Anthropic released 11 new plug-ins for its Claude Cowork AI tool at the end of January sparking a massive sell-off in SaaS stocks. The update — enabling automation in sectors like legal, finance, and marketing — was seen as an existential threat to traditional software firms, erasing nearly $1 trillion in market value from software and services stocks over six days.

Shares of companies like Salesforce (NYSE:CRM | CRM Price Prediction) and Workday (NASDAQ:WDAY) dropped sharply amid fears of AI disruption. Two weeks later, the panic has eased, with the threat appearing overstated. Goldman Sachs CEO David Solomon said yesterday, “There’ll be winners and losers — plenty of companies will pivot and do just fine.”

JPMorgan has identified stocks poised to thrive, including CrowdStrike (NASDAQ:CRWD), Palo Alto Networks (NASDAQ:PANW), and ZScaler (NASDAQ:ZS) that are long-term winners amid rising AI-driven threats.

CrowdStrike (CRWD)

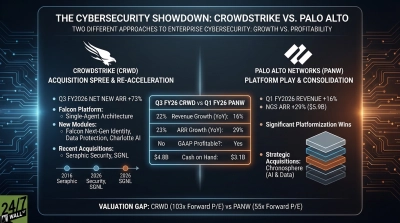

CrowdStrike stands out to JPMorgan for its AI-native Falcon platform, which provides cloud-based endpoint protection and has shown resilience against broader software sector fears. The firm maintains an Overweight rating, viewing CrowdStrike as a high-quality name with potential for short-term rotation back into favor as AI disruption concerns prove unrealistic in the near term.

In its fiscal 2026 third quarter, CrowdStrike reported $1.35 billion in annual recurring revenue from its flexible Falcon Flex offering, underscoring strong customer adoption. JPMorgan highlights the company’s exposure to high-priority enterprise spending in security operations, with its 29 cloud modules enhancing competitiveness.

Analysts expect fiscal 2026 revenues between $4.797 billion and $4.807 billion, up from prior estimates, with non-GAAP earnings of $3.70 to $3.72 per share. The Zacks Consensus Estimate for current-year earnings rose 1.1% over 60 days to $3.71 per share, reflecting that optimism.

JPMorgan sees CrowdStrike benefiting from AI-enabled efficiencies, high switching costs, and multi-year contracts that buffer against shocks. As cyber threats evolve with AI, CrowdStrike’s real-time updates position it for sustained growth, with analysts forecasting 16.8% earnings expansion in 2026.

Palo Alto Networks (PANW)

JPMorgan rates Palo Alto Networks Overweight with a $235 per share price target, citing its comprehensive platform as the most end-to-end in security software. The firm positions Palo Alto as a long-term share consolidator, bolstered by its pending acquisition of CyberArk Software (NASDAQ:CYBR), which adds identity security to its arsenal.

In Palo Alto’s fiscal first quarter 2026, revenues grew 16% year-over-year to $2.47 billion, hitting the top of guidance, with product revenue up 23% to $343 million. Next-generation security annual recurring revenue surged 29% to $5.85 billion, driven by SASE growth of 34% to over $1.3 billion and a customer base expansion of 18% to more than 6,800.

JPMorgan notes Palo Alto’s scale supports profitability, with two consecutive quarters of operating margins above 30%. The company’s unified approach integrates next-generation firewalls, Cortex endpoint suite, and Prisma Cloud, using identity as a key signal across networks.

In a period of AI spending waves, JPMorgan expects Palo Alto to capitalize on enterprise security budgets, with Morningstar viewing it as undervalued by 17% at a $225 per share fair value. Analysts project strong secular tailwinds in a $352 billion cybersecurity market by 2030, making Palo Alto a core holding for diversification and leverage.

Zscaler (ZS)

Zscaler earns JPMorgan’s Overweight rating, with the firm bullish on its cloud-native zero-trust architecture amid a structural move away from legacy networks. In the fiscal 2026 first quarter, emerging products in AI security, zero trust, and data security exceeded $1 billion in combined annual recurring revenue. Revenues beat guidance by $15 million, prompting a $17 million upward revision to full-year outlook, signaling robust multi-product expansion.

JPMorgan highlights accelerating backlog and disciplined cost control as key drivers, with Zscaler forecasting fiscal 2026 annual recurring revenue of $3.698 billion to $3.718 billion and revenues of $3.282 billion to $3.301 billion. The company’s platform targets a $780 billion cloud market by 2030, leveraging AI for threat detection as hybrid work expands.

Analysts note strong traction in Zero Trust Everywhere, supporting medium-term upside despite volatility, with price targets in the mid-$300s. JPMorgan sees Zscaler bucking AI fears through scalability and competitive moats, positioning it for rapid price gains in 2026.

Contact [email protected] for any questions or corrections.