Micron Technology (NASDAQ:MU | MU Price Prediction) presents a compelling bull case at $420.52. Fundamentally, the argument for owning it has rarely been cleaner for a semiconductor name of this scale. With AI-driven memory demand accelerating and earnings growing at a pace that makes the current valuation look genuinely cheap, the stock deserves serious attention from investors who can tolerate volatility.

Micron is the only U.S.-based manufacturer of DRAM and NAND flash memory, giving it a structural position in the AI infrastructure buildout that no domestic competitor can replicate. It is also well-positioned amid the ongoing memory chip shortage.

The company has moved aggressively into high-bandwidth memory, the specialized chip architecture that powers AI accelerators, with order books stretching into 2027. Revenue has climbed from $8.05 billion in Q2 FY2025 to a guided $18.70 billion in Q2 FY2026, reflecting a genuine demand supercycle rather than a one-quarter anomaly.

The Bull Case: A Supercycle With a Cheap Forward Multiple

The stock trades at a trailing P/E of 20x, modest for a high-growth semiconductor company. The forward P/E drops to just 7x, implying the market is either deeply skeptical of earnings durability or dramatically underpricing a sustained upcycle. The PEG ratio of 0.245 reinforces this: growth is not priced in.

Q1 FY2026 delivered record revenue of $13.64 billion, beating estimates by nearly 6%, alongside non-GAAP EPS of $4.78 against an estimate of $3.94. Q2 guidance called for revenue of $18.70 billion and non-GAAP EPS of $8.42. CEO Sanjay Mehrotra stated: “Our Q2 outlook reflects substantial records across revenue, gross margin, EPS and free cash flow, and we anticipate our business performance to continue strengthening through fiscal 2026.”

The Bear Case: A Stock That Has Already Run Hard

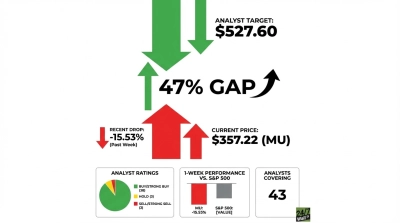

Micron is up 47% year to date and has risen more than 500% over the past year. That kind of move compresses future returns and raises the stakes if anything disappoints. Memory is a notoriously cyclical industry, and the current upcycle is well-known, meaning much of the good news may already be reflected in the price.

Insider activity has been net selling across 36 recent transactions. The stock carries a beta of 1.61, making it significantly more volatile than the broader market. Any sign of demand softening, inventory buildup, or macro deterioration could produce sharp drawdowns. Tariff and trade policy exposure adds unpredictability for a company that manufactures and sells globally.

The Hold Argument: Waiting for Confirmation on Q2 Delivery

Investors who prefer to see guidance confirmed before adding exposure have a reasonable case. Q2 FY2026 earnings are expected around mid-June, roughly 65 days out. If Micron delivers the $18.70 billion in revenue and $8.42 in EPS it has projected, the forward multiple compresses further and the bull case strengthens materially. Waiting for that confirmation costs some upside but eliminates the binary risk of a guidance miss.

What the Numbers Actually Say

Micron trades at $420.52, against a consensus analyst target of $526.48, implying meaningful upside. Of 43 analysts covering the stock, 38 rate it Buy or Strong Buy, 5 rate it Hold, and none rate it Sell. A unanimous absence of Sell ratings across a 43-analyst panel is notable. Year to date, Micron has risen 47%, substantially outperforming the S&P 500. The stock sits roughly 11% below its 52-week high of $471.14, having pulled back from that peak before recovering.

At $420, the Forward Multiple Presents a Compelling Case

A forward P/E of 7x on a company growing revenue at this pace is the kind of setup that long-term investors rarely encounter in large-cap technology. The AI memory supercycle is real, HBM demand is structural, and Micron’s position as the sole U.S.-based manufacturer gives it a geopolitical tailwind that peers cannot match. If Q2 guidance is delivered, the stock would likely move meaningfully toward the analyst consensus target.

The primary risk is cyclicality. If AI infrastructure spending decelerates or inventory builds faster than expected, earnings could disappoint sharply. Watch Q2 FY2026 results closely, particularly gross margin delivery against the guided 68% non-GAAP target and any change in management’s tone around second-half demand.

At this price, the risk-reward profile is defined by a forward multiple of 7x, 88% analyst bullish consensus, and a revenue trajectory that has grown from roughly $8 billion to a guided $18.70 billion over six quarters — all grounded in numbers that have consistently beaten expectations.

Contact [email protected] for any questions or corrections.