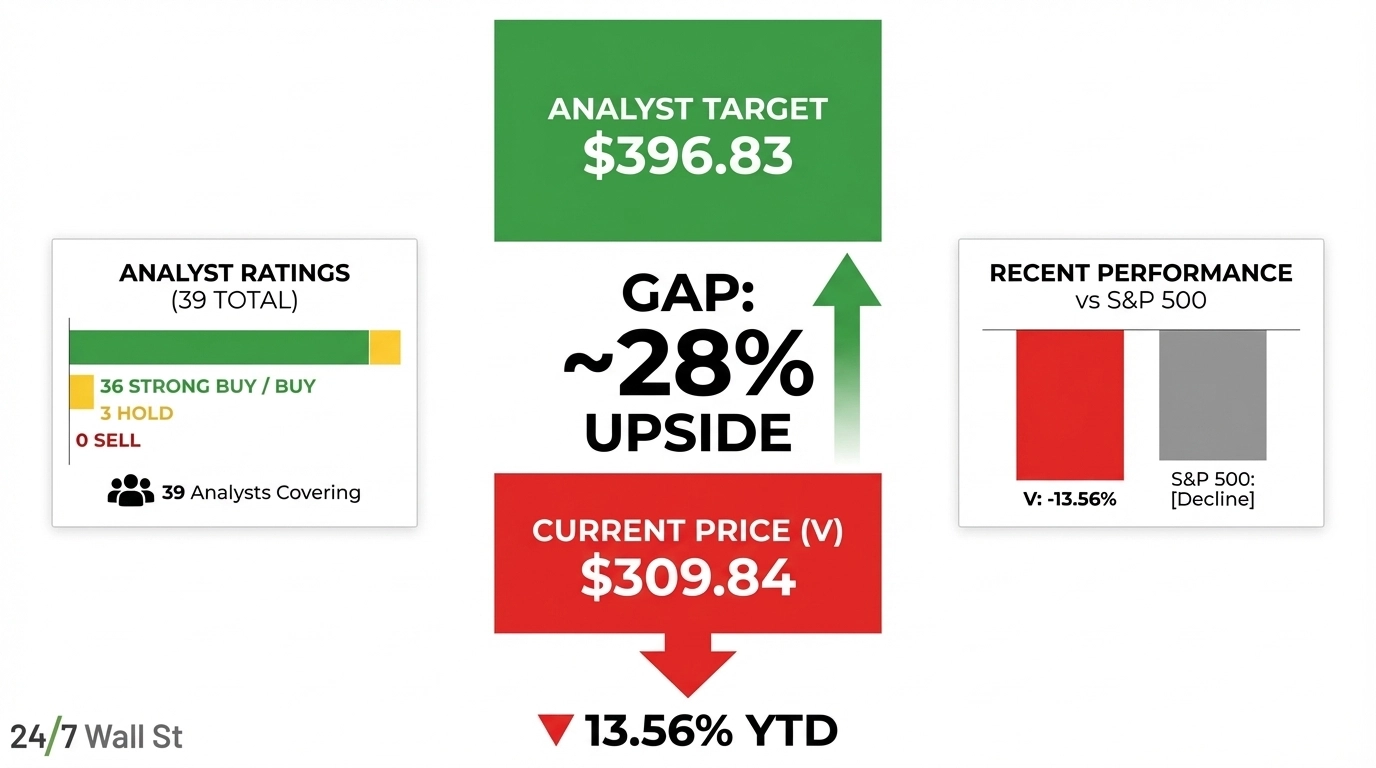

Visa (NYSE:V | V Price Prediction) currently trades around $309.84, while Wall Street’s consensus price target sits around $396.83. This means Wall Street sees roughly 28% upside for the stock today.

