Yesterday, the market was watching to see whether TeraWulf‘s (NASDAQ: WULF) accelerating HPC pivot would offset continued pressure on its bitcoin mining segment. The short answer: The infrastructure story is winning, even if the quarterly revenue number disappointed. Shares closed at $17.88 on Feb. 26, and WULF has gained +55.6% year to date, signaling that investors are pricing the asset base, not the income statement.

The Headline Miss Masks a Bigger Story

But the number that mattered most heading into the print was HPC lease revenue, and it delivered. Q4 HPC lease revenue hit $9.70 million, up 35% sequentially. Full-year 2025 revenue reached $168.46 million, up 20% year over year. The massive reported net loss of $661.42 million is largely an accounting artifact. A $429.79 million non-cash charge from changes in fair value of warrants and derivatives drove the bulk of that figure. It does not reflect operational performance.

A key operational metric from the quarter: $12.80 billion in total contracted long-term revenue across 522 contracted critical IT megawatts, with Google credit enhancement backing key leases.

Management Holds the Bullish Line

CEO Paul Prager framed the setup confidently on the earnings call. “We enter 2026 with 522 critical IT MW of contracted HPC capacity and a gross 2.9-GW multi-regional platform designed for long-term expansion,” he said. The tone was consistent with what we flagged heading into the print: this is a company in aggressive build mode, not consolidation mode.

Capacity delivery milestones are stacked throughout 2026, with CB-2B due in Q1, CB-3 in May, CB-4 in Q3, and CB-5 in Q4. Design optimizations on CB-4 and CB-5 added an estimated $200 million in incremental lease revenue to the financial plan without increasing base construction budgets.

What to Watch Through Mid-2026

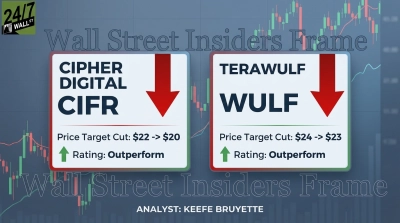

The revenue miss will likely prompt some analyst model adjustments, but the consensus remains firmly positive. All 12 covering analysts rate WULF a buy or strong buy, with a consensus price target of $23.56. Execution on the CB-3 and CB-4 delivery schedule is now the primary catalyst. Any slippage there, or further deterioration in bitcoin prices compressing mining margins, would be the key risk to monitor in the quarters ahead.

Contact [email protected] for any questions or corrections.