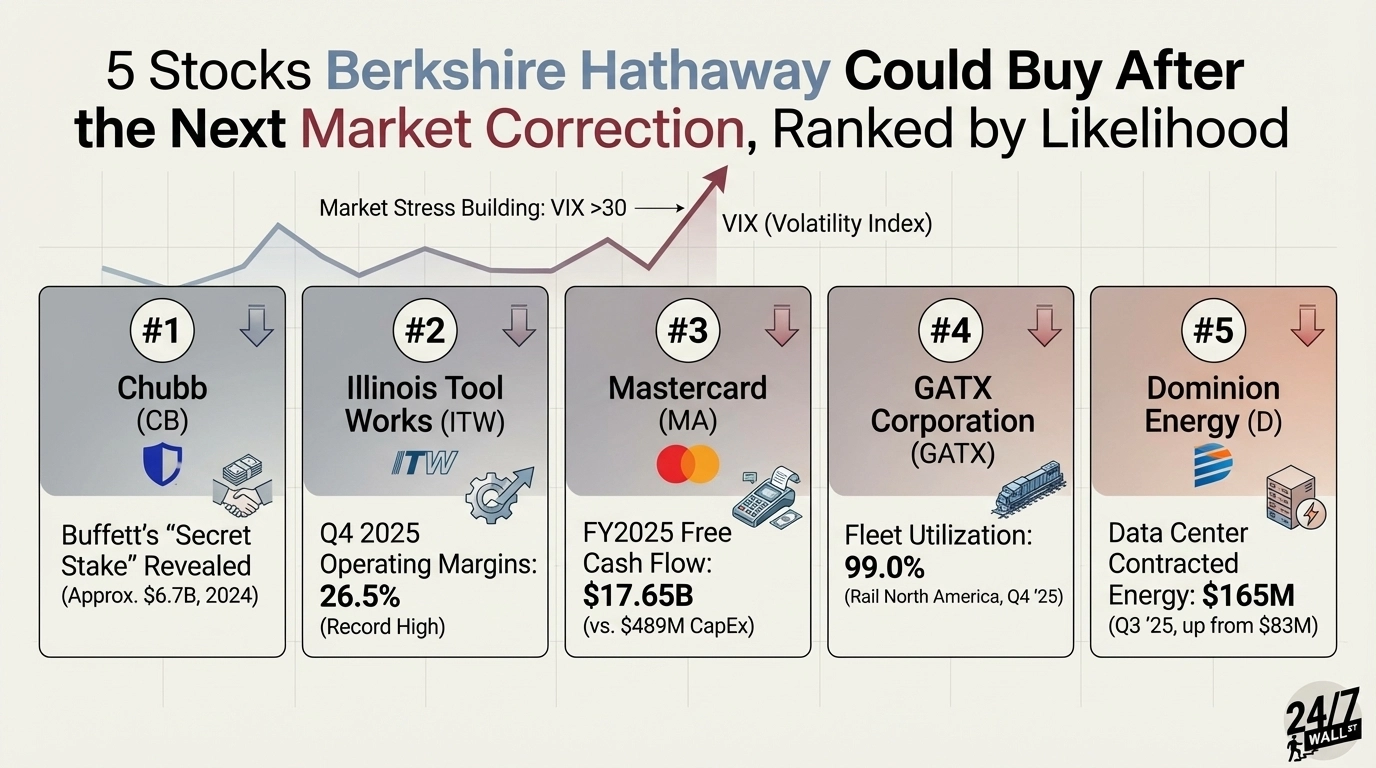

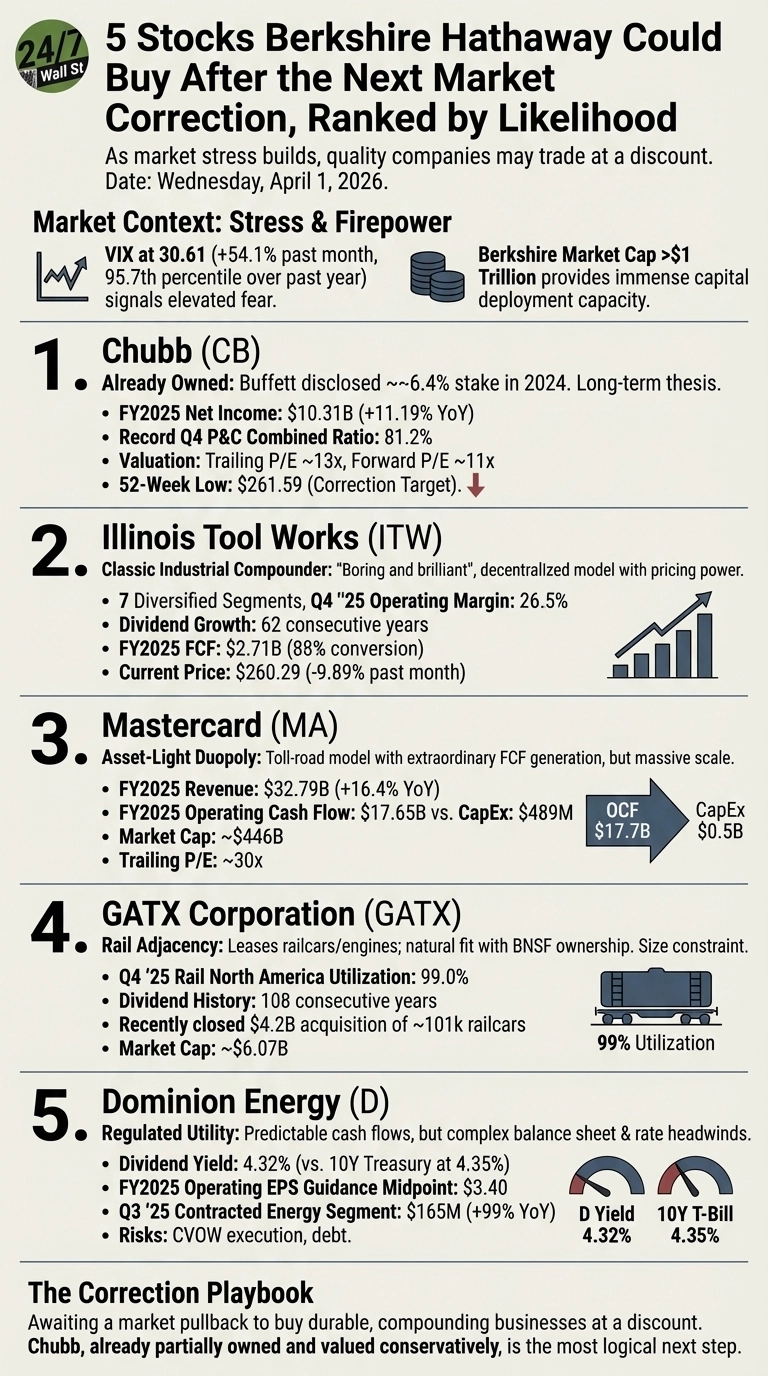

With the Cboe Volatility Index (VIX) recently at 30.61 and up 27.7% over the past six weeks, market stress is building in ways Berkshire Hathaway (NYSE: BRK-B | BRK-B Price Prediction) watchers should note. When fear spikes, Warren Buffett deployed capital. Berkshire’s market cap stands at over $1 trillion, giving it firepower to move decisively when quality companies trade at discounted prices. The five stocks below carry the hallmarks Berkshire prizes: durable moats, predictable cash flows, pricing power, and long records of rewarding shareholders. They are ranked from least to most likely to land in Berkshire’s portfolio after the next meaningful correction.

5. Dominion Energy

Dominion Energy (NYSE: D) operates regulated electric and gas utilities across Virginia, North Carolina, and South Carolina. Berkshire already purchased Dominion’s pipeline assets in 2020, demonstrating prior appetite for this business. The regulated model delivers predictable cash flows, though the 10-year Treasury at 4.35% makes Dominion’s 4.1% dividend yield less compelling than in a lower-rate environment.

The data center buildout in Northern Virginia provides a genuine growth tailwind, with the Contracted Energy segment delivering $165 million in Q3 2025 versus $83 million in the prior year. However, only 15% of analysts rate the stock bullish, the Coastal Virginia Offshore Wind project carries execution risk, and balance sheet complexity reduces the fit versus simpler Berkshire targets. A sharp correction would need to compress valuation meaningfully before the risk-reward ranks higher.

4. GATX

GATX (NYSE: GATX) leases railcars and engines, generating predictable, long-duration cash flows from hard assets. Berkshire’s ownership of BNSF railroad gives it direct industry knowledge, making GATX a natural adjacency. The business is executing well: Q4 2025 fleet utilization reached 99.0% in Rail North America, and GATX closed a $4.2 billion acquisition of roughly 101,000 railcars from Wells Fargo in January 2026.

The company has paid dividends for 108 consecutive years and recently joined the S&P 400 Dividend Aristocrats. All four covering analysts rate it a Buy, with a consensus target of $215.50. The constraint is size: at a $6.1 billion market cap, GATX barely registers for a company of Berkshire’s scale. A post-correction discount could change that calculus, but the deal would need creative structuring to matter.

3. Mastercard

Mastercard (NYSE: MA) operates one of the world’s two dominant payment networks, an asset-light toll road collecting fees on every transaction crossing its rails. Berkshire already holds Visa, so the payment network model is well understood in Omaha.

Mastercard’s financials are exceptional: FY2025 revenue reached $32.79 billion, up 16.42% year over year, with operating cash flow of $17.65 billion against capex of only $489 million. Q4 2025 adjusted EPS came in at $4.76 versus a $4.24 estimate. At a $445.9 billion market cap and a trailing PE of 30x, a full acquisition would be unprecedented in Berkshire’s history. A significant market correction could open the door to a much larger equity stake. Currently, 33 of 38 analysts currently rate it Buy or Strong Buy.

2. Illinois Tool Works

Illinois Tool Works (NYSE: ITW) is the kind of “boring and brilliant” compounder Berkshire has historically favored. Across seven diversified industrial segments, ITW generates operating margins of 26.5% in Q4 2025 and has grown its dividend for 62 consecutive years. FY2025 free cash flow reached $2.71 billion at 88% conversion, and management guided for FY2026 EPS of $11.00 to $11.40 with buybacks of roughly $1.5 billion planned.

The stock trades at $260.29, down 9.9% over the past month, already showing correction pressure. A deeper pullback toward the 52-week low of $214.66 would bring valuation into a range that makes a Berkshire move genuinely plausible. The decentralized operating model and pricing power across niche industrial markets are textbook Buffett criteria.

1. Chubb

Chubb (NYSE: CB) sits at the top for one overriding reason: Buffett already took a secret stake of approximately $6.7 billion, revealed in 2024. Berkshire builds positions like that only with a longer-term thesis. Chubb is the world’s largest publicly traded property and casualty insurer, generating FY2025 net income of $10.31 billion, up 11.19% year over year, with a record property and casualty combined ratio of 81.2% in Q4. Operating cash flow for FY2025 was $12.82 billion.

CEO Evan Greenberg has described the outlook plainly: “anticipate an excellent 2026 with strong growth in operating earnings and double-digit growth in EPS and tangible book value.” The stock trades at a trailing PE of just 13x with a forward PE of 11x, cheap for a franchise of this quality. A correction pulling Chubb back toward its 52-week low of $264.10 would almost certainly accelerate Berkshire’s buying.

The Correction Playbook

Each company offers a different version of what Berkshire values most: durable competitive advantages, honest management, and reliably compounding cash flows. Dominion and GATX offer regulated or contracted cash flows but carry constraints in size or complexity. Mastercard and Illinois Tool Works are premium compounders where valuation is the primary barrier. Chubb, already partially owned and trading at a modest multiple for its quality, is the most logical next step. The VIX at its 95.7th percentile over the past year suggests the correction that creates these opportunities may arrive sooner than many investors expect.