TeraWulf (NASDAQ:WULF) stock is up 13.5% in today’s session. Also, Cipher Digital (NASDAQ:CIFR) stock is rallying 7% while Coinbase Global (NASDAQ:COIN | COIN Price Prediction) shares are up 4.6%. These are three different layers of the crypto infrastructure stack, all moving together on the same macro tailwind.

The common thread is Bitcoin’s weekly momentum. Bitcoin has gained roughly 6% over the past week, climbing from around $68,432 to approximately $72,521.

Institutional ETF inflows, geopolitical tensions including the Iran war, and rising oil prices pushing investors toward alternative assets have all contributed to the move. When Bitcoin runs, the equities that live closest to it tend to amplify the trade.

TeraWulf: The AI Pivot Gets Its Moment

TeraWulf’s 12% gain today is partly a rebound from the punishment the stock took after its Q4 2025 earnings report. Revenue came in at $35.8 million, missing the $42.96 million consensus by about 17%. The stock fell roughly 15% in the aftermath, and WULF was still down about 8.5% over the past month heading into today.

Yet, the earnings miss obscured a more important transition happening underneath. TeraWulf’s HPC lease revenue grew 35% quarter-over-quarter to $9.7 million in Q4 2025, even as the company’s Bitcoin mining revenue collapsed from the prior quarter.

In 2026, TeraWulf is no longer primarily a miner. It’s building AI and HPC data center infrastructure, and the contracts to prove it are piling up.

The company has secured over $12.8 billion in long-term customer contracts and $6.5 billion in financing. Google provided a $3.2 billion credit backstop and took an equity stake, supporting the pivot to AI and HPC infrastructure. CEO Paul Prager framed the scale of what is being built: “We enter 2026 with 522 critical IT MW of contracted HPC capacity and a gross 2.9-GW multi-regional platform designed for long-term expansion.”

Analyst sentiment remains constructive. Morgan Stanley carries an Overweight rating on WULF stock with a $37 price target; Keefe Bruyette & Woods rates it Outperform with a $23 target.

Furthermore, the consensus sits at Moderate Buy with an average target of $20.62. Director Michael Bucella has been reinforcing that view with his own money, making five consecutive open-market share purchases between March 4 and March 11, 2026.

Cipher Digital: The Execution Year Begins

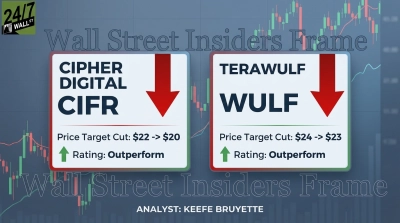

Cipher Digital’s 6% gain today comes after a rough stretch. The stock is down about 13.5% over the past month, weighed down by a Q4 earnings miss and subsequent analyst price target cuts. If you want the full context on those cuts, Wall Street’s March 11 reaction is worth reading. The stock has recovered some ground after the post-earnings decline.

The rebrand from Cipher Mining to Cipher Digital isn’t cosmetic. The company has approximately $9.3 billion in contracted HPC revenue across two landmark leases: a 15-year, 300 MW deal with Amazon Web Services and a 10-year, 300 MW deal with Fluidstack and Google, with both data centers targeting October 2026 energization. Expected average annualized NOI from those contracts is approximately $669 million.

Cipher Digital CEO Tyler Page set the tone for the year ahead:

“2026 is a year of execution for Cipher as we fully transition the business into a leading infrastructure platform. With construction on track at our existing projects, a deep and expanding development pipeline, and heightened demand from both capital providers and tenants, we are firmly focused on establishing Cipher Digital as the premier developer and operator of data centers powering the next generation of compute.”

Moreover, Soros Fund Management increased its Cipher Digital stake by 67.5% to 1.3 million shares, a signal that sophisticated capital sees value in the transformation story.

Canaccord Genuity carries a Buy rating with a $27 price target on CIFR stock, and the consensus sits at Moderate Buy with an average target of $24.73.

The bear case is real, though. Cipher Digital’s total liabilities have expanded to $3.46 billion from $173 million year-over-year as bond financings funded construction. Execution on large-scale data center builds with a small number of hyperscale tenants leaves little margin for error.

Coinbase: The Exchange Layer Catches the Bid

Coinbase’s 4% move today is the most straightforward of the three. When Bitcoin climbs, trading volumes rise, and Coinbase collects fees on every transaction. The company is the largest U.S. cryptocurrency exchange and benefits directly from rising Bitcoin prices and increased trading volumes.

Coinbase stock is up about 27.6% over the past month, so today’s move is building on genuine momentum rather than a bounce from weakness. The company’s full-year 2025 revenue came in at $7.2 billion, with total crypto trading volume of $5.2 trillion, up 156% year-over-year. Plus, Coinbase’s board approved a $2 billion share repurchase program, with $2.3 billion remaining as of February 10.

Coinbase CEO Brian Armstrong has been clear about where the company is positioning: “As regulatory clarity emerges, we believe crypto will update all financial services.” Reddit sentiment on COIN stock has stayed consistently bullish all week, with sentiment scores ranging from 72 to 78, suggesting retail conviction has not faded even after the recent run.

The Bigger Picture

What today’s move illustrates is that the crypto infrastructure trade is no longer a single-variable bet on Bitcoin’s price. TeraWulf and Cipher Digital are now AI and HPC data center companies that happen to have Bitcoin mining heritage.

As for Coinbase, it’s hard to argue with a 156% year-over-year gain in total crypto trading volume. Going forward, expect a persistent association between the prices of Bitcoin and COIN stock.

All three stocks represent different parts of the same infrastructure stack: compute (WULF, CIFR) and exchange (COIN). Bitcoin’s weekly momentum and institutional accumulation activity remain key factors for the crypto infrastructure sector heading into the back half of March.

Contact [email protected] for any questions or corrections.