran happens… it could go to $250+”

That post drew 147 upvotes and 111 comments with “low” activity, meaning concentrated enthusiasm from a small cohort. The reasons serious investors watch STNG have nothing to do with war scenarios.

Scorpio’s Q4 Makes the Income Case Without Geopolitics

Q4 2025 results:

- Revenue of $252.65M, beating the $240.45M consensus

- Net income of $128.1M, up 87% from $68.6M a year earlier

- Average daily TCE rates of $28,066 versus $21,978 in Q4 2024, a 28% jump

For now, the company is looking at a cash position of around $937 million against total debt of $628 million. Management prepaid $154.6 million covering all scheduled amortization through December 2027, leaving near-term cash flows unencumbered by debt service.

The quarterly dividend rose to $0.45 per share, up from $0.42 last quarter, with the ex-dividend date set for March 6, 2026. The annualized payout runs $1.80 per share, roughly a 2.38% yield, backed by 10 newbuilding vessels delivering through 2029, all scrubber-fitted.

Analysts Are Aligned, but One Risk Deserves Attention

One of the key points here is that five of six analysts rate STNG a strong buy, with a 12-month price target of $79.0, compared with a current price near $75. To get there, the focus will be on things like the company’s LR2 tankers, which are fixing above $50,000 per day on key routes, and on structural ton-mile demand, which has grown roughly 20% since 2019 as refinery relocations force longer voyages. The variable worth tracking is the proposed US and China port fee regimes, which could affect certain vessels in Scorpio’s fleet. That’s the real risk, not oil price speculation.