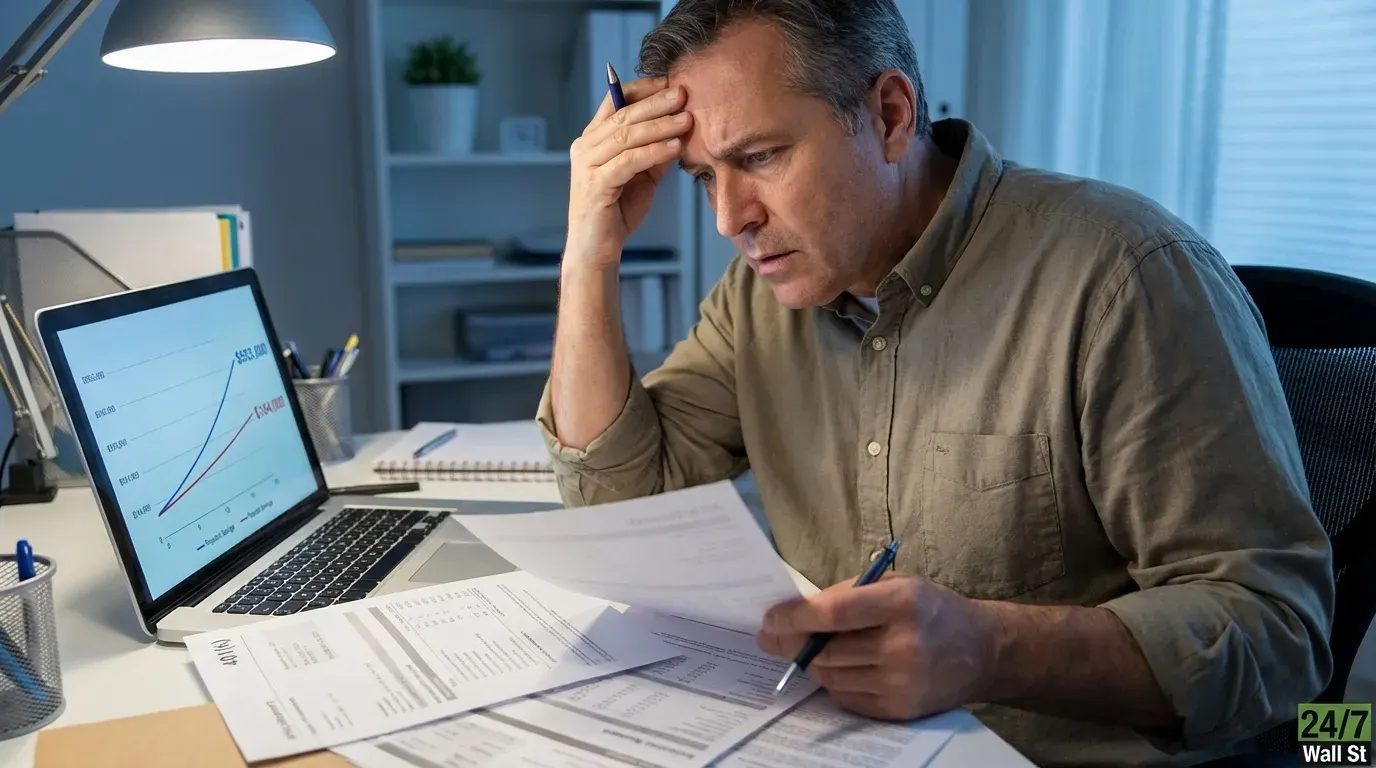

A worker earning $65,000 and auto-enrolled at 3% will contribute $1,950 per year. Left untouched, that contribution rate delivers roughly $184,000 by retirement. Double the rate to 6% and capture the full employer match, and the same person accumulates closer to $553,000. The gap exceeds $350,000, and it stems not from market timing or stock picks but from a single checkbox in an account portal that most participants never revisit.

Why the 3% Default Stuck

Plan sponsors deliberately chose 3% when designing auto-enrollment programs. The logic was straightforward: a low default minimizes opt-outs from employees worried about smaller paychecks. Three percent felt painless enough to keep workers from abandoning the plan entirely. Decades of behavioral research have since confirmed that inertia keeps the majority of auto-enrolled participants at whatever rate they were defaulted into, sometimes for their entire tenure with an employer.

The most common employer matching formula is a 50% match on contributions up to 6% of salary, according to data from Fidelity and industry surveys. At a $65,000 salary, contributing only 3% forfeits half the available employer match, roughly $975 each year. Over a 30-year career, that uncollected match compounds into tens of thousands of dollars in lost wealth. Employer matching contributions reached a record average of 4.7% in 2025 according to Vanguard’s “How America Saves 2026” report, making the missed match more costly than ever for workers stuck at low default rates.

The broader picture is one of progress laced with persistent gaps. Fidelity reports that the average total retirement savings rate, combining employee deferrals and employer contributions, held at 14.2% for the third consecutive year. Vanguard’s data tells a similar story: its average employee contribution rate reached 7.6% in 2025, and when employer contributions are included, the average total participation rate climbed to a record 12.1%, up from 11.6% four years earlier. Yet hardship withdrawals climbed to 6% of participants in 2025, up from 5% in 2024 and well above the pre-pandemic average of roughly 2%. That uptick reflects both easier access to hardship provisions under SECURE 2.0 and genuine financial pressure among lower-income workers, marking the sixth consecutive annual increase since 2018.

The Auto-Escalation Feature Most Plans Offer but Few Workers Activate

Most plans include automatic contribution escalation alongside auto-enrollment. The feature increases a participant’s deferral rate by 1% per year until hitting a cap, typically 10% or 15%. According to Vanguard’s “How America Saves 2026” report, 71% of plans with auto-enrollment included an automatic escalation feature. Despite that broad availability, only 31% of participants actually had their deferral rate increased via auto-escalation over the prior year.

A 35-year-old starting at 3% and escalating by 1% annually reaches a 6% contribution rate within three years and climbs to 8% or higher by mid-career. The compounding effect of those early rate increases, applied over three decades, produces the $200,000-plus gap referenced in this article’s title. The damage comes not from a single bad market year but from years of under-contribution during the period when compounding does its heaviest lifting.

Vanguard’s 2026 data also provides encouraging context. Average participant account balances rose 13% in 2025 to a record $167,970, with a median balance of $44,115 representing a 16% year-over-year gain. Overall plan participation climbed from 65% to a record 86% among eligible employees as auto-enrollment spread. Even so, 62% of plans with auto-enrollment defaulted employees at a contribution rate of at least 4% as of year-end 2025. That still leaves a meaningful employer match gap for workers whose plans match up to 6%, since a 4% default forfeits a portion of the available match under most common matching structures.

SECURE 2.0 Changed the Rules for New Plans Only

The SECURE 2.0 Act requires new 401(k) plans established after December 29, 2022 to auto-enroll eligible employees at a minimum of 3% and escalate automatically by at least 1% per year until reaching at least 10%. This mandate applies only to new plans. If your employer’s plan predates that cutoff, the old defaults still apply, and the escalation feature may be sitting dormant in your account settings.

SECURE 2.0 also introduced a “Super Catch-Up” window for workers between the ages of 60 and 63. The standard employee deferral limit for 2026 sits at $24,500, confirmed by the IRS, and the standard age-50-plus catch-up allows an additional $8,000. Workers in the 60 to 63 age bracket can substitute a higher catch-up contribution of $11,250 instead of the standard $8,000 limit.

High earners face strict new rules beginning this year. If a worker’s prior-year FICA wages (reported in Box 3 of Form W-2) exceeded $150,000 for 2025, any age-based catch-up contributions in 2026 must be made on a Roth (after-tax) basis. If a plan has not added the necessary Roth infrastructure, high earners in those plans will be unable to make any catch-up contributions until a Roth option becomes available. The $150,000 threshold is indexed for inflation.

Consumer sentiment data from the University of Michigan shows that anxiety about household finances, while improving, remains well below historical norms. The index closed June 2026 at a final reading of 49.5, rebounding from May’s all-time low of 44.8. The preliminary July 2026 reading then climbed further to 54.4, the highest level since February, as easing gasoline prices provided some relief. Even so, sentiment sits 12% below where it stood a year ago, and elevated prices continued to draw spontaneous complaints from a majority of survey respondents. That persistent financial stress is exactly the environment where auto-enrollment defaults do the most long-term damage, pushing workers to avoid account portals rather than engage with them.

Two Actions That Take Less Than Two Minutes

The fix requires checking account settings, not elaborate planning.

- Check your current deferral rate. Navigate to your 401(k) plan portal contribution settings and confirm your contribution percentage. Those contributing only 3% when their employer matches up to 6% are forfeiting free money every pay period. Raising to 6% on a $65,000 salary costs roughly $1,950 more per year out of pocket but captures an equal amount in employer contributions previously left behind.

- Review the auto-escalation feature. It is usually labeled “automatic increase” or “contribution escalation” in the same settings screen. Setting it to increase by 1% per year meaningfully closes the gap over time. A 1% raise on a $65,000 salary amounts to $650 annually. Most people never notice it on their paychecks.

Tax Mitigation and Medicare Surcharge Protection

Reviewing internal plan settings serves a dual purpose for households approaching higher income thresholds. Maximizing pre-tax contributions reduces Modified Adjusted Gross Income (MAGI), which matters directly for future Income-Related Monthly Adjustment Amount (IRMAA) surcharges. Medicare assesses Part B and Part D premium surcharges based on a two-year tax look-back window, so suppressing current MAGI through maximum workplace plan contributions can prevent significantly higher healthcare costs in retirement. This strategy is worth coordinating with a fee-only financial advisor, but the first step is simply logging in to audit your default settings.

Editor’s note: This article has been updated to reflect the preliminary University of Michigan Consumer Sentiment reading for July 2026, which came in at 54.4 — the highest level since February — up from the June final reading of 49.5 cited in the prior version, with sentiment now running 12% below year-ago levels rather than the nearly 20% gap cited earlier. Vanguard’s median account balance of $44,115 and the average employee contribution rate of 7.6% for 2025, both from the full “How America Saves 2026” report, have also been added for additional context.

Contact [email protected] for any questions or corrections.