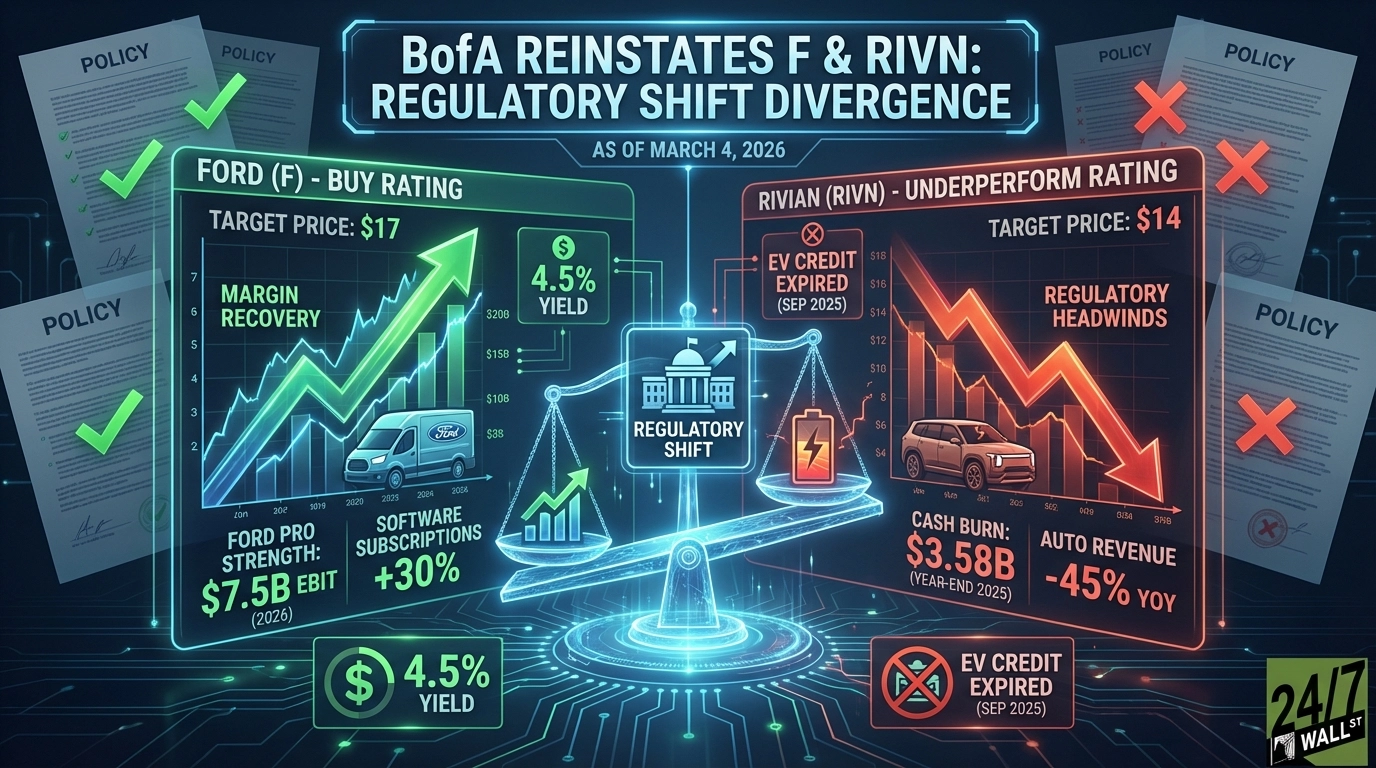

Bank of America just put its name behind two of the most polarizing auto stocks on the market, and the signals point in opposite directions. BofA reinstated Ford (NYSE: F) | F Price Prediction with a Buy rating and a $17 price target, while slapping Rivian (Nasdaq:RIVN) with an Underperform and a $14 price target. The regulatory shift reshaping the auto landscape is the dividing line between these two calls.

Three Data Points That Define the Divergence

First, the street consensus on Ford is cautious but BofA is leaning bullish. The broader analyst community has 16 Hold ratings, 3 Strong Buys, and 1 Buy, with a consensus target of $13.99. BofA’s $17 target sits well above that crowd, reflecting a more aggressive view on Ford’s margin recovery. Ford trades at $13.04 today, meaning BofA sees roughly 30% upside from here.

Second, the Ford thesis rests on a real earnings engine. Ford Pro, the commercial vehicle segment, is guiding for $6.5 billion to $7.5 billion in EBIT for 2026, and paid software subscriptions in that segment grew 30% in 2025. Ford Credit delivered a 55% YoY jump in full-year EBT to $2.6 billion. These are not speculative numbers. BofA expects Ford to progress from a 4.8% EBIT margin in 2026 toward its stated 8% adjusted EBIT margin target by 2029. CEO Jim Farley framed it plainly on the earnings call:

“Moving forward, we’ll continue building on our strong foundation to achieve our target of 8% adjusted EBIT margin by 2029.”

Jim Farley, Ford CEO

Third, on Rivian, BofA’s $14 Underperform target is notably below where the stock trades today at $15.105, and it’s even more bearish than you’d expect given that the broader analyst consensus carries a $18 target with 7 Buy ratings and 10 Holds. BofA is the outlier on the bear side, and the data gives them cover. Rivian’s Q4 automotive revenue collapsed 45% YoY, driven by a $270 million collapse in regulatory credit sales and softer R1 deliveries after the federal EV tax credit expired on September 30, 2025. Cash burned to $3.58 billion at year-end, down 32.4% YoY.

The Gap Between Wall Street and Where These Stocks Trade

Ford is down 9.67% over the past week despite the BofA reinstatement, a signal that the market is not yet buying the margin recovery story. With Ford’s 52-week high at $14.80 and the stock sitting below its 50-day moving average of $13.73, there’s a clear gap between analyst optimism and current price action. The bull case requires Model e losses to abate, tariff headwinds to stabilize, and Ford Pro to keep compounding. That’s three things that all need to go right.

Rivian’s gap is different. The stock is down 23.31% year-to-date and trades below its 50-day moving average of $17.12. The R2 launch targeting Q2 2026 customer deliveries at a base price of roughly $45,000 is the next real catalyst, but BofA’s view is that the regulatory environment makes near-term profit improvement unlikely regardless of execution.

The Takeaway

BofA is right to split these calls. Ford is a restructuring story with a profitable commercial core, a dividend yielding roughly 4.5%, and a management team that is cutting EV losses rather than doubling down. You buy Ford if you believe the regulatory tailwind for trucks and SUVs is durable and that Ford Pro’s software flywheel keeps spinning. Rivian is a different bet entirely: a high-conviction growth trade on R2 execution and VW partnership revenue that requires patience, capital, and tolerance for a stock that has lost nearly 85% from its IPO highs. BofA’s Underperform on RIVN is not a call that the company fails. It’s a call that the stock is priced for a recovery that the regulatory backdrop will not deliver on schedule.

Contact [email protected] for any questions or corrections.