Micron Technology (NASDAQ:MU | MU Price Prediction) has risen 522.09% over the past twelve months, climbing from $65.38 to $406.73. If you watched that move from the sidelines, the question is whether the remaining upside justifies the entry price. The reasons it does — and the risks that could change that — are worth examining carefully.

Valuation: Cheaper Than It Looks

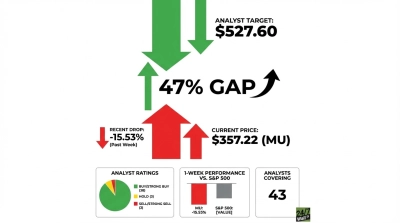

Despite the 500%+ gain, the fundamentals remain compelling. Micron trades at a trailing P/E of 18x and a forward P/E of 6x. A PEG ratio of 0.213 suggests the market has not fully priced in the earnings growth trajectory. For context, trailing earnings per share stand at $22.82, and the company guided Q2 FY26 non-GAAP EPS to $8.42 — for a single quarter. That annualizes to a run rate that makes the current multiple look modest. Gross margin is expanding fast: 56.0% in Q1 FY26, up from 38.4% a year earlier, with Q2 guidance pointing to 68.0%. At 38 buy ratings and zero sell ratings among covering analysts, the consensus target sits at $525.48, implying roughly 29% upside from current levels.

Forward Catalyst: The HBM Cycle Is Still Early

The move in Micron’s stock reflects a real structural shift, not a sentiment bubble. CEO Sanjay Mehrotra disclosed on the Q1 FY26 earnings call that “we have completed agreements on price and volume for our entire calendar 2026 HBM supply, including Micron’s industry-leading HBM4.” The revenue numbers confirm the momentum: Q2 FY26 guidance calls for $18.70 billion in revenue, up from $13.64 billion in Q1. Mehrotra projects the HBM total addressable market will grow from approximately $35 billion in 2025 to around $100 billion in 2028, a CAGR of approximately 40%. Micron is the only U.S.-based memory manufacturer, and its order book for HBM reportedly stretches into 2027. The next earnings report is expected June 17, 2026, giving investors a concrete near-term catalyst to watch.

Risk and Entry: What the Downside Looks Like

The risks here are real and deserve direct attention. Micron raised its FY26 capital expenditure plan to approximately $20 billion, up from a prior estimate of $18 billion. Free cash flow in Q1 FY26 was $3.906 billion — strong, but well below the CapEx pace. The memory industry is cyclical, and NAND oversupply remains a structural risk if AI-driven demand softens. Insider activity over the past three months has been net selling: executives including the EVP of Global Operations and the Chief Business Officer disposed of shares in the $388 to $431 range. The stock’s beta of 1.606 means it will amplify any broader market selloff. The 52-week low was $65.49 — a reminder of how far this name can fall in a downcycle. The stock is currently trading about 12% below its 52-week high of $471.14, which provides a modest cushion relative to recent peaks.

Verdict

Micron is not too late to buy for a retirement-focused investor with a multi-year horizon. A forward P/E of 6x, a fully contracted HBM order book through 2026, and Q2 guidance for record revenue and margins at $18.70 billion and 68.0% gross margin describe a business still in the early innings of a structural earnings expansion, with meaningful upside still ahead. The cyclical risk and heavy CapEx are genuine concerns, so position sizing matters: this is a stock to own with eyes open to volatility, not a set-and-forget holding.