CrowdStrike Holdings (NASDAQ:CRWD) currently trades at $426.51, while the Wall Street consensus price target sits at $489.86, a gap of roughly 14.85%. That is a meaningful dislocation for a company that just delivered its strongest fiscal year on record.

CrowdStrike operates the Falcon platform, a cloud-native cybersecurity suite protecting enterprise endpoints, cloud workloads, identity, and data. With $5.25 billion in ending ARR and its first-ever positive GAAP net income, the fundamental story looks intact. While the current upside to analysts’ price targets is only 15%, this is a high-quality business that may be worth a closer look.

A Stock That Peaked Above $560 and Hasn’t Recovered

CrowdStrike shares hit a 52-week high of $566.90, but the stock is currently over 20% below that peak. The pressure stems from company-specific overhang and broader sector rotation.

More recently, sentiment weakened after Anthropic unveiled its new “Claude Mythos” model, which it claims can identify hidden cybersecurity vulnerabilities across a wide range of software systems. The model has only been shared with about 40 major tech companies, including CrowdStrike and Palo Alto Networks, but the announcement sparked broader concerns about how quickly AI could disrupt traditional cybersecurity approaches.

That narrative spread quickly across retail channels, with social sentiment on CrowdStrike dropping from around 74 in early March to as low as 28 by late March. While the fears highlight how quickly AI is advancing, the sell-off appears driven more by perception than by any clear change in CrowdStrike’s underlying business.

What 42 Buy-Rated Analysts Are Still Betting On

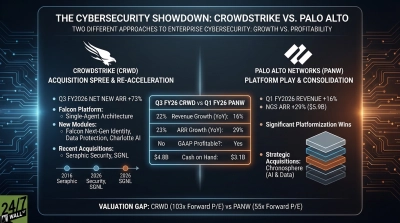

Despite the pullback, Wall Street’s conviction has not wavered. Forty-two analysts rate CRWD a Buy or Strong Buy, with 14 at Hold and zero at Sell. Wall Street is clearly bullish. The bull thesis centers on platform consolidation, AI tailwinds, and an ARR trajectory that management believes can reach $20 billion by FY2036.

Net new ARR grew 47% year-over-year in Q4 FY26 to a record $330.7 million, and the Falcon Flex segment posted ARR of $1.69 billion, up more than 120% year-over-year. Gross retention held at 97%, signaling customers are not leaving. CEO George Kurtz stated: “As enterprises rapidly adopt AI, CrowdStrike is mission-critical infrastructure, securing AI across every layer from GPU to agent to prompt.”

The Q1 FY27 pipeline came in at a record high, and full-year FY27 guidance calls for revenue of $5.868 billion to $5.928 billion, with non-GAAP EPS of $4.78 to $4.90. Module adoption is deepening, with 50% of customers using six or more modules and 24% using eight or more, supporting both retention and upsell revenue.

Strong Fundamentals Paired with Analyst Optimism

At $426.51, CrowdStrike trades at roughly 82x forward earnings based on consensus estimates. The average analyst price target of $489.86 implies about 14.9% upside, which is relatively modest given the company’s growth profile. Still, sentiment remains highly positive, with 42 Buy ratings and zero Sell ratings across 56 analysts.

Year to date, the stock is down 9.0% compared with a roughly 0.9% decline in the S&P 500, reflecting sector rotation and lingering incident-related overhang. Over the past year, however, shares are up 31.2%, showing the longer-term trend is still intact. The balance sheet also remains strong, with $5.23 billion in cash and $1.235 billion in free cash flow generated in fiscal 2026, providing the company with ample financial flexibility.