Visa operates the world’s largest retail electronic payments network, processing trillions of dollars in transactions annually across consumer payments, commercial solutions, and money movement. It is one of the most widely owned large-cap financials on Wall Street, making a 28% gap between the stock’s price and analysts’ price targets worth examining. The question is whether the market sees something analysts do not, or whether this represents a genuinely attractive entry point in a lasting financial tollbooth business.

A Strong Business Dragged Down by Macro Pressure and Litigation Noise

Visa’s fundamentals remain strong despite the stock selling off 13.56% year to date. The stock hit a 52-week low in late March, pressured by general market weakness and the loss of its NFL sponsorship to American Express, which rattled sentiment around brand positioning. The stock has also traded below its 200-day moving average of $336.21, reinforcing selling pressure.

Litigation adds to the pressure. Visa recorded a $707 million litigation provision in its most recent quarter tied to the interchange MDL settlement, following provisions of $899 million in Q4 FY25, $615 million in Q3 FY25, and $992 million in Q2 FY25. These GAAP charges weigh on reported earnings despite strong underlying cash flows. Non-GAAP operating expenses grew 16% year over year, slightly outpacing revenue growth of 14.63%, a margin dynamic that has concerned some investors.

Analysts Aren’t Blinking, and the Bull Case Remains Intact

Despite the price decline, Wall Street’s conviction in Visa has not wavered. Of the analysts covering the stock, 36 rate it a Buy, 3 rate it a Hold, and 0 rate it a Sell. Loop Capital initiated coverage with a Buy rating and a $387 price target as recently as late March, citing network strength and payments growth trajectory.

The bull case centers on Visa’s ability to compound volume and transaction growth across expanding global payments infrastructure. Cross-border volume grew 11% on a constant-dollar basis in the most recent quarter, and processed transactions reached 69.4 billion, up 9%. CEO Ryan McInerney stated: “Our purposeful investments in our Visa as a Service stack continue to position us as a payments hyperscaler to deliver technology and infrastructure that redefine what’s possible in payments.” Analysts are watching value-added services, tokenization, and real-time money movement as the next growth legs beyond core transaction processing.

Visa is returning significant capital to shareholders. The company repurchased approximately 11 million shares at an average of $342.13 per share in the most recent quarter alone, with $21.1 billion remaining in its buyback authorization. Insider buying activity has been notably positive, with 29 recent insider buy transactions reinforcing confidence from those closest to the business.

What the Numbers Show: A Premium Business at a Discounted Price

Visa currently trades at $309.84, against a consensus analyst target of $396.83, implying roughly 28% upside if analysts prove correct. That target reflects a broad and consistent view across 39 analysts with no bearish outliers. The stock is down 13.56% year to date, meaningfully worse than the S&P 500, which has also declined over the same period. Visa has also underperformed its own recent history, trading well below its 52-week high of $373.33.

The underlying business tells a different story. Revenue grew 14.63% year over year in the most recent quarter, operating cash flow expanded 25.65%, and net income rose 14.34%. The trailing P/E sits at 28x and the forward P/E at 23x, reasonable multiples for a business with Visa’s consistency and network moat. Profit margins stand at 50%+, and return on equity is over 50% as well.

The Bull and Bear Case: What Investors Are Watching

The path back to reach analysts’ consensus price target of nearly $400/share depends on a few key things coming together. The company needs to keep driving cross-border volume growth, expand its higher-margin value-added services, and clear up the litigation noise that continues to weigh on reported earnings.

At the same time, there are real risks to watch. If the macro environment weakens, investors should pay close attention to consumer spending volumes and any increased regulatory pressure on interchange fees. Ongoing litigation provisions look manageable for now, but they remain unresolved, and a worse-than-expected outcome could force analysts to reset estimates.

Stepping back, this is still a business generating 50%+ profit margins with about 28% upside to consensus, which typically does not stay overlooked forever. That said, the stock’s recent pattern tells a story. It tends to rally on earnings and then fade, which suggests the market is not yet ready to re-rate the multiple higher.