Micron Technology (NASDAQ:MU | MU Price Prediction) and Western Digital (NASDAQ:WDC) have spent a decade riding one of the most volatile cycles in technology. Both sit at the intersection of memory and storage, and both have been rewired by the AI buildout. The returns reflect it.

Two Very Different Paths

Micron spent years trapped in the boom-bust rhythm of DRAM and NAND pricing. When memory oversupply hit, earnings collapsed; when demand recovered, they exploded. AI changed the ceiling. High-bandwidth memory became critical infrastructure for AI accelerators, and Micron is the only U.S.-based manufacturer of it. Cloud Memory revenue nearly doubled to $5.28B in Q1 FY26, with gross margins of 56%. That is a structurally different business than five years ago.

Western Digital’s story is messier. It straddled hard disk drives and flash storage for years, then completed the spinoff of its Sandisk flash division on February 21, 2025. What remains is a pure-play HDD company with cloud revenue representing 87% of its mix, driven by hyperscaler demand for high-capacity drives in AI data centers. Gross margins expanded from around 30% to 46.1% in Q2 FY26.

The Numbers

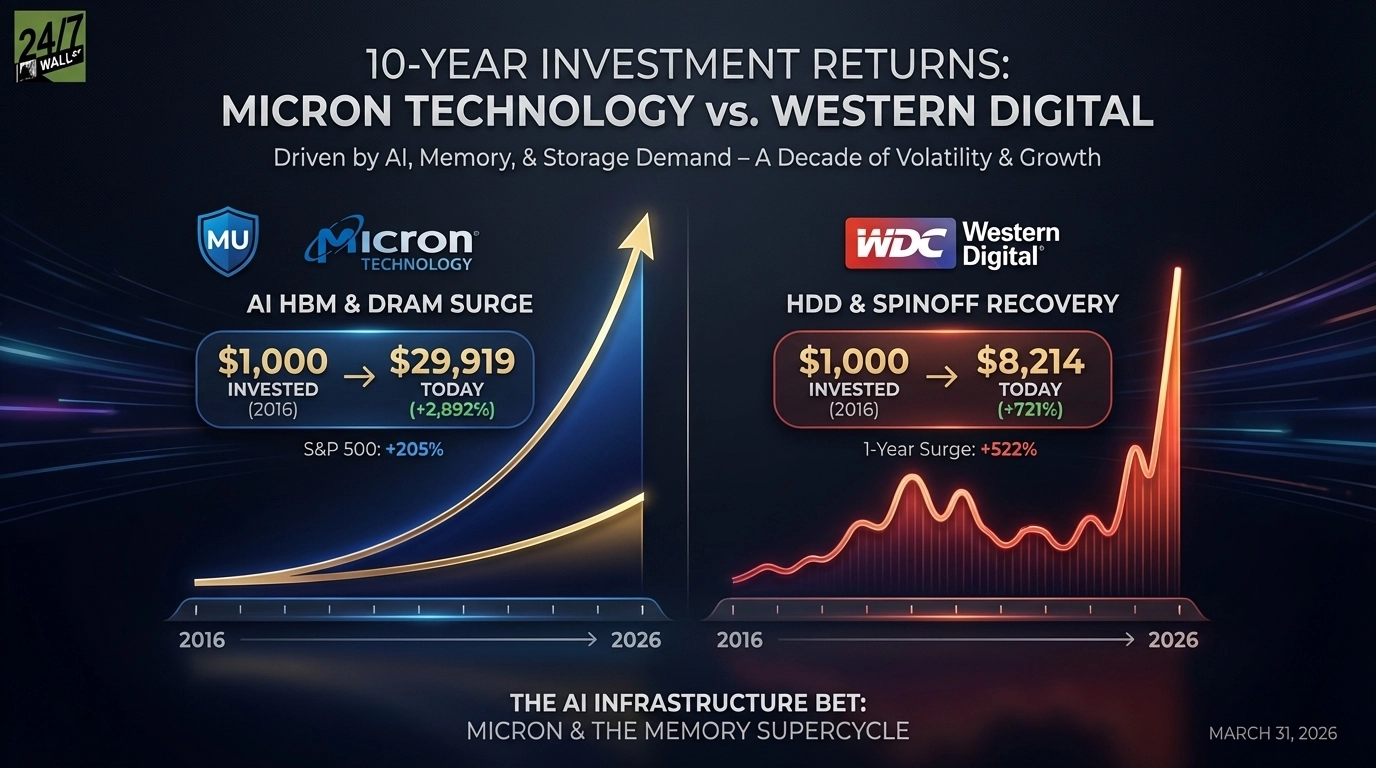

Micron’s 10-year number is extraordinary. A $1,000 investment at $10.76 per share in April 2016 would be worth roughly $29,919 today, nearly 10x the S&P 500’s return over the same window, though the ride required holding through brutal drawdowns including a near-halving during the 2022 memory glut. Western Digital’s one-year surge of 522% is the standout short-term number, driven almost entirely by the Sandisk separation and AI demand lifting HDD valuations.

Micron Is the Cleaner Bet

Micron’s investment case rests on whether the AI infrastructure buildout continues compounding demand for HBM and data center DRAM. Analysts carry a consensus target of $527.60 against a current price of $329.89, and the forward P/E sits at roughly 8x, cheap for a company posting this kind of revenue growth. Micron is the only domestic HBM producer, and that matters geopolitically. The risk is memory pricing, which has turned before and will again. The stock can cut in half before most investors react.

Western Digital is more conditional. The thesis holds if margin expansion toward 47-48% guidance continues and cloud HDD pricing stays firm, but the forward P/E of roughly 27x prices in significant execution. The Sandisk spinoff reset the story and the dividend, which was cut from $0.50 quarterly to $0.10 before recovering to $0.125. That capital allocation history warrants caution. Micron is the cleaner bet on AI memory infrastructure at a more reasonable valuation.

Contact [email protected] for any questions or corrections